Pro-Rata Rule & Backdoor Roth IRAs Simplified

Hey FAANG FIRE!

Backdoor Roth IRAs are great.

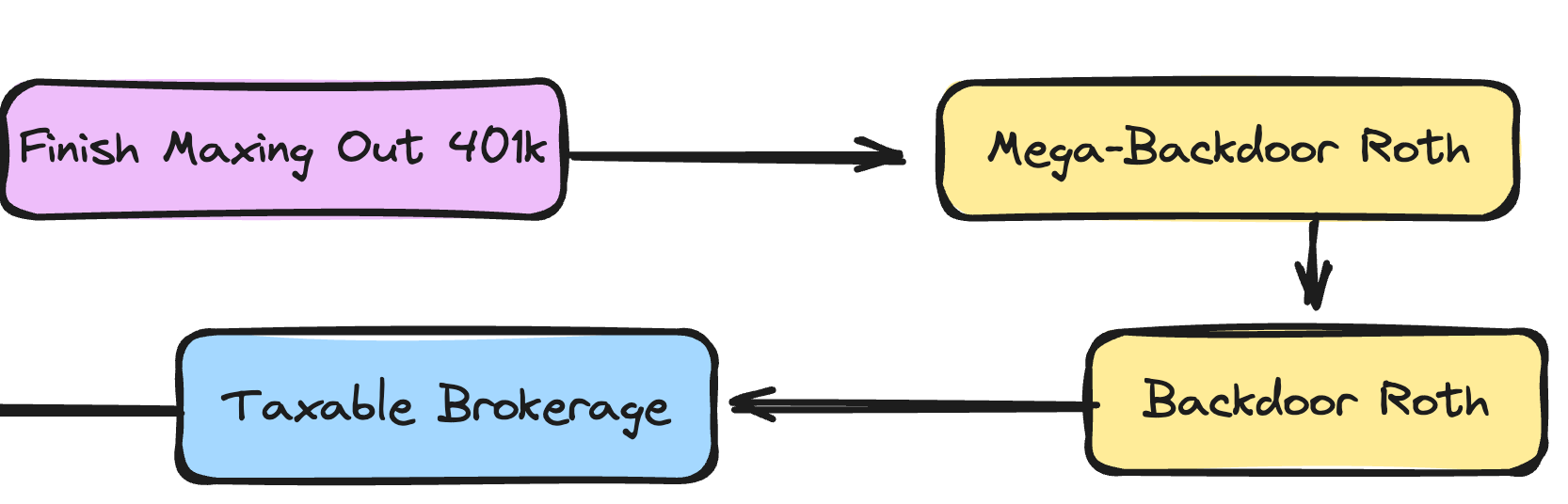

In my cashflow prioritization waterfall I have the Backdoor Roth just behind the Mega-Backdoor Roth.

The Backdoor Roth allows high income earners to get an additional $7,000 per year into their Roth IRAs, where the funds and any growth will not be taxed when they tap into the account in retirement.

If you have already maxed out your full 401k, all $70,000, the $7,000 you can contribute into a Backdoor Roth IRA is a nice cherry on top before you start building up your taxable brokerage account.

There is one major issue that tends to get everyone tripped up though, the pro-rata rule. I wanted to dive into the specifics of the pro-rata rule to help y’all understand why it causes issues.

Posts about Roth IRAs will typically say something like "If you want to contribute to a backdoor roth, make sure you don't have any funds in a Traditional IRA or Rollover IRA due to the pro rata rule. An easy way to do this, is to roll your Rollover IRA or Traditional IRA into your current workplace 401k." In fact I said exactly that in my entire guide walking through the entire backdoor roth process.

I realized that this still glosses over the "why". Leading to confusion and a tendency to overcomplicate things.

Let’s fix that so we can all understand.

Disclaimer: There is a lot of nuance. It is always a good idea to consult a tax professional.

First, A Recap on the Backdoor Roth:

A Roth IRA is a tax-advantaged account where after-tax funds can grow tax free and be withdrawn tax free in retirement.

In 2025 the contribution limit is $7,000.

If you earn more than $150k single or $236k married you can’t contribute directly to a Roth IRA.

