Optimizing 401ks When You Change Jobs Mid-Year

Are you switching FAANG jobs this year? Already switched jobs? Or do you have side hustle income alongside your W2?

If so, you have a unique opportunity to save more than $100k into Roth accounts this year.

The key to unlocking this opportunity is to understand how 401k limits work.

It can mean the difference between saving $70k in your 401k or $140k. That is a lot of tax advantaged goodness to leave on the table.

The 401k Rules to Understand

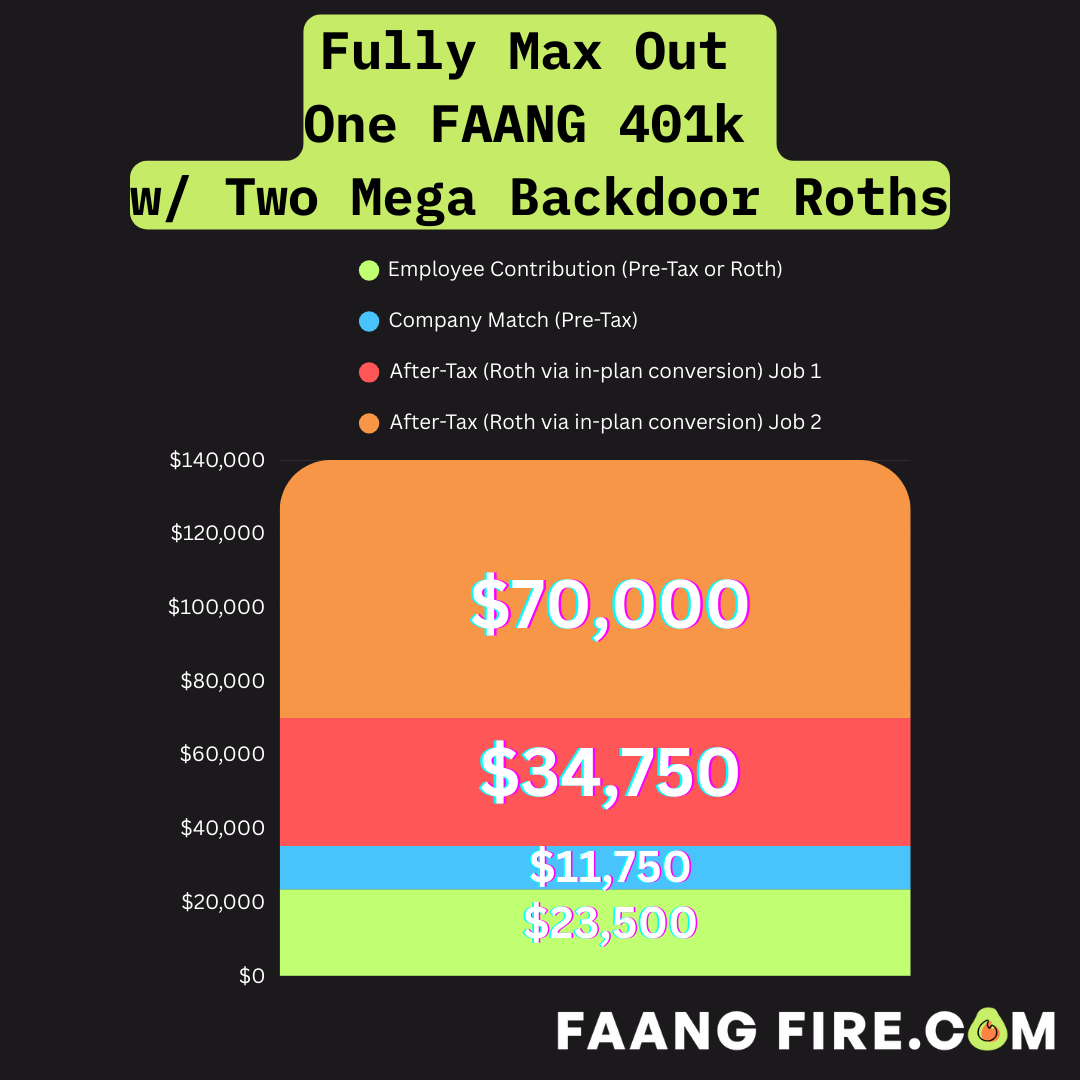

All of you brilliant FAANGFIRE readers understand that in 2025 you are able to contribute $70,000 into your 401k thanks to all FAANG workers having access to after-tax 401k contributions aka the mega backdoor roth.

For example, a Meta or Google employee’s 2025 401k contributions would break down as shown in the image below.

