My San Francisco Plans and Q1 Progress Against Goals

The first quarter of 2023 is now in the books. The end of the quarter is the perfect time to look at how the year is going to see if there are any adjustments needed to hit our full year 2023 goals.

Macro Themes from Q1:

Tech layoffs continue and in many cases accelerate across much of FAANG

Silicon Valley Bank forces everyone to refresh their understanding of FDIC and SIPC

Stronger Pushes for Return to Office

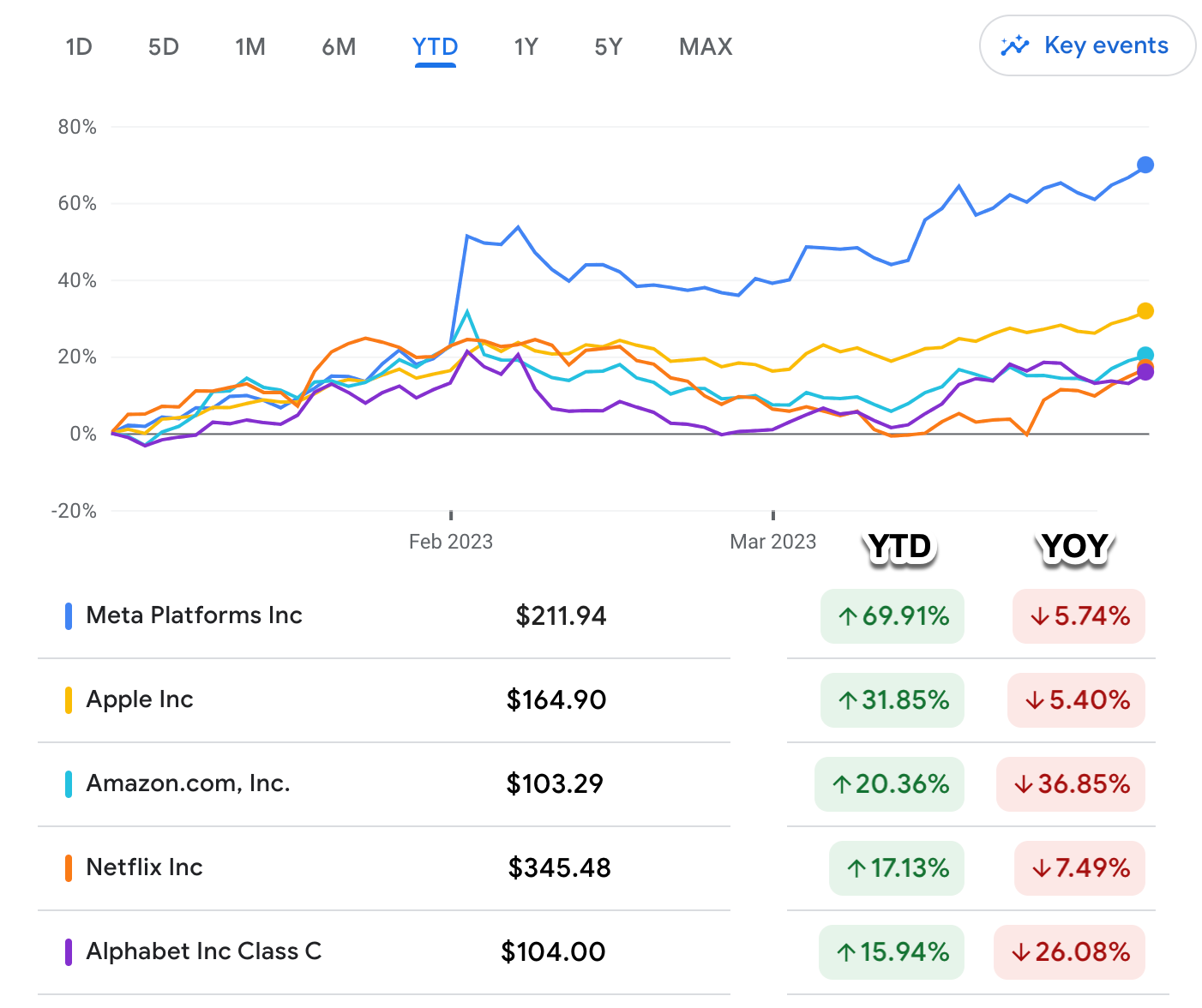

Year to Date FAANG Stocks up 17-76% (still very down year over year)

Year to Date Overall Market up 7%

FAANG Stock Performance

Start With “WHY”

Whenever talking about goals it is very easy to just dive straight into the numbers. Just like in work, it is important to ground yourself into the WHY behind the numbers.

