Experimenting With Spending More

What if I told you that you might be better off spending more?

The early FIRE movement was built around the core tenets of frugality, anti-consumerism, delayed gratification, and living well below your means.

Save more than 50% of your income. Drive a used Civic. Invest what you save in low-fee index funds. Keep your spending low even as your pay rises over time. Boom, the magic behind retiring early.

Frugality was at the heart of everything.

I think that can be a very powerful place to start.

In fact it is where I started my FIRE journey.

Combine that level of frugality with a high tech salary and, with a well-defined idea of “enough,” you can reach financial independence on something close to easy mode.

But it can go too far.

That frugality that helped you be at the doorstep of your FIRE number 10, 20, or even 30+ years early may now be preventing you and your family from fully enjoying the life you worked so hard to build.

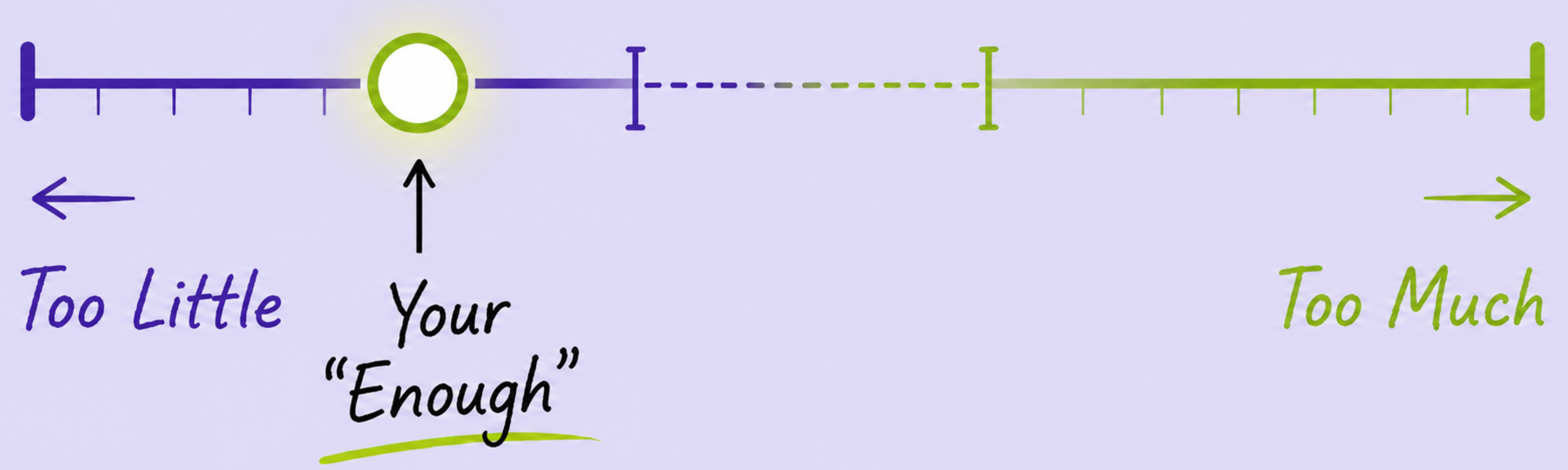

As you approach your enough number, the question should be:

How could I spend more to make my life meaningfully better?

I don’t want to adjust my lifestyle to fit my enough number; I want my enough number to reflect the lifestyle I want to be living.

A quick note on this post: it isn’t designed for everyone. It is designed for the FAANG worker who is already saving and investing aggressively and is within five years of their enough number.

Today’s newsletter is sponsored by Wealthfront.

One of my 2026 goals is to be more intentional with how I spend money. Wealthfront is a key part of that.

My high-yield Cash Account at Wealthfront is where I keep part of my cash, including money I want to earmark for specific goals. I am not just using Wealthfront to save for the future, I am also using it to help me spend more intentionally today.

Right now for a limited time, you can earn up to 4.30% variable APY on your cash. Wealthfront is offering my audience an exclusive 0.75% APY boost for three months on up to $150,000 when you open your first Cash Account using my link. You also get another 0.25% APY increase by direct depositing $1,000 a month and maintaining a funded investing account. Go to wealthfront.com/andre. Base APY is 3.30% as of 1/30/26, is provided by program banks, and is subject to change. Promotional terms and conditions apply. See our affiliate link for more details.

Spending for Sustainability?

I captured a similar sentiment in my Dear Highly Paid Tech Worker post:

Make it sustainable

Dear High Paid W2 Tech Workers (except Rohan),

You might be better off spending more.

