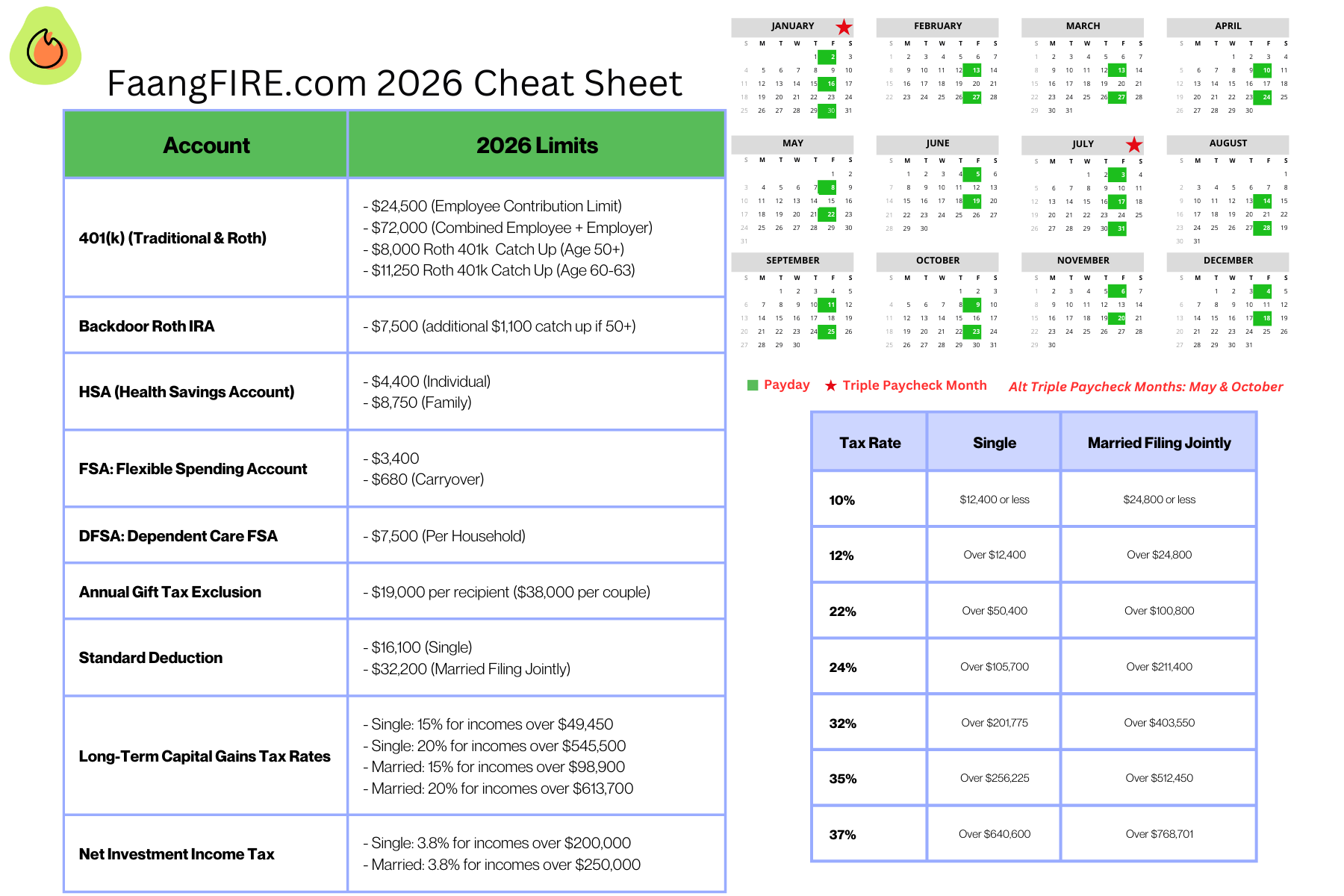

Plan your 2026: Triple Paychecks & Contribution Limits

Happy 2026! By popular demand, here is the 2026 FAANGFIRE.com Cheat Sheet. I created multiple versions for the most common pay schedules, including Meta’s unique 27 pay period year.