$23,500 Employee Deferral (Pre-Tax or Roth)

$11,750 Employer Match

$34,750 After-Tax with In-Plan Conversion to Roth

As an employee you are able to contribute up to $23,500 across either Pre-Tax and/or Roth 401k while the overall limit when you include your employer match is $70,000.

This is all fairly standard stuff at this point. Many of you are already doing this.

Let’s Dig Into the Underlying Rules a Little More

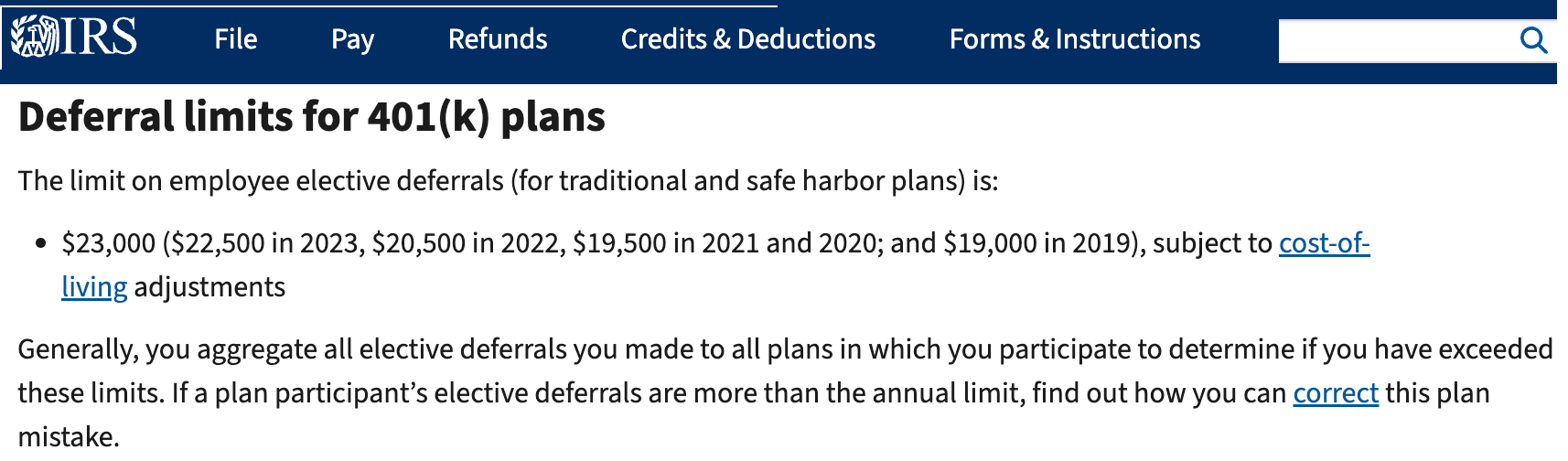

$23,500 is the annual limit an employee can contribute towards elective deferrals (doesn’t include After-Tax) for the entire year.

