The Marriage Penalty Impacting FAANG

Would you consider not getting married to your partner for an extra $10,000 per year?

That is a very real question that high earning dual income couples can face. The issue has to do with how the US federal tax brackets are set up. At higher income levels the size of the tax brackets for a married household is not double that of a single earner.

When the total income taxes paid for a married couple exceeds the amount they would have paid if they were single, then they are experiencing The Marriage Penalty.

The Trump era Tax Cut & Jobs Act (TCJA) greatly reduced the size of the marriage penalty, however it still very much exists for many dual income FAANG couples.

The Marriage Penalty is most common for high earning couples who both earn similar amounts, especially when combined incomes are above $731,200 (the 37% tax bracket).

Another factor is a 0.9% additional medicare tax which single filers begin to pay at incomes above $200,000, while the tax starts at combined incomes of $250,000 for those married filing jointly.

On the other hand, when a couple has large differences in incomes, they are more likely to pay less in income taxes when married, leading to what is called The Marriage Bonus.

Interesting Side Note: As of 2020, California residents have an interesting workaround; they can become registered domestic partners instead of getting married. This gives them the benefits of marriage in California while still allowing them to file your federal taxes as two separate single individuals. This was previously only available to same-sex partners in the state of California with the bill SB 30 expanding the eligibility of RDPs to all couples.

Please don’t change your life on these calculations. These are overly simplified estimates of federal taxes based only on the tax brackets, standard deductions, and medicare surcharge taxes. There are countless variables that are not accounted for.

The Marriage Penalty at FAANG Incomes

While much has been written on the Marriage Penalty and Marriage Bonus previously. I haven't seen a deep dive into specific scenarios that FAANG workers are likely to encounter.

Let’s start with an example at the higher end of the income spectrum to illustrate the marriage penalty:

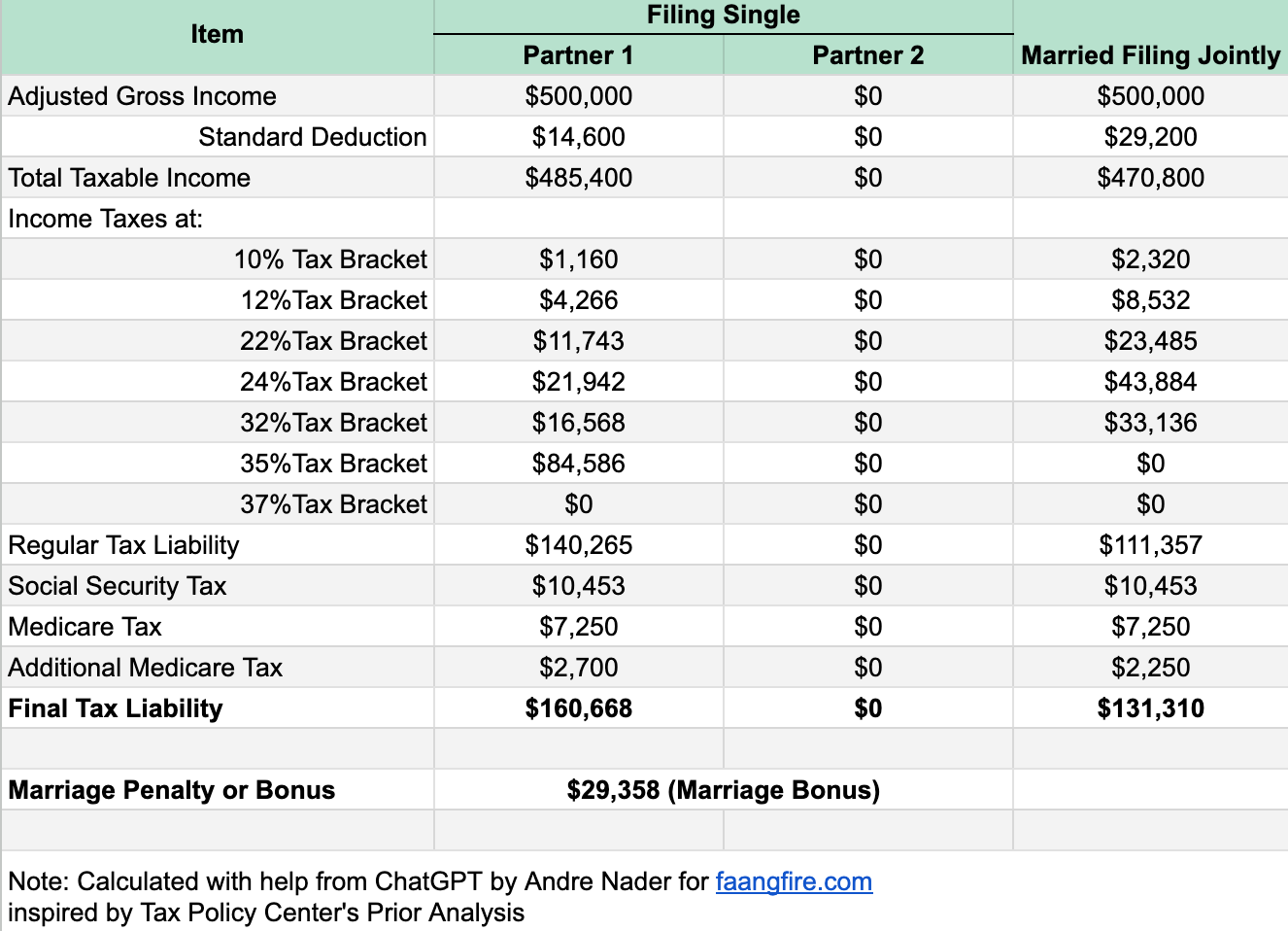

Two high earners making $750,000 each would pay an additional $11,102 at the federal level in taxes if they were married.

Remember, the marriage penalty is most extreme when both earners make around the same amount of income.

Let’s change the ratio away from an equal 50/50 split to a 70/30 split. Where one earner makes $1,050,000 and the other $450,000.

Total income taxes paid as two single filers: $473,947.63

Total income taxes paid as a married household: $481,569.88

Increase in taxes due to being married: $7,622.25

Going from a 50/50 split to a 70/30 split diminishes the marriage penalty by nearly $3,500 per year.

As you begin to shift the distribution of the income away from an equal 50/50 split, the marriage penalty begins to diminish and can turn into a substantial marriage bonus.

What happens when 100% of the income is earned by one of the workers.

Total Federal Income Taxes Paid as Two Single Filers: $520,667.50

Total Federal Income Taxes Paid as a Married Filing Jointly (MFJ) Household: $481,569.88

Decrease in Federal Income Taxes by Being Married: $520,667.50 - $481,569.88 = $39,097.62

In the case of large differences in earnings, the marriage penalty becomes The Marriage Bonus.

