Getting my cash in order

Earlier this year my wife asked me two simple questions:

“Where is our money?” and “Help me understand it.”

Not being able to clearly explain my web of accounts pushed me to simplify our entire financial setup. A key part of that was rethinking how we handle our emergency fund.

Today’s newsletter is sponsored by Wealthfront.

One of my 2025 goals was to simplify my financial life. Wealthfront is a key part of that simplification. I have been a Wealthfront customer since 2020.

My high-yield Cash Account at Wealthfront has consistently been among the highest Annual Percentage Yield (APY). Their website is designed for how we actually manage money today, not a legacy bank bolting on features.

Right now, you can get an extra 0.50% APY for three months on up to $250,000, for a total 4.25% variable APY from program banks when you open your first Cash Account using my link.

Go to wealthfront.com/andre. Promotional terms and conditions apply. See our affiliate link for more details.

Evolving My Strategy

Over the past few years I’ve written about my tiered emergency funds, the savings prioritization waterfall, and the need for simplification. This year, I finally put all of those lessons into practice and made some changes.

I really wanted to simplify things. I wanted to be able to easily explain to my wife why we had each account. I wanted to make it easy for her to take over if something happened to me.

That doesn’t mean there isn’t some smart optimization happening. Just that every account needed to earn its place.

Shedding the dead weight

I went on an account closing spree:

Three random Fidelity checking/savings accounts → closed.

Fidelity brokerage link account → closed.

Ally Invest account → closed.

Multiple Chase accounts → closed.

Citi checking account → closed.

Efficiency, simplicity, and easy explainability were the core goals.

At one point, the “return on hassle” for juggling accounts and playing the points game made sense. But in 2025, the payoff wasn’t worth the mental clutter.

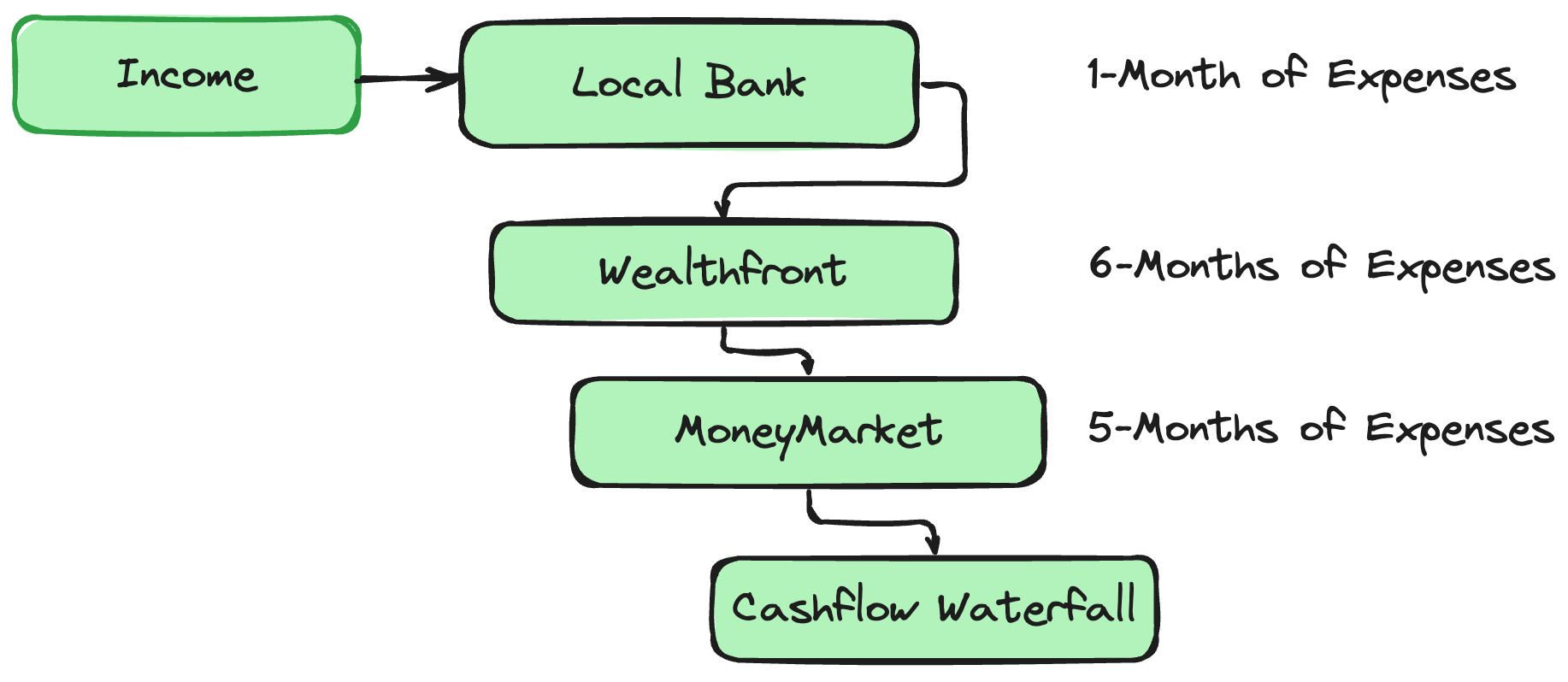

One Core Checking Account: 1-Month Expenses

Now things are simple. I keep one checking account with one month of expenses. This is where my wife’s W-2 income gets deposited, our credit cards get paid off, and the rent goes out.

I like having a bank account with a physical branch for those rare moments when you need to walk in (you know who you are, requesting a medallion signature in 2025). There doesn’t need to be anything special about this account; it just needs to be nearby and not require maintaining a large balance to avoid fees.