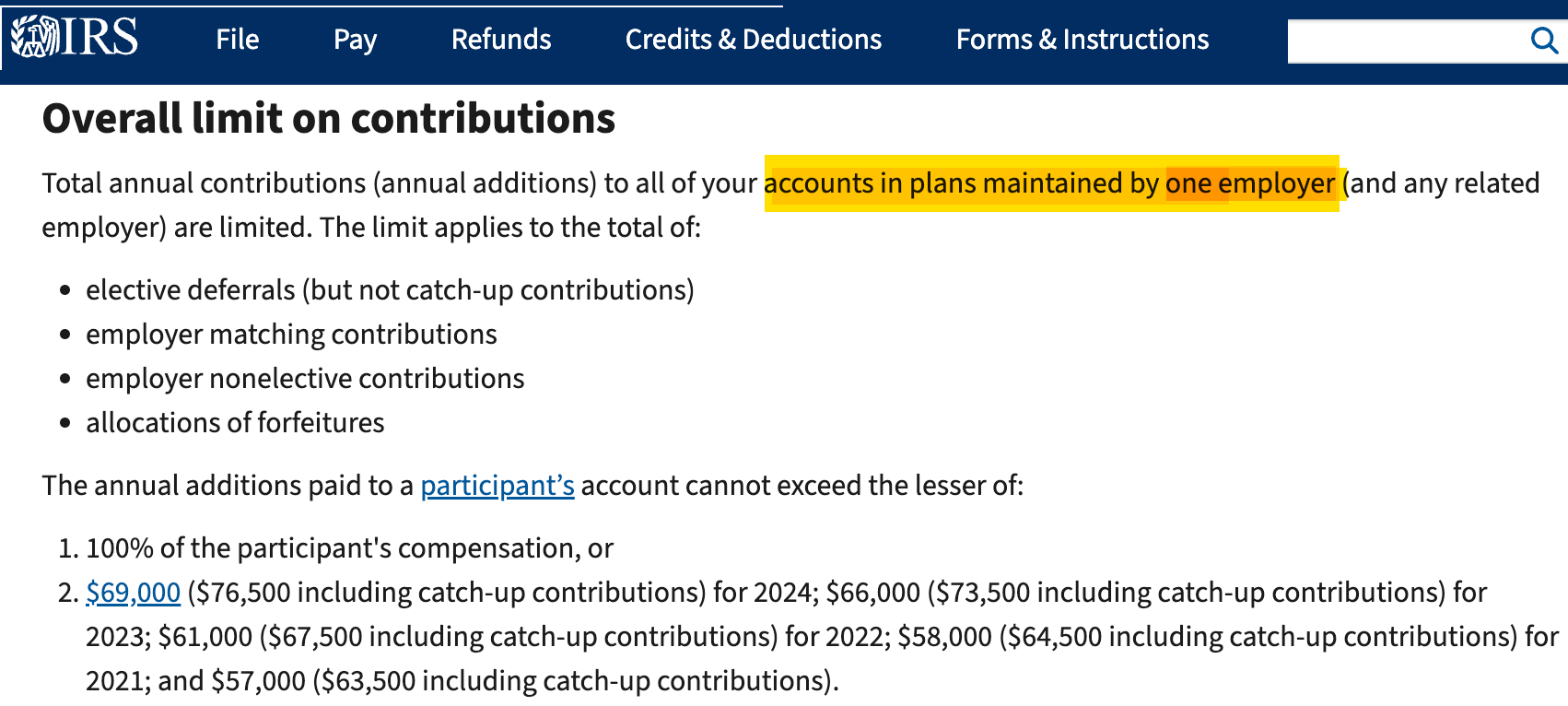

$70,000 is a limit at the employee AND company pair level.

In simple English: If you work at multiple companies in a single year, you have multiple opportunities to contribute $70,000 into each plan.

Let’s Break Down the Types of Contributions according to the IRS

IRS: Employee Elective Deferrals “you aggregate all elective deferrals you made to all plans”.

Translation: The $23,500 you elect (whether pre-tax or roth) applies across all 401k plans you are part of.

IRS: Total annual contributions to all your accounts in plans maintained by one employer are limited to… $70,000.

Translation: Every employer you work for has a separate $70,000 overall limit to your 401k.

This means that when you switch jobs mid-year, you could contribute a theoretical $140k into your 401k.

Job 1: $70,000

$23,500 Pre-Tax Employee Deferral

$11,750 Employer Match

$34,750 After-Tax with in-plan conversion to Roth (mega backdoor roth)

Job 2: $70,000

$0 Pre-Tax Employee Deferral

$0 Employer Match

$70,000 After-Tax with in-plan conversion to Roth

Additional Resources from Kitces, and White Coat Investor on the topic.

Notes:

Companies often have their own plan limits. Meta, for example, limits After-Tax contributions to $34,750

If you have side income, you can contribute an incremental $70k (see below)

A More Optimized 401k Contribution Plan

In the original scenario the employee missed out on their Job 2’s employer 401k match because they had already contributed $23,500 to Job 1’s Pre-Tax Employee Deferral. If you know you are switching jobs, you could strategically only contribute enough to get the full match at Job 1 to allow yourself to still get the match at Job 2.

Example Scenario: Hass is a senior engineer at Meta who is joining Uber in Q4.

Let’s walk through the different ways Hass could approach optimizing their 401k contributions.