My personal mission statement helps capture the WHY.

“I want to be able to Avocado FIRE in the next 5 years after hitting my “Enough” number of $3.3M in index funds, $600k housing fund, and $90k college fund. I want to achieve my goals while also ensuring that I also set up my daughter to have a future where she is able to contemplate ridiculous things like early retirement (if she chooses). I also really want to be living somewhere that I can see myself staying for the next 3 years.”

If you want to learn more about how I developed this plan, be sure to go to Step #1 of my 2023 Financial Plan.

Non-Financial Goals

Measuring progress against numeric goals is relatively straightforward. What about the rest of my mission statement, how can I measure whether I am making progress?

These are more “ship goals” than ones that can be measured numerically.

For example, this part of my mission statement:

I also really want to be living somewhere that I can see myself staying for the next 3 years.”

Here is what I had to say about this in June of last year.

…the most common question I get when talking with people is “Where are you moving?” Apparently when you write multiple articles about relocation, the benefits of leaving CA, and how you can make more money in Texas, people get the idea that you are planning on leaving. It isn’t like I wrote a piece titled “The Analysis into leaving San Francisco” or anything. I almost feel obligated to leave San Francisco at this point! But the city can’t get rid of me that easily. I have renewed my rental lease until July 2023.

As mentioned above, my rental lease is up in July 2023. We have no plans to stay in our current rental for a number of reasons (school proximity, water leaking, usability of space).

So Am I Leaving San Francisco?

One of the biggest factors that would accelerate my plans to leave San Francisco would be if my daughter, who is turning 5 this month, didn’t get into a good public school in San Francisco.

San Francisco’s public school system is so complicated an entire sub-industry of public school consultants have emerged to help parents navigate the system. As part of the system you submit a ranked list of preferred schools. We had 25 schools on our list. We were primarily targeting language immersion programs as well as highly ranked schools (whatever that means). Instead of targeting schools near where we lived, we targeted the best schools in parts of the city we would be willing to move to. Since we had location flexibility, it didn’t make sense to me to need to go to a private school in order to get a good education. I would rather move to a city with a stronger public school system and more predictable admissions.

… and about Remote Work

The future of remote work is murkier than ever before. I clearly hedged my bets by going remote while remaining in San Francisco. I think remote work is here to stay in some capacity, but I just not as confident as before. While continuing to work in tech I just feel more confident staying in a major tech hub.

While continuing to work in tech I just feel more confident staying in a major tech hub. Particularly during this period of efficiency, having the pool of available new opportunities is once again a significant factor.

Lottery Results

With the first round of the San Francisco City-Wide lottery finished, we are really happy with our assigned school. While we didn’t get into a language immersion program yet, our assigned school is still very good. It is within one of the cities more residential neighborhoods that would still be commutable to the Uber office for my partner.

So between my lack of confidence in the future of remote work, some level of job insecurity, and good public school prospects… San Francisco will continue to be home.

5 More Years?

I have always viewed my time in San Francisco as a perpetual cycle of “1 more year”. With my daughter starting elementary school in August, for the first time ever, I can picture myself in this city for the next 5 years.

One interesting thing about the 5 year mark… it is where the Rent vs Buy calculators start to hit break even.

I still put the probability of me buying at <5%. But since I am moving anyway, I am occasionally flipping the toggle between Rent/Buy a little more often while keeping track of interest rates and local housing trends.

What about beyond 5 years?

I am hoping that the next 5 years will see me with the option to FIRE. Being able to FIRE in San Francisco is simply requires an order of magnitude more money than nearly anywhere else for the level of Avocado FIRE that I want.

Recap of my Investment Goals:

The specific numbers within my mission statement are part of my “Long Range Planning” to hit my Enough Number. I have specific annual numeric goals on a per-account basis for the year that ladder up into my LRP.