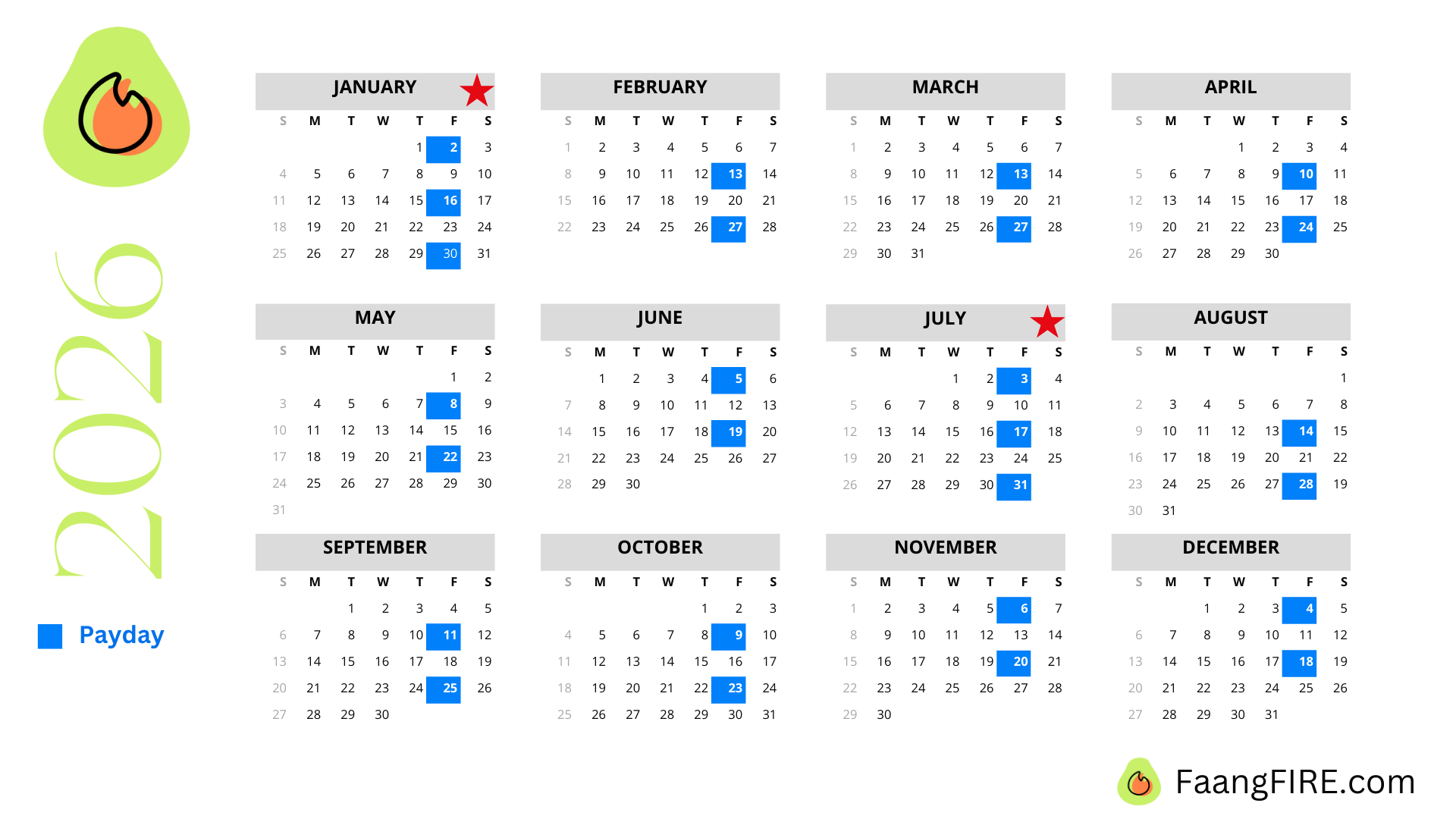

2026 Bi-Weekly Cheat Sheet

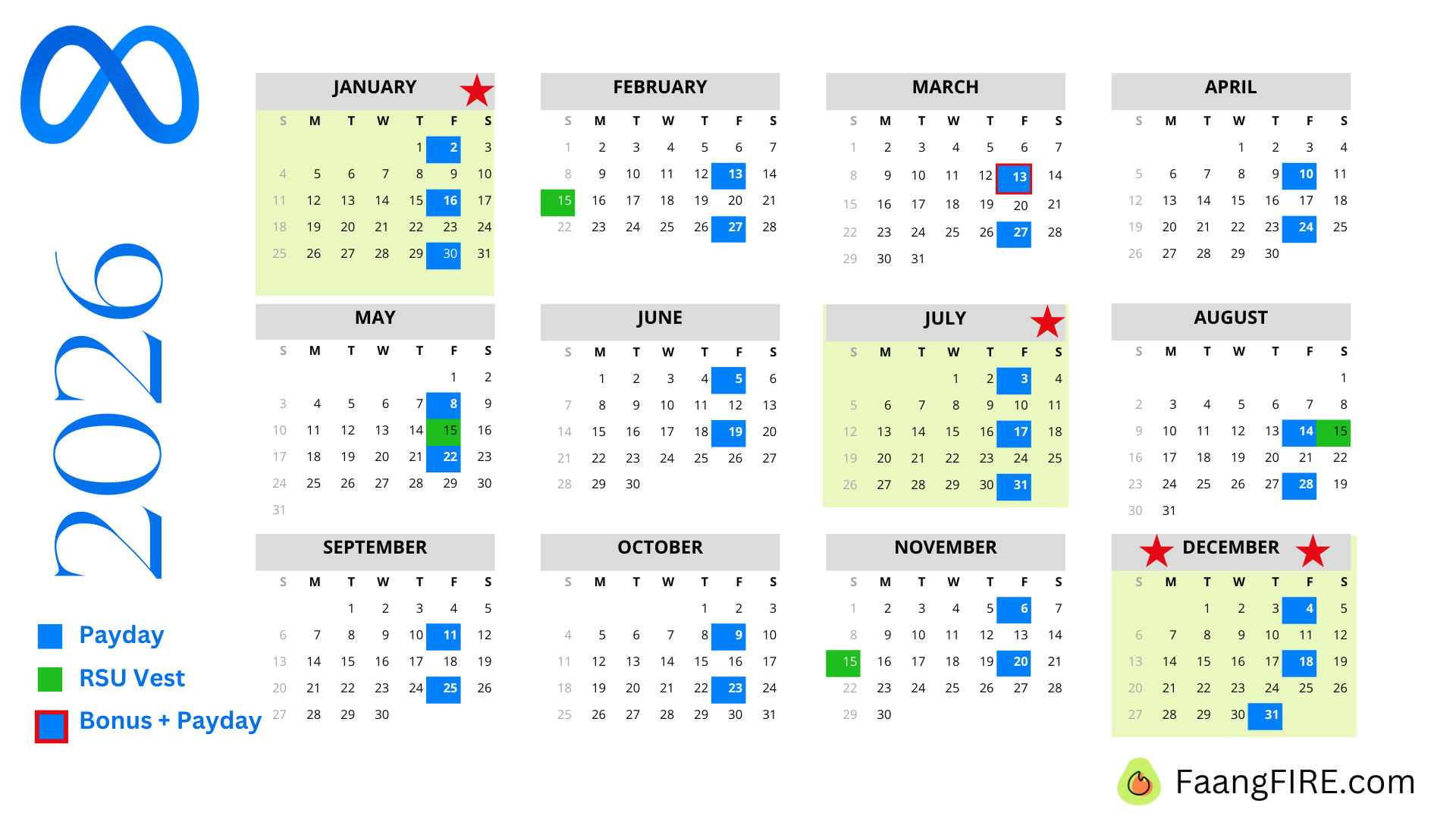

2026 Meta Cheat Sheet

Other 2026 Cheat Sheets

Let’s walk through a few of the sections, so we are all starting 2026 on the same page! There are also additional items below that are not included in the cheat sheet that I personally wanted in one place to reference!