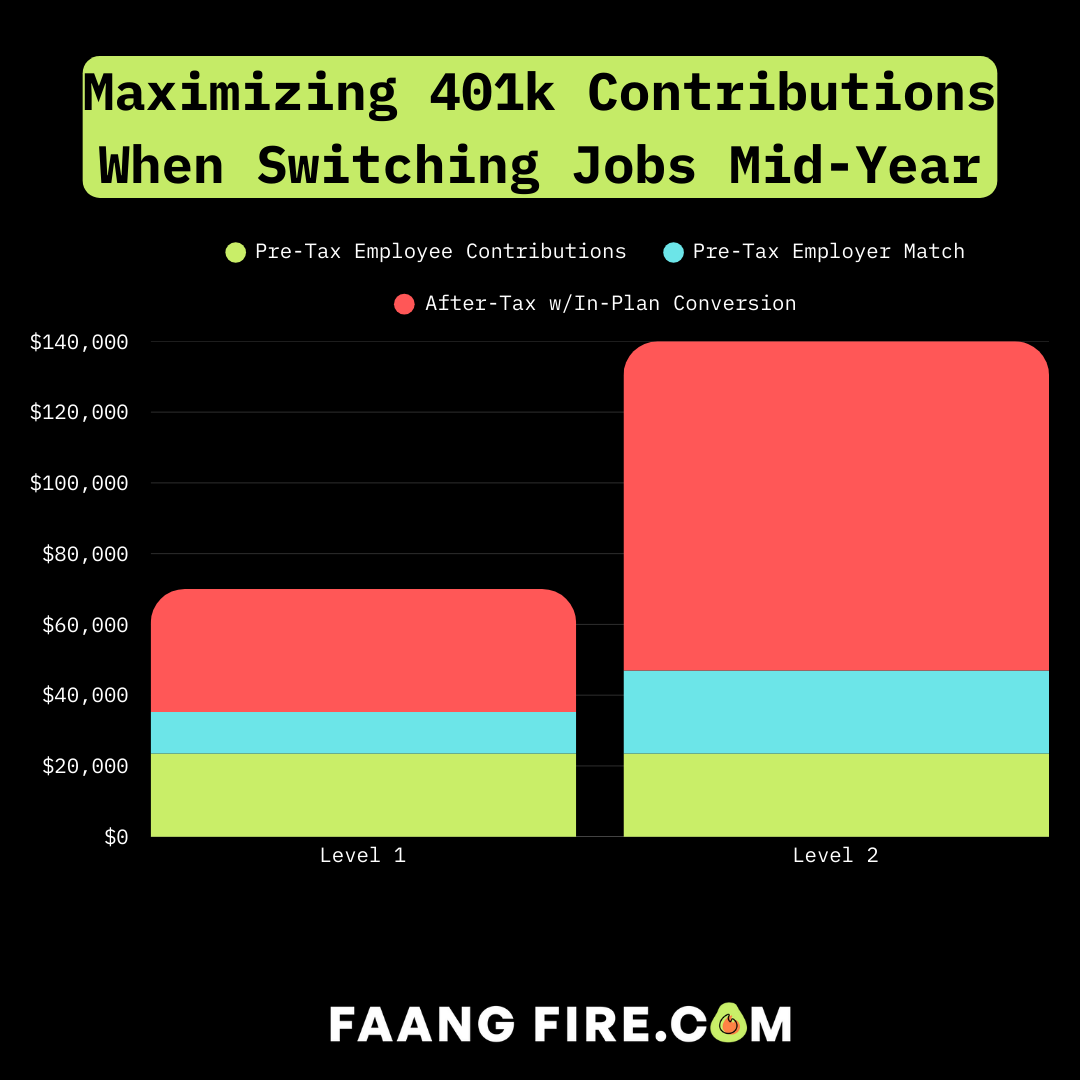

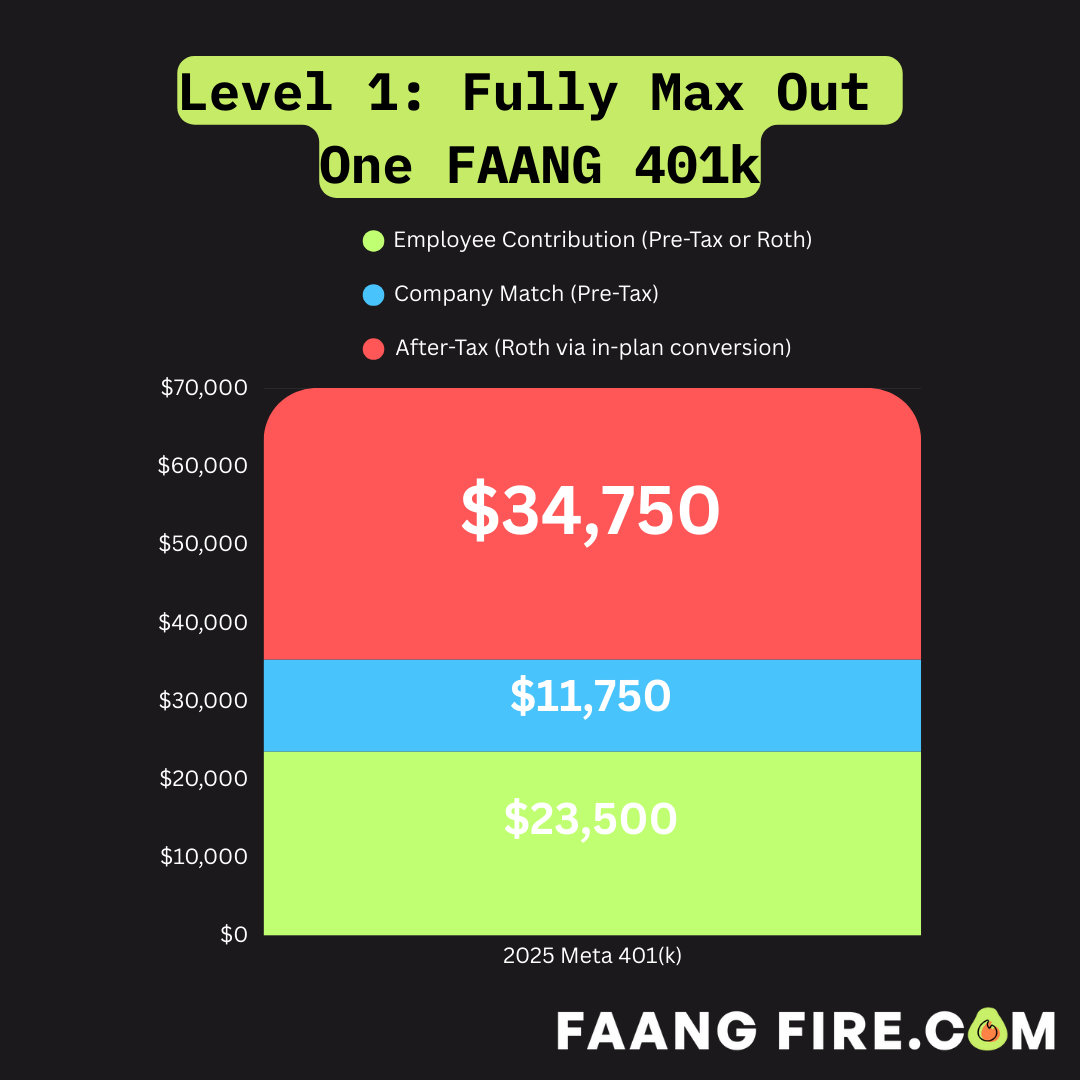

Level 1: $70,000 Contributed ($23,500 Employee Contributions, $11,750 Meta Employer Match, $34,750 After-Tax)

In level 1 Hass fully maxed out their 401k while at Meta. They are awesome. They think that their 401k is being fully maxed out for the year. So when Hass joins Uber they end up waiting until 2026 to contribute more to their 401k.