A “Backdoor” Roth IRA involves making a nondeductible contribution to a traditional ira and then converting those funds into a Roth IRA.

This allows high earners to effectively fund $7,000 per year into a Roth IRA despite any income limits on direct contributions by going through the backdoor of a traditional ira.

The important caveat is that you want to make sure you have $0 in all traditional ira and rollover ira accounts by the end of the year or else you will be subject to the “pro rata rule”.

Again, I have a full walkthrough of the backdoor roth ira process including dealing with existing rollover iras available:

Pro Rata In More Detail

Let’s address the Pro-Rata Rule. What is so painful about the Pro-Rata rule that makes it not worth doing the Backdoor Roth?

Instead of an explanation, let’s walk through an example:

Brandon hits the pro-rata rule

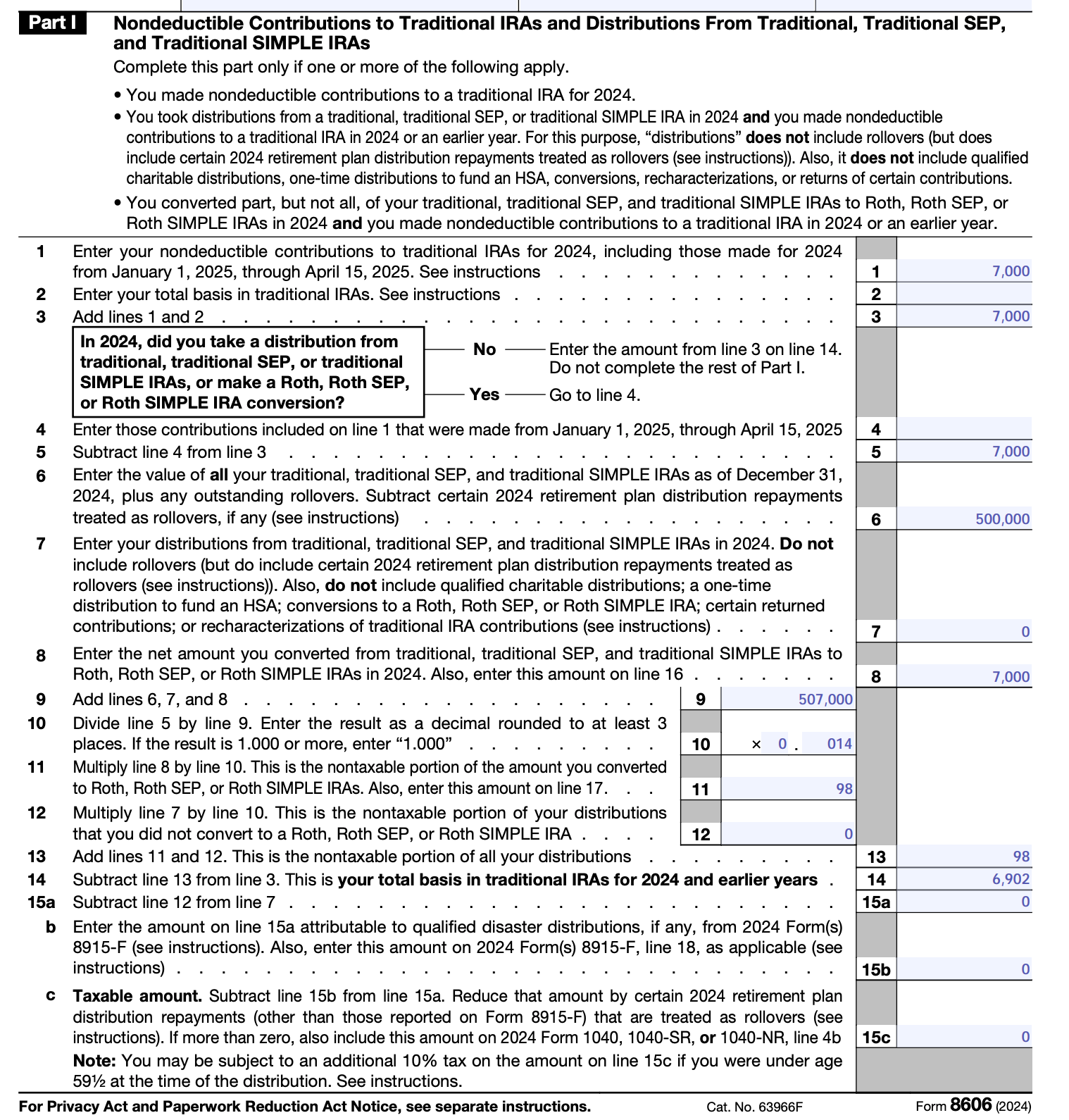

Let's say in 2024 Brandon has $500,000 in a rollover ira from a past employer. He heard about this "back door roth" thing and created a new traditional ira, contributed $7,000 and then converted it to a Roth IRA.

Then in April 2025 Brandon is doing his taxes and is greeted with not so fun surprise.

Instead of the $7,000 of After-Tax funds being converted into a Roth IRA, tax free he seems to have accidentally created a more than $2,400 tax bill.

This is the day Brandon learns about the Pro Rata Rule.

Instead of that $7,000 being converted into a Roth IRA tax free, nearly all of it was taxed!

The Pro-Rata Math Broken Down

The IRS wants you to "pro rate" the conversion across all your traditional ira and rollover ira accounts. This only applies to pre-tax IRA accounts, not 401ks.

The Math Behind Brandon’s Tax Bill:

Total Balance Across All Pre-Tax IRA Accounts: $500,000 + $7,000 = $507,000

Prorated Percent Converted: 1 - ($7,000/$507,000) = 98.6%

Taxable conversion: 0.986 * $7,000 = $6,902

Federal Tax Bill: Marginal Tax Rate * $6,902 (which is 35% federally or more if Brandon has an adjusted gross income of more than $250k and is single)

So $6,902 out of the $7,000 Brandon converted is going to be coming from the pre-tax funds in his Rollover IRA causing the $6,902 to be taxed at his current marginal tax rate! That could be >$2,400 in taxes at the federal level alone!

My non-CPA attempt to show how this would look on Brandon’s actual tax forms.

Avoiding the Pro-Rata Rule:

Brandon’s entire tax bill could have been avoided if he simply moved all of his prior rollover ira funds into his workplace 401k before the end of the year!

Let me repeat that. You want to end the calendar year with a $0 balance in all Traditional and Rollover IRAs by the end of the year to avoid the pro-rata rule.

This is a simplified example. But hopefully you now understand the pro-rata just a little bit more.

In this example, Brandon technically still has $6,902 of After-Tax funds in your Traditional IRA. He should still be able to move those funds into his ROTH IRA, assuming he finally moves that rollover IRA into his employer 401k.

If this has happened to you, don’t beat yourself up about it. It is a very common mistake! On the bright side, you essentially just did a normal Roth Conversion on those funds. You won’t ever have to pay taxes on the rolled over amount. Most people just wait until they are not in FAANG employee tax brackets before they do that :).

As always, it is a good idea to talk to a tax professional who can discuss your specific situation.

What if you have a rollover ira but don’t have a current employer 401k?

In order to contribute to a Backdoor Roth IRA you need earned income. If you have earned income from earlier in the year or income from your personal entrepreneurial endeavors there is still a way. Since you don’t have a current employer 401k, you can look into a Solo 401k as a potential option.

By opening a Solo 401k, you now would have an account you can move your Rollover IRA funds into before the end of the year. I would not wait until the end of the year to do this since it can take a little bit of time. I personally use Carry (affiliate link) for my own Solo 401k since they were one of the few providers that made it easy to also contribute to a Mega Backdoor Roth IRA. You can also get a free year of Carry by joining the Extra Guac tier, instantly paying for itself.

Proof I actually use and personally pay for Carry:

Congrats, you now understand the pro-rata rule more than 98% of FAANG employees. It is a very fun party conversation :).

While we are on the topic of Backdoor Roth IRAs, I would be remiss to call out one of the most common tax mistakes of incorrectly entering a Backdoor Roth IRA even when you are not dealing with the pro-rata rule. I wrote on that topic when discussing the Holy Trinity of Common Tax Filing Mistakes.

-Andre

What about post-tax funded Traditional IRA accounts? Are those subject to the pro-rata rule as well?