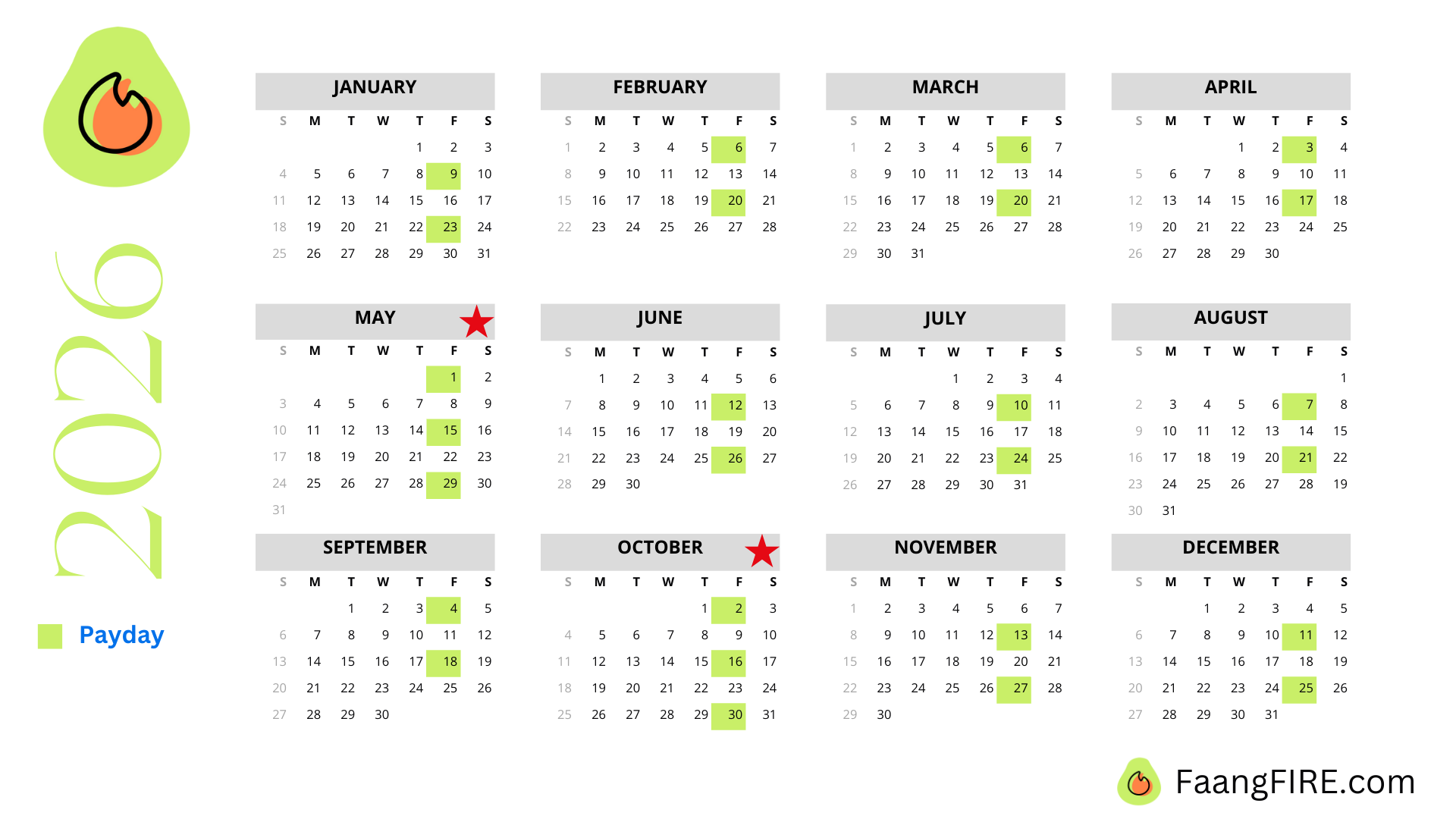

Bi-Weekly Pay Schedule for most FAANG

All of FAANG seems to be on the same bi-weekly pay schedule. This typically results in 26 pay periods with two months featuring three pay checks!

One quirk is that there is occasional years with 27 pay periods. Here is a more detailed breakdown of 2026 for Meta employees that features the unique 27 pay period year they are having:

FAANG Triple Paycheck Months 2026: January and July (+ December for Meta)

A bi-weekly pay schedule results in 26 pay periods per year. This means that there are typically 2 months per year where a FAANG employee will receive 3 paychecks! Since humans are creators of habit, we tend to mentally budget based off two pay checks per month. So the “Triple Paycheck Months” can sometimes make it easier to save those “extra” paychecks.

If your first paycheck of 2026 is 1/9/2026, then your triple paycheck months would be May & October.