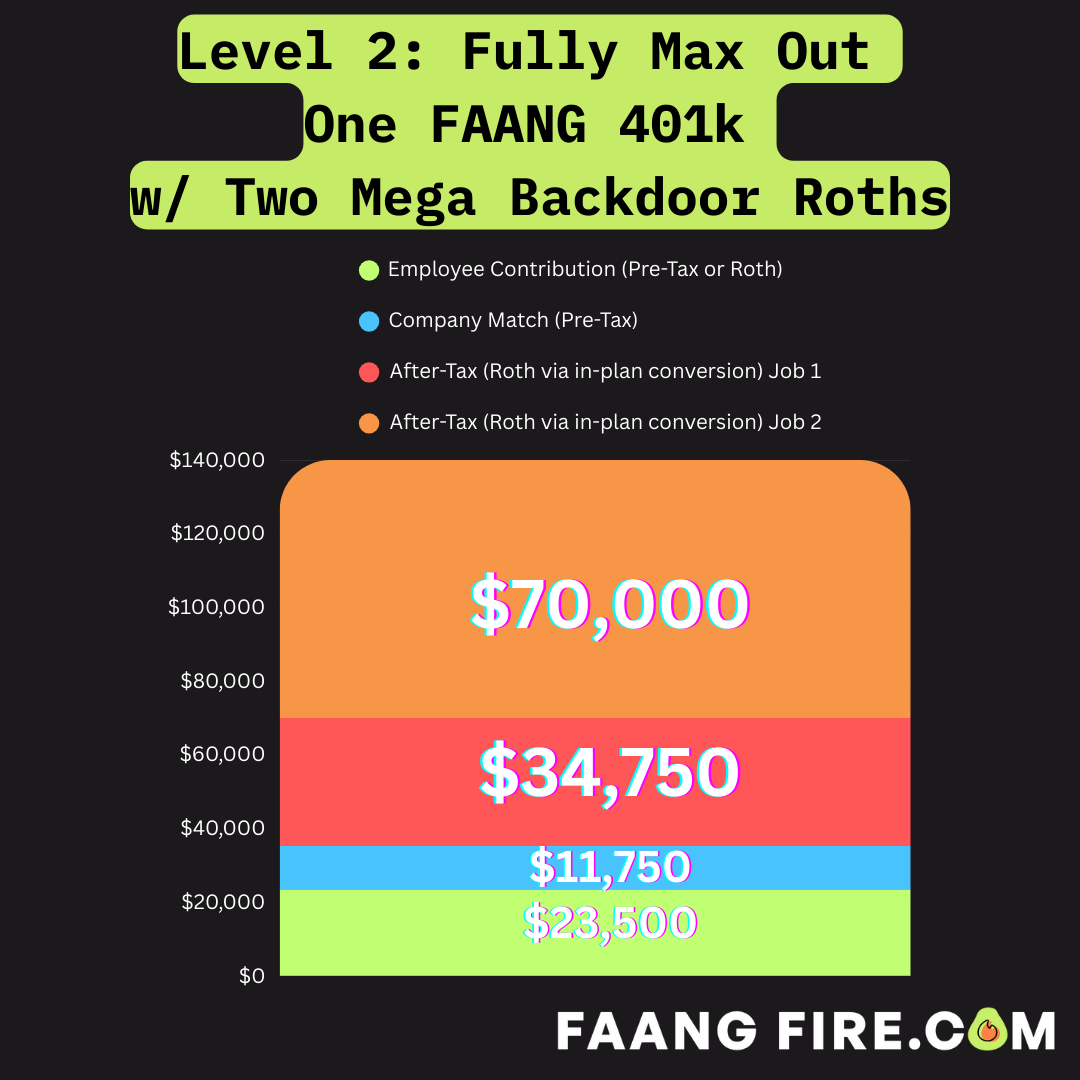

Level 2: $140,000 Contributed ($23,500 Employee Contributions, $11,750 Meta Employer Match, $34,750 After-Tax at Meta, $70,000 After-Tax at Uber)

Hass is a badass FAANGFIRE subscriber. They know that the $70,000 401k limit applies to each company plan they are part of. So they fully max out their 401k while at Meta with $70,000 and then when they join Uber, Hass contributes $70,000 directly into the After-Tax at Uber*.

*Uber’s maximum contribution per paycheck to their After-Tax is currently 45% which could make it difficult for Hass to reach the full $70,000 depending on when they joined during the year.