Working at a FAANG can be a grind. Find ways to make it sustainable. This can include things like spending more money on making it sustainable.

Imagine ways that you could spend an extra $1,000 per month that would make your life more enjoyable. If spending that extra $1,000 makes it so you can work your FAANG job two weeks longer, it would be worth it.

This includes using your damn vacation. There are too many burnt out tech workers sitting on a maxed out PTO balance.

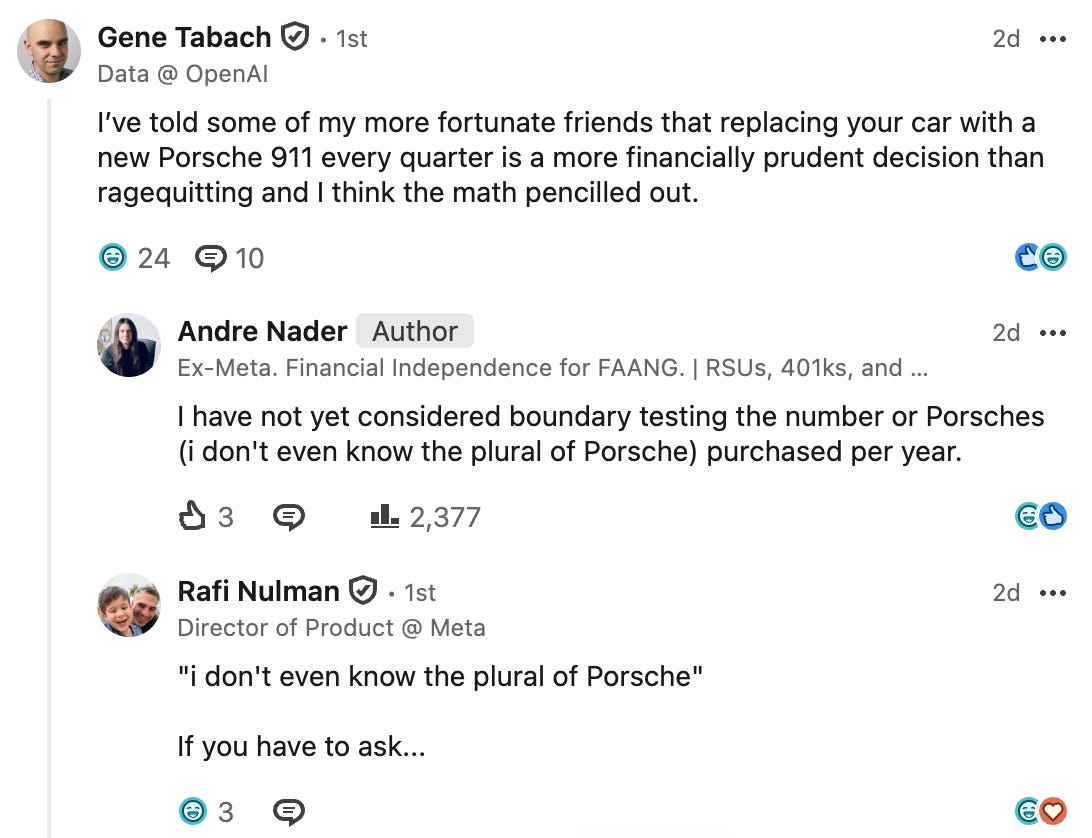

The theme of spending to make the FAANG grind sustainable clearly resonated with many of you and generated some great comments over on LinkedIn last week.

But I think there is another layer here worth exploring, particularly as you approach FIRE. As you get closer to your enough number, the question starts to change.

It is no longer: What can I spend money on to make work more sustainable?

It becomes: What can I spend money on to make my life meaningfully better?

The Shift to Spending for Happiness

That shift from sustainability to happiness is what I have been experimenting with this year.

Experimenting is the key word. That is the moment to begin testing which expenses actually improve your life.

You want to learn whether you enjoy business class flights before you FIRE, not after. If your enough number does not factor in that expense, then you are making a sacrifice. That sacrifice may be worth it, but you should know that before you lock in your enough number.

Boundary Testing For FIRE

This is where the idea of Boundary Testing comes into play.

In addition to being a lifelong optimizer, I also spent a decade focused on Growth at Facebook. I have been hard wired to approach things with a “Growth” lens. One of the tools that we used to grow products at Facebook often involved running boundary tests. This lets you understand what the maximum potential metric driver a specific growth lever could be and more importantly allows you to learn “when does adding more of that lever stop being incremental”. This is critically important when it comes to prioritizing which projects your team should be invested in, with a focus on driving topline metric impact.