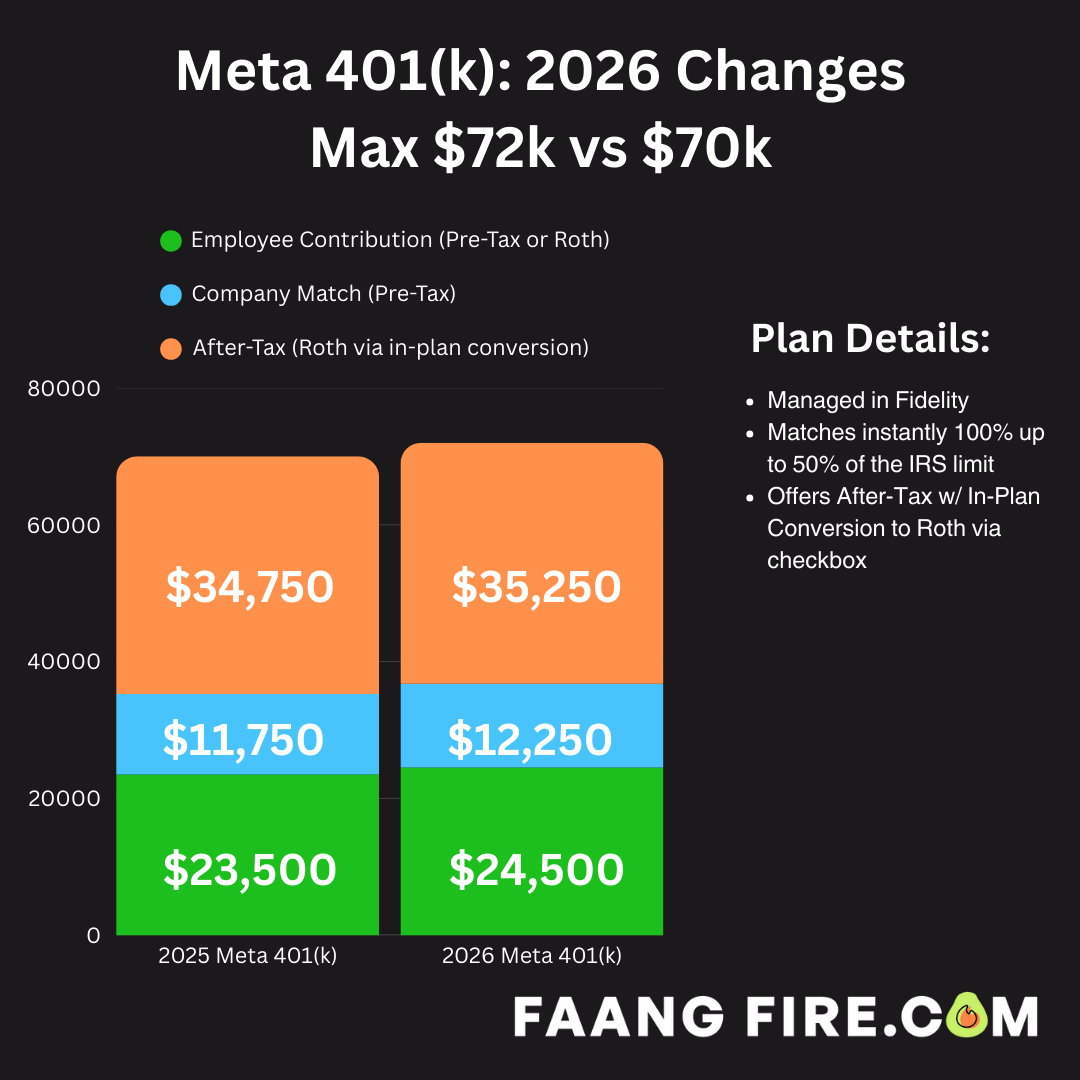

401k 2026 Contribution Limits

$24,500 Employee Contribution Limit (Roth or Pre-Tax)

$72,000 Maximum Contribution Limit (Pre-Tax/Roth + Employer Match + After-Tax)

Example of the 2026 changes for a Meta Employee:

401k 2026 Catch-Up Contributions

If you are 50+ you may contribute an additional $8,000 Roth ONLY (New for 2026 for high earners)

If you are between 60 and 63 there is an odd extra $3,250 catch up bringing the total for this age group to $11,250 Roth ONLY (New for 2026 for high earners)

Past Posts for Reference:

Backdoor Roth IRA 2026 Limits

If you earn more than $153k filing as single or $242k married filing jointly your ability to contribute directly to a Roth IRA is phased out. You would still be eligible to contribute to a backdoor Roth IRA.