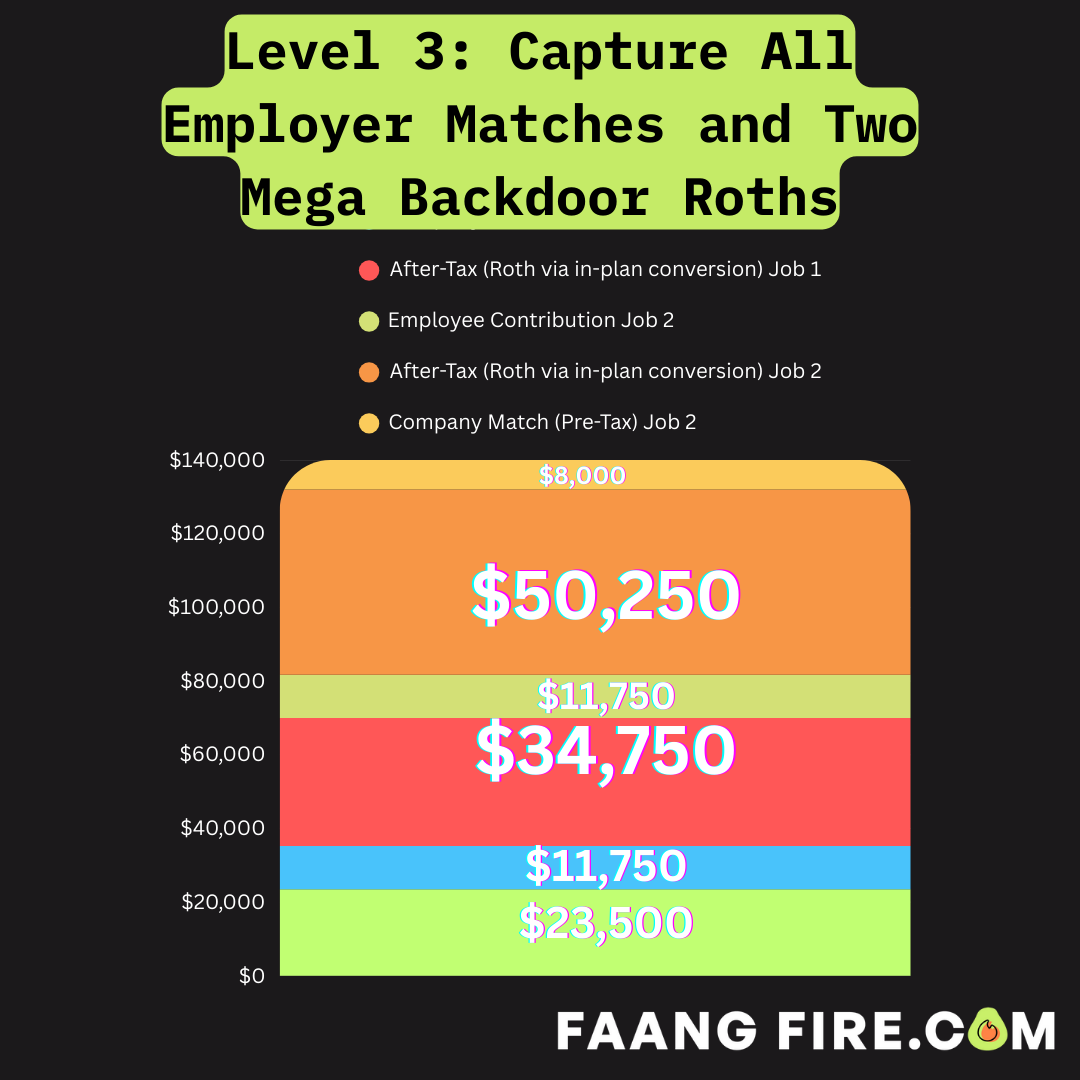

Level 3 $140,000 Contributed ($11,750 Employee Contribution at Meta, $11,750 Meta Employer Match, $34,750 After-Tax at Meta, $11,750 Employee Contribution at Uber, $8,000 Uber Employer Match, $50,250 After-Tax at Uber)

Hass has incredible planning skills and a deep understanding of both Uber’s and Meta’s 401k. They were able to milk every single free employer contribution. So while Level 2 and 3 both result in $140k in Hass’s 401k, in Level 3 $8,000 of that is from the company. Which means Hass would have an extra $8,000 to invest in their taxable portfolio (or spend on avocados).

Notes:

There is nuance depending on the specific companies’ 401k plans. For example at Meta you can contribute $11,750 and receive the full match of $11,750 instantly. While at Google, they contribute 50% up to a total contribution of $11,750. So the only way to get the full Google match is to contribute $23,500 in employee contributions into your Google plan.

It is sometimes possible to get Job 1 to do a withdrawal of excess contributions to make room for you to contribute to Job 2’s 401k and receive the match. However the success of this has been very hit or miss. The company isn’t obligated to do this and if you overcontribute, you can end up paying taxes on the overcontribution twice.