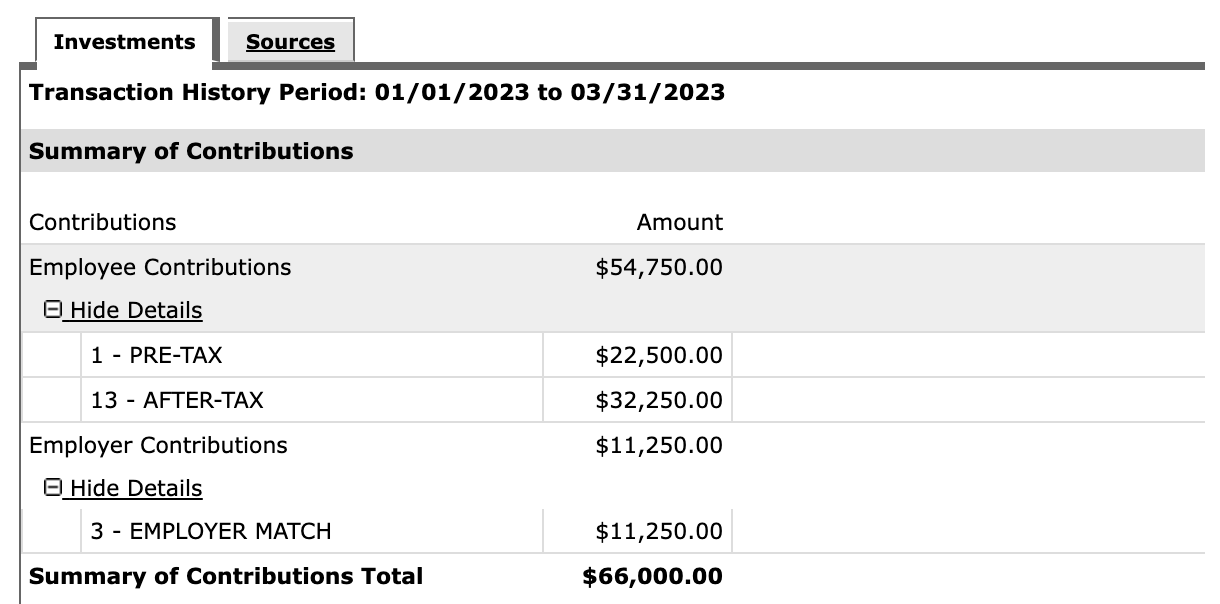

$66,000 towards maxing out my Meta 401k + After Tax.

$22,500 to Traditional 401k

$11,250 Meta 401k Match. they match 100%, dollar for dollar, up to 50% of the 401k limit (22,500/2= $11,250)

$32,250 After-Tax 401k which gets auto-converted to the Roth 401k in Meta’s plan.

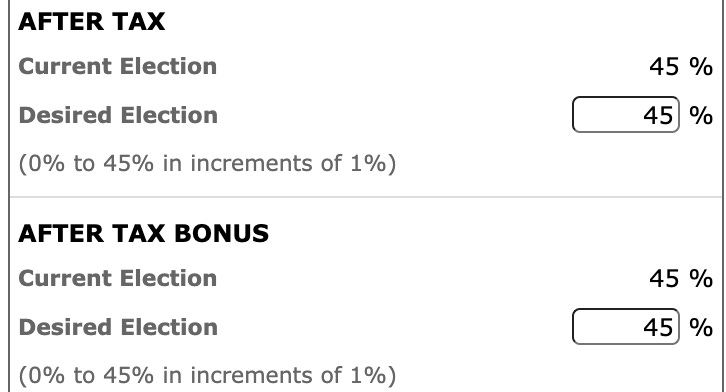

$66,000 towards maxing out my partners Uber 401k + After Tax.

$22,500 to Traditional 401k

$0 Match, Uber does not have a 401k match

$43,500 After-Tax 401k which gets auto-converted to a Roth 401k

$20,000 into iBonds

$13,000 into Backdoor Roth IRA

Any additional excess will then go towards my taxable brokerage, 529 college savings, and moving fund