$7,500 ( If you are over 50 you can add an additional $1,100 catch-up)

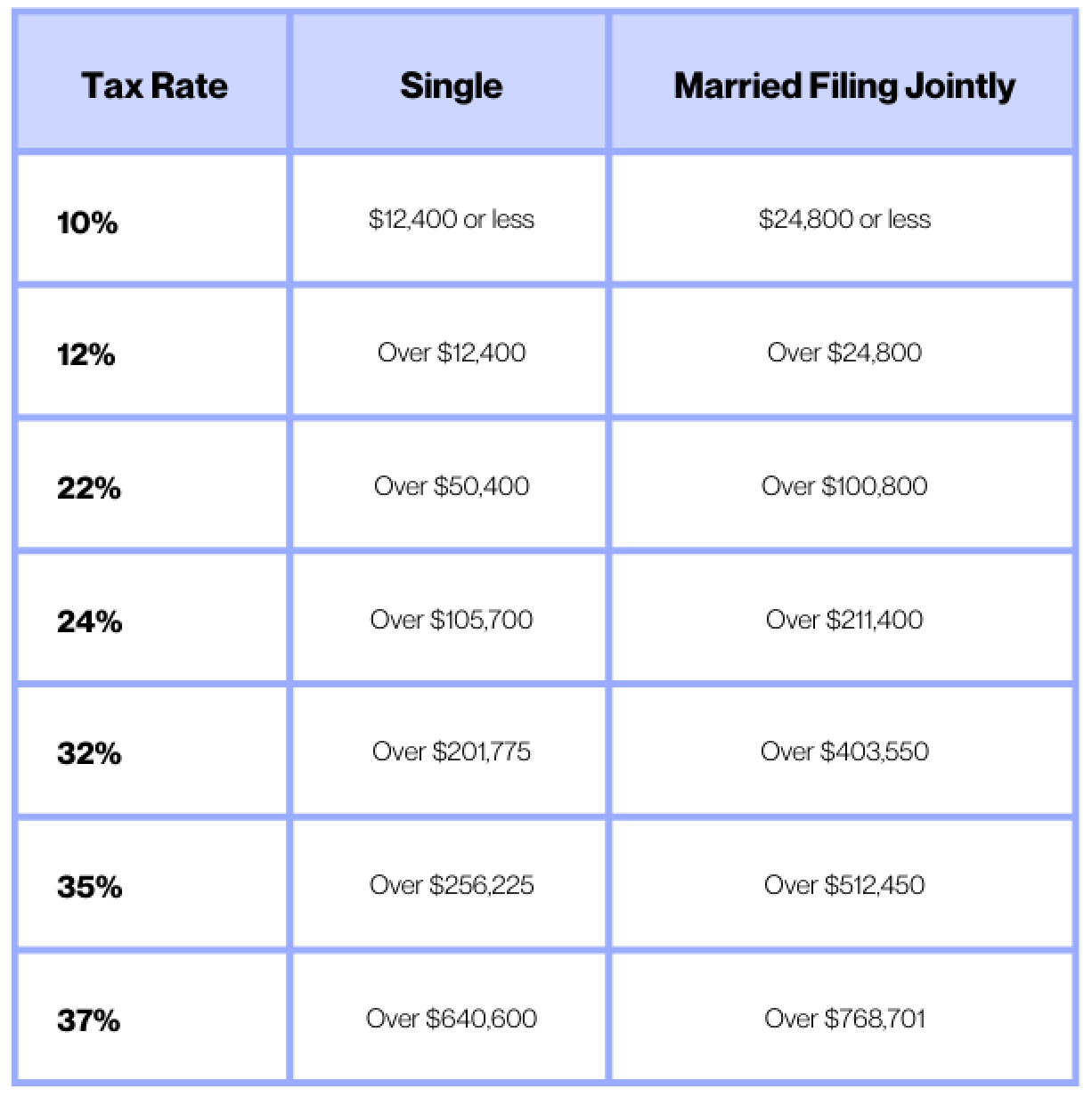

Federal Marginal Tax Rates

For tax year 2026, the top tax rate remains 37% for individual single taxpayers with incomes greater than $640,600 ($768,701 for married couples filing jointly). The other rates are:

35% for incomes over $256,225 ($512,450 for married couples filing jointly).