Enough of the growth lesson. What does any of this have to do with FIRE?

At the end of the day it is all about maximizing a metric. In this case though, the metric I want to be optimizing is “Lifetime Enjoyment”, or lifetime utility for the economics folks, and the lever I am pushing is “spend”.

Pick one category of spending and test it intentionally.

What categories should you experiment with? You tell me. What are things you personally enjoy? Travel, hobbies, coffee, restaurants, donating to charities…

Don’t make this feel like work. This is supposed to be fun.

If you are telling me you have something that you love to do, but the thought of spending more money doing that stresses you out… that is also a really good realization to have before you FIRE. If this is the case I would encourage you to test spending more on mental health. Which I promise you will be easier to spend on while you have baller FAANG health coverage.

Remember, this isn’t a carte blanche permission slip to spend frivolously. Be disciplined in your approach. Spend explicitly.

Do This Before Your FIRE

I highly encourage you to run these boundary tests while you are still working full time. It is extremely common for all retirees to struggle with the transition from accumulating assets to spending down their assets. You are just increasing the amount of struggle by telling yourself that during your early retirement you will be comfortable increasing your spend even more.

The way I think about it is that spending more while you are working can help give you even more confidence in your final enough number and how long you need to keep working to really FIRE the way you want.

Not to mention the simple fact that it will be mentally easier to spend more while you are still earning a steady salary.

This is especially important if you are like me and come from a frugal background where saving money is easy but spending it is hard.

My Travel Spending

One area of spend that I have consistently struggled with is travel.

I really want to increase my annual spending on travel and experiences with my family. But wanting to spend more and actually spending more are two different things.