FAANG + Side Hustle Income

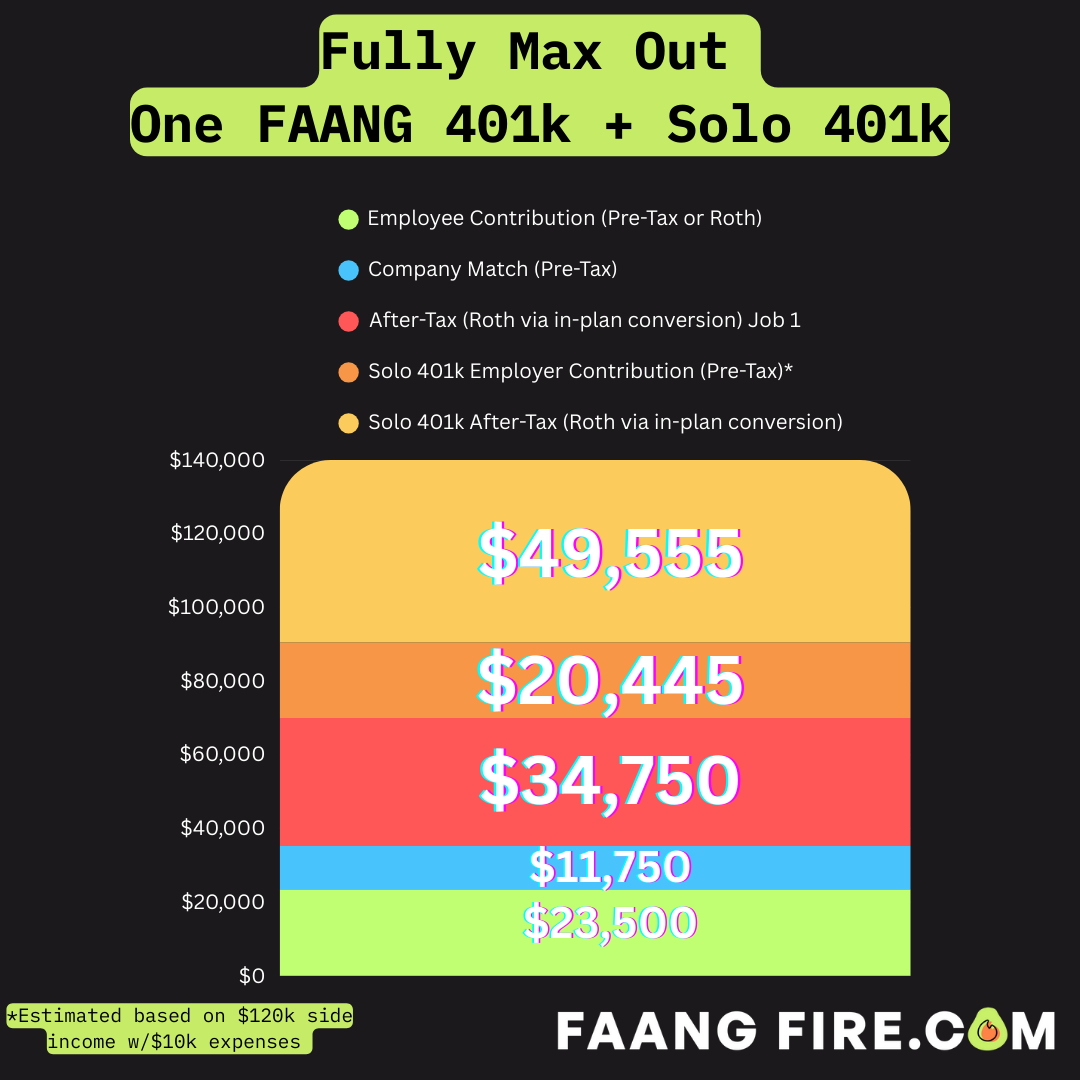

Level Hustle: $140,000 Contributed ($23,500 Employee Contributions, $11,750 Meta Employer Match, $34,750 After-Tax, $20,445 Solo Employer Contributions, $49,555 After-Tax)

Hass is somehow working full time at Meta and also bringing in $120k selling Avocado NFTs. Hass is now able to contribute $70,000 into their Solo 401k in addition to the $70,000 they contributed to the Meta plan.

Just like how someone with two jobs in the same year can contribute $70,000 into two separate company 401ks. When you have your own business, you can do the same thing!

You can still only contribute $23,500 in elective deferrals to your pre-tax or Roth 401(k). However, what's unique about having your own 401(k) for your side hustle is that you may be able to also contribute on behalf of the employer (aka also you).

For Employer Contributions, Sole Proprietors and Single-Member LLCs can contribute up to 20% of your net self-employment income (net profit minus half of self-employment tax). This is why Hass is able to contribute $20,445 in employer contributions into their Solo 401k.

I personally use Carry Money for my Solo 401k. I would definitely recommend Carry Money for anyone with a side hustle or your own business. There is a $299 annual fee, but they helped me receive a $500 tax credit as part of the Secure 2.0 Act, which I’ll also get the next two years. They were one of the few places that made it easy to set up mega backdoor roth contributions and it is so nice using a website that wasn’t created in 1995.

This email isn’t sponsored, but I may receive an affiliate commission if you sign up through my link. This helps FAANG FIRE generate a profit so I can contribute back into my Carry Money account while also keeping FAANG FIRE free.

What do you think? Have you contributed to multiple 401ks in the same year? What is your strategy?

Hi Andre,

I worked at Google and Meta in 2025 (about 6 months at each) and maxed out my 401k contribution at Google and then did $11750 at Meta. I thus over contributed by $11750 and am now doing taxes. I have heard some people have had their matches clawed back after requesting a withdrawal of excess contributions. Since you mention my exact scenario, curious if you know any strategy here.

Thanks, Andre! You could also note the potential for catch up contributions for people 50+.