32% for incomes over $201,775 ($403,550 for married couples filing jointly).

24% for incomes over $105,700 ($211,400 for married couples filing jointly).

22% for incomes over $50,400 ($100,800 for married couples filing jointly).

12% for incomes over $12,400 ($24,800 for married couples filing jointly).

10% for incomes $12,400 or less ($24,800 or less for married couples filing jointly).

Standard Deduction

The majority of tax filers take the standard deduction when they file their taxes. This is essentially the amount of income that isn’t subject to federal taxes by default.

$16,100 if Single and $32,200 for Married Filing Jointly

Long Term Capital Gains Tax Rates for 2026

Long term capital gains typically apply to realized gains on assets that were held for more than 1 year. LTCG also apply to qualified dividends.

15% for incomes over $49,450 ($98,900 for married couples filing jointly).

20% for incomes over $545,500 ($613,700 for married couples filing jointly).

Net Investment Income Tax (NIIT)

This NIIT surtax applies to investment income above the specified thresholds, impacting capital gains, dividends, and rental income.

3.8% above $200k Single, $250k Married

Medicare Tax Rate

All employees contribute 1.45% of their payroll income to fund Medicare, with no upper wage limit for this portion of the tax.

1.45% of payroll income

Medicare Surcharge

In addition to the 1.45% Medicare Tax, if you earn more than $200k in wages you would be subject to an additional 0.9% surcharge.

.9% of additional Medicare Tax for income above $200k Single, $250k Married

Social Security Wage Base

Only the first $184,500 of wages is subject to the 6.2% Social Security tax, though self-employed individuals pay both the employee and employer portions.

The first $184,500 of wages are subject to a 6.2% Social Security Tax (double if self-employed)

HSA 2026 Contribution Limits

Additional Reading: HSAs are 🔥 for FIRE.

$4,400 for individual coverage, $8,750 if your family is covered by a HDHP.

FSA 2026 Contribution Limits

Unlike the HSA, the FSA is a use it or lose it account. Any amount remaining above the $680 carry over limit will be forfeited!

$3,400 with up to $680 allowed to be carried over into 2027

Annual Gift Tax Exclusion Limits: $19,000

For 2026 you can gift $19,000 per individual without needing to cut into your lifetime exception ($15M in 2026).

This is useful to know since it can impact things like 529 contributions.

Looking to accelerate your 2026 Financial Goals?

Accelerate your financial goals by partnering with me 1:1 to identify your FIRE goals and create an action plan on how to achieve it.

Each coaching plan is personalized, confidential, and the best way to get my thoughts on the specifics of your situation.

From on-going accountability, setting up a path to fire, and one-off deep dives. All from a fellow tech worker who has been there.

FAANG FIRE w/ Extra Guac

If you want to kickstart 2026 with access to some of the financial tools I actually use, that’s what the Extra Guac subscription tier is for.

For $200 annually, Extra Guac members get access to the following tools free (new users):

1 year free of ProjectionLab Premium to model your FIRE plans

1 year free of Lunch Money to add logging into your financial life

1 year free of Mezzi to get an AI driven insights into your portfolio

1 year of Carry Solo 401k for $1 to power your Solo401k

$75,000 managed fee free with Frec to power your direct index

30 minutes of 1:1 FIRE coaching with me to help bring it all together

Offers available for first time customers of the tools, you can upgrade to the Extra Guac tier and to claim your codes which will be delivered within 2 days.

Other Financial Tools I Use from my Partners

Top Free Tool: Empower. If you are looking for a free alternative to track your overall net worth Empower (formerly Personal Capital) is my recommendation.

Top All-In-One Paid Tool: Monarch. If you care about strong categorization of your spending, goal setting, smart automation, good design, and are willing to pay Monarch is an easy option to recommend ($99 normally but available 50% off with promo code MONARCHVIP).

Premium Net Worth Tracking Tool For Complex Scenarios: Kubera. Kubera has quickly become one of my favorite net worth trackers. It helps me break down my entire net worth in all the ways I want. Designed to help high-net-worth individuals track their overall finances.

-Andre

ps, I read every reply to these emails