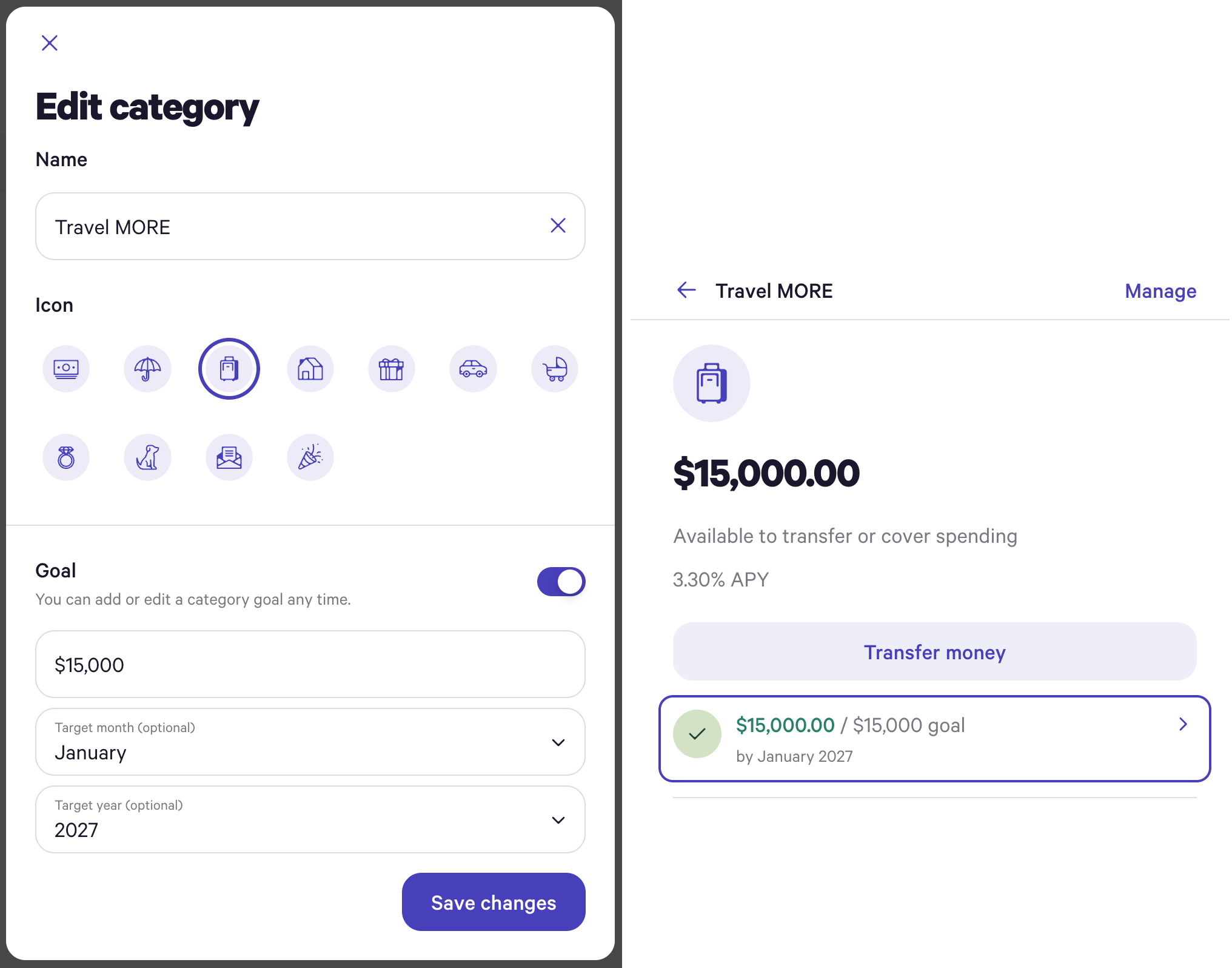

To help me be more intentional, I created a dedicated travel category inside my Wealthfront Cash Account and pre-funded it with money I actually want to spend on travel this year.

The goal isn’t to let that balance sit at $15,000 forever. The goal is to make the money feel intentionally available for the travel plans I already decided I want to fund.

In a weird way, the “goal” is to get that category down toward $0 by the end of the year. Not because I want to spend money just to spend money, but because the whole point of the spend goal is to help me actually follow through on spending that aligns with the life I want.

Then, in January 2027, I’ll refill it back to whatever my 2027 travel goal ends up being.

If you end up opening a Cash Account to set your own goals, use Wealthfront.com/Andre for an extra 0.75% APY boost for three months on up to $150,000 for new clients and get another 0.25% APY increase with direct deposit ($1,000/mo) and maintaining a funded investing account

Travel is just one category. The point is not that everyone should spend more on travel. The point is that you should be testing the categories that matter to you before you lock in your enough number.

I don’t want to adjust my lifestyle to fit my enough number; I want my enough number to reflect the lifestyle I want to be living.

If you are getting close to your FIRE goals, you should be testing what spending more feels like.

It is infinitely easier to just work another year than it will be to realize your “enough” number doesn’t finance the type of life you really find fulfilling.

Homework

Pick one category in the next month. Double your spend on it, upgrade it, or pre-fund it.

Then ask: did this actually improve my life enough to deserve a permanent place in my enough number?

I’ll leave you this LinkedIn comment thread that I really wanted to include in this post:

Disclosures: Andre Nader is a Wealthfront client and was compensated ~$3,330 for the testimonial and promotion of the Wealthfront Cash Account. This compensation creates a conflict of interest. Experiences may vary among Cash Account clients, and results are not guaranteed.

The Cash Account, which is not a deposit account, is offered by Wealthfront Brokerage LLC (”Wealthfront Brokerage”), Member FINRA/SIPC. Wealthfront Brokerage is not a bank. The Annual Percentage Yield (”APY”) on cash deposits as of January 30, 2026, is representative, requires no minimum, and may change at any time. The APY reflects the weighted average of deposit balances at participating Program Banks, which are not allocated equally. Funds in the Cash Account are swept to Program Banks where they earn a variable APY and are eligible for FDIC insurance. Conditions apply. For a list of Program Banks, see: www.wealthfront.com/programbanks. FDIC pass-through insurance, which protects against the failure of Program Banks, not Wealthfront, is not provided until the funds arrive at the Program Banks. While funds are at Wealthfront Brokerage, and while they are transitioning to and/or from Wealthfront Brokerage to the Program Banks, the funds are eligible for SIPC protection up to the $250,000 limit for cash. FDIC insurance is limited to $250,000 per customer, per bank, regardless of whether those deposits are placed through Wealthfront Brokerage. You are responsible for monitoring your total deposits at each Program Bank to stay within FDIC limits. Wealthfront works with multiple Program Banks to make available up to $8 million ($16 million for joint accounts) of pass-through FDIC coverage for your cash deposits. For more info on FDIC insurance coverage, visit www.FDIC.gov.

The Direct Deposit Plus Investing Program from Wealthfront Advisers LLC and Wealthfront Brokerage LLC provides eligible clients a 0.25% APY increase above the base APY on eligible Cash Account balances (up to an overall boosted rate of 4.30% for a limited time when including the three month 0.75% APY boost for new clients) when you direct deposit $1,000 a month, plus open, fund, and maintain an investing account. Wealthfront may change or end the program at any time and determine eligibility at its discretion. Terms apply. Full details at wealthfront.com/promo-terms.

Good stuff here! Appreciated the note on who this post is and *isnt* for. Loved reading through