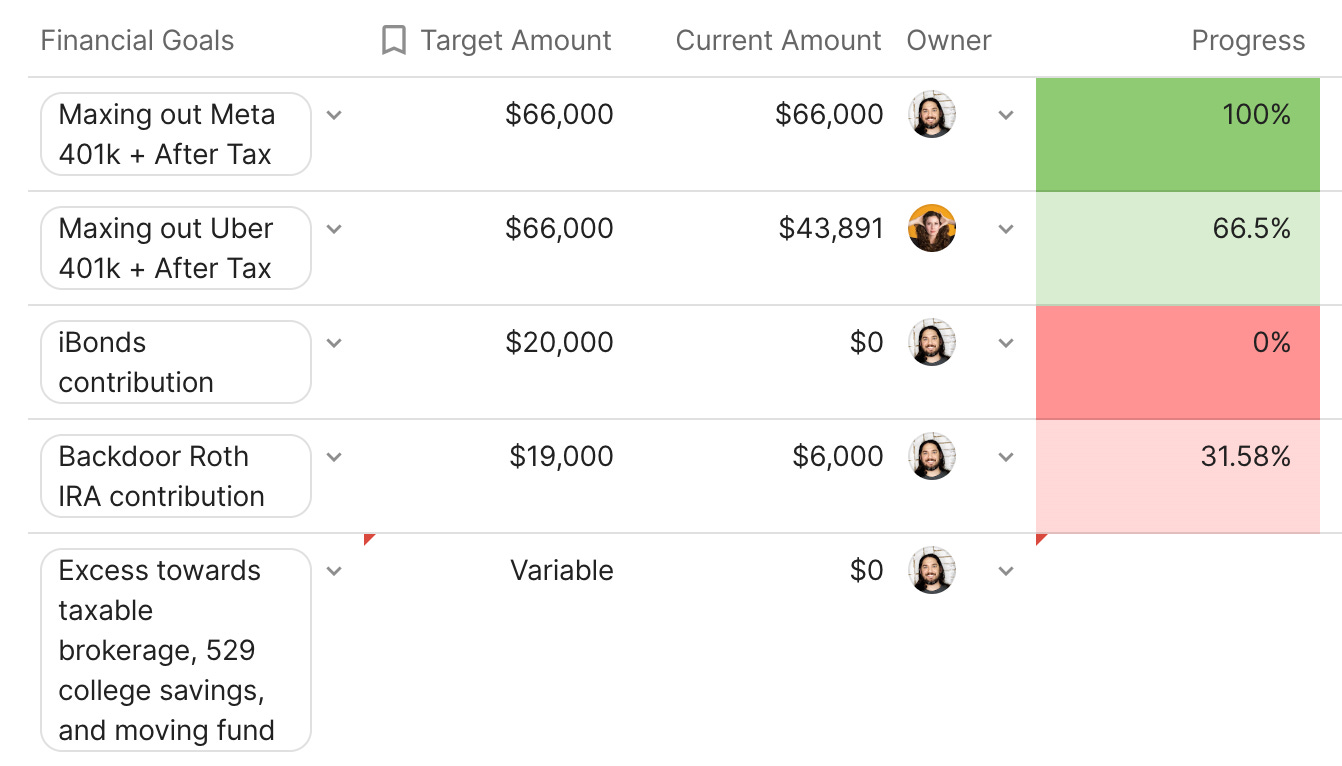

Current Status of Financial Goals:

Goal #1: $66,000 towards maxing out my Meta 401k + After Tax

Status: Green, Goal Hit

Notes: $66,000 out of $66,000 complete. Thanks to “Budgeting Hard Mode” this is finished in Q1.

Goal #2: $66,000 towards maxing out my partner’s Uber 401k + After Tax

Status: Green, On Pace to Hit Goal in Q2

Notes: $43,900 out of $66,000 complete. While also doing “Hard Mode” there is a contribution cap within the Uber 401k plan where “After Tax” can’t be set to greater than 45%. Still fully on track to hit our goals.

Goal #3 $20,000 into iBonds

Status: Red, Goal to be reassessed

Notes: $0 out of $20,000 have been contributed. This goal is being reassessed since iBonds may not be the most optimal investment in 2023. We will know more in April, but there is a high likelihood that T-Bills, CDs, or even just a high yield savings account would be a better place to put these funds, which I use as part of my final tier of my emergency fund.

Goal #4 $13,000 into Backdoor Roth IRA

Status: Green, Goal increased from $13,000 to $19,000. Still on track.

Notes: This goal should be updated from $13,000 to $19,000 since I contributed to my partner’s Backdoor Roth for 2022 in March.

$6,000 out of $19,000 contributed have been contributed. While I finished my partner’s 2022 contribution after rolling over their rollover IRA into their Uber 401k we still need to make our 2023 contributions. Due to “Budgeting Hard Mode” the cash flow available to make these contributions will only be available in Q2. Still on track to hit the new increased goals.

Goal #5 Any additional excess will then go towards my taxable brokerage, 529 college savings, and moving fund.

Status: Meh, Let’s call it Orange

Notes: 0 progress here. I have been going 3 months with nearly $0 paychecks. My taxable brokerage will become the primary target of future excess cash flow, in addition to future investments in a 529 college savings account, and building up a moving budget buffer.

So all in all it has been a successful start of the year…. at least from a metrics standpoint.

But it definitely hasn’t felt like a successful year.

I expect that over the next couple months… i’ll experience more volatility.

While I try to focus on what I can control… I can’t always control what needs to be focused on.

Change is never easy… but I know i’ll get through this with confidence in my planning.

Good luck out there.

-Andre