Building the Real Buffer: 6-Months Expenses

Back in 2023, my tiered approach to rainy day funds meant keeping 2–3 months of expenses in my Wealthfront Cash Account as part of my “tier 2”. A lot has changed since then.

Today, I’ve moved closer to a one-year cushion for my overall emergency fund. That shift makes sense for my family as we are now a single-income household.

Even with millions in a taxable brokerage, I prefer having my emergency fund extremely liquid. When I am fully FIRE, I’ll transition this bucket to be where I will hold 6-months of my annual portfolio withdrawals (see the math 3% withdrawal rate math here).

What hasn’t changed is where I keep the bulk of those reserves. I keep the first six months of my emergency fund in my Wealthfront Cash Account, these are the dollars I’d immediately tap into.

I’m currently earning a base 3.75% APY on my Wealthfront Cash Account without needing to jump through hoops. The APY has consistently remained competitive even as rates shifted over the past five years, solidifying my original reason for utilizing them.

Too many people let their savings sit idle. It physically hurts me when I see friends with large sums sitting in their checking accounts earning nearly 0%. I prefer keeping a portion of mine in an account that earns a competitive yield while still being easy to access.

If you end up signing up, don’t forget to use Wealthfront.com/Andre for an extra 0.50% APY for three months.

Tax-Aware Secondary Buffer: 5-Months Expenses

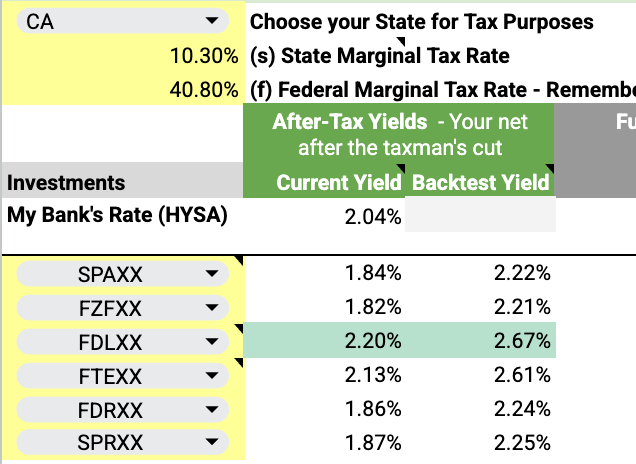

I keep the rest of my emergency reserves in money market funds at my primary brokerage. The reason for the change here was that I started thinking less about the posted yield and more about the after-tax return that really matters.

For a high-income household in California, roughly half of interest income goes to taxes.

Key Takeaway: Interest rates alone don’t tell the entire story.

I am currently holding the remaining 5-months of my emergency fund in a money market fund. The specific one that makes sense for me might be different than the one that makes sense for you.

I use FDLXX (VUSXX is the Vanguard equivalent) because it primarily holds federal treasuries, making the interest exempt from California state taxes. If I lived in a state without income tax, the municipal money market comes out ahead (FTEXX).

Yields shift daily, and some weeks the muni fund wins, other weeks the treasury fund does. I don’t over-optimize this. The goal is simply to earn a competitive, tax-aware return on cash I might not need for months.

I am going to this level of detail because some people treat their emergency fund as a catch-all excuse for holding too much cash. It starts as six months of expenses and quietly grows into more than a year of idle money.

Knowing Thy Numbers

Many people I talk to have very round numbers for their emergency fund. Fifty thousand. One hundred thousand. When I hear that, it usually means they have not done the math.

The more arbitrary the number, the more hesitation there tends to be around investing the rest. It is often a sign they are not confident their emergency fund would actually cover them in a real emergency.

That is why it is so important to know, with precision, how much your current lifestyle costs each month. Know your fixed costs. Know your discretionary costs. For me, my emergency fund is based on our current lifestyle. I don’t want to have to change anything if something goes wrong. Maybe you would be willing to cut back a little more, but it still comes down to knowing your numbers.

Some third-party tools I use to help me understand my numbers.

The Simplification Payoff

In the past, I had three separate “tiers” of emergency funds, multiple banks, and accounts scattered across the landscape. Today, it’s distilled down to:

One local checking account with 1 month of expenses.

Wealthfront with a 6-month of expenses.

Brokerage money markets for tax-efficient overflow with 5-months of expenses.

That’s it. Clean. Simple. Easy to explain to my wife, easy to manage, and easy to access if something goes wrong.

How do you have your emergency fund set up? Leave a comment or reply to this email and let me know.

Disclaimer: Andre Nader is a Wealthfront client and was compensated $5,000 for the testimonial and promotion of the Wealthfront Cash Account. This compensation creates a conflict of interest. Experiences may vary among Cash Account clients, and results are not guaranteed.

The Cash Account, which is not a deposit account, is offered by Wealthfront Brokerage LLC (”Wealthfront Brokerage”), Member FINRA/SIPC. Wealthfront Brokerage is not a bank. The Annual Percentage Yield (”APY”) on cash deposits as of September 26, 2025, is representative, requires no minimum, and may change at any time. The APY reflects the weighted average of deposit balances at participating Program Banks, which are not allocated equally. Wealthfront Brokerage sweeps cash balances to Program Banks, where they earn the variable APY.

If you are eligible for the overall boosted rate of 4.25% offered in connection with this promo, your boosted rate is also subject to change if the base rate decreases during the three-month promotional period.

It's so awesome that you're transparent with how much you were paid for an ad, and CoIs! I've always been curious how much influencers get paid :)

Why do you still have three tiers - why not just go with either Wealthfront or the money market? Is it about having more in an FDIC bucket?