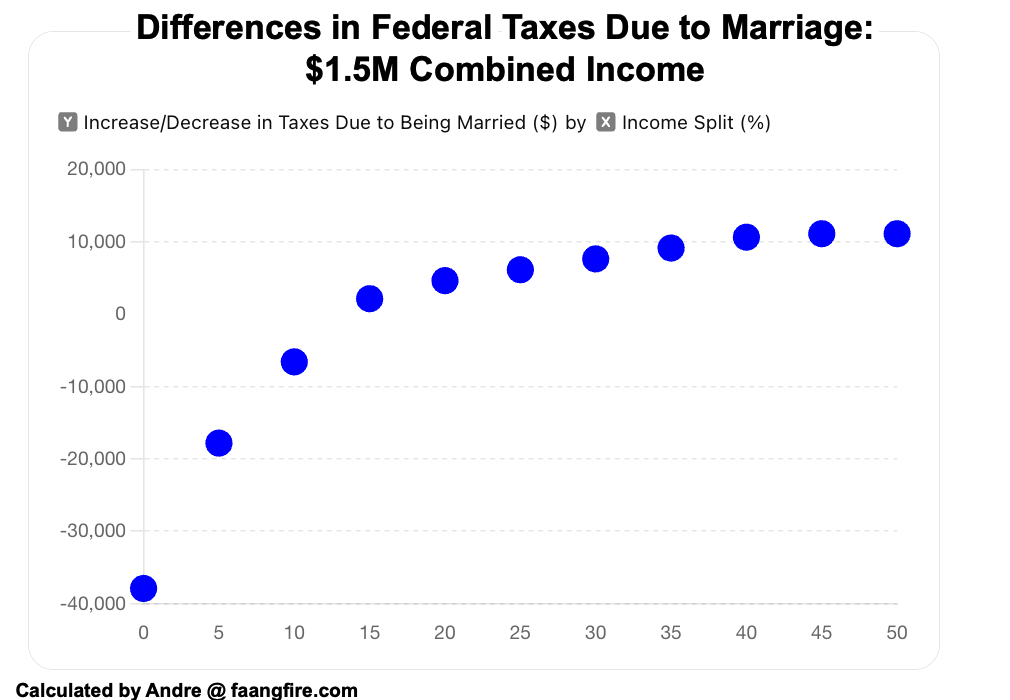

Here is what it looks like when we compute the marriage penalty/bonus due to being married for a household who earns $1,500,000 across the range of income splits.

$1,500,000 Total Income

Ratio when Marriage Penalty Begins: 14%/86%

High Income Earner: $1,290,000

Low Income Earner: $210,000

Increase in Taxes Due to Being Married: $1,372.15

Now, while a combined $1,500,000 is certainly possible within a FAANG setting. It definitely represents the higher end of the spectrum. Lets look at $500,000 in total income across different splits.

$500,000 Total Income

Ratio when Marriage Penalty Begins: 41%/59%

High Income Earner: $295,000

Low Income Earner: $205,000

Increase in Taxes Due to Being Married: $126.68

So now we find that in the vast majority of cases having $500,000 in combined income leads to a household experiencing a “marriage bonus”.

Looking at the two prior examples together with an additional $750k income breakdown.

Additional Marriage Penalties

Up until this point we have been primarily looking at federal income taxes and the additional medicare tax.

Most deep dives into the marriage penalty stop here (most actually stop before factoring in the Medicare Surcharge). I wanted an even more comprehensive look that also factored in social security taxes and medicare taxes which all W2 workers would also be paying.

Note: These calculations still assume both individuals are taking the standard deduction and do not have kids. There are instances of itemizing that are not covered in addition to factoring in Head of Household for one partner if they have children.

Examples of Marriage Penalty

Scenario: $1,500,000 split 66.6/33.3

Partner 1: $1,000,000

Partner 2: $500,000

Marriage Penalty: $8,621

Scenario: $850k split 35/65

Partner 1: $300,000

Partner 2: $550,000

Marriage Penalty: $3,142

Scenario: $800k split 50/50

Partner 1: $400,000

Partner 2: $400,000

Marriage Penalty: $2,143

Example of Marriage Bonus

Scenario: $500k Split 100/0

Partner 1: $500,000

Partner 2: $0

Marriage Bonus: $29,358

Reader Story

I was fascinated when FAANG FIRE reader, Sagar Manda, reached out to me detailing how he and his wife were utilizing California’s Registered Domestic Partnership status as a way to avoid the federal marriage penalty. He gave me his permission to share this real example to highlight that this is very much something couples grapple with.

As we prepared for our wedding back in late-2021, our minds were at ease knowing that the TCJA had eliminated most marriage penalties. My two rental properties left me with approximately $30,000 of itemized deductions from mortgage interest and SALT. My fiancé took the standard deduction. We had wrongly assumed that married-filing-separately (MFS) would allow us to avoid any resulting marriage penalty until I discovered the following on the IRS website:

“If you and your spouse file separate returns and one of you itemizes deductions, then the other spouse must also itemize deductions.”

Separate returns would not save us from a marriage penalty exceeding $4,392.

Our total deductions came to $42.5k ($30k itemized + $12.5k standard), which was destined to be reduced significantly if we married. Our only options would be to itemize $30k of deductions or take the $25k in standard deductions which would result in $12,550 more taxable income.

The value of the standard deduction for the median big tech employee at $12,550 * 35% marginal rate = $4,392/year. Today’s standard deduction of $14,600 is worth $5,110/year in the same bracket.

Losing this deduction by marrying someone who itemizes is far from romantic and caused me to even consider selling my rentals.

My wife and I view marriage as a social institution, so we felt no pride in the IRS recognizing our marriage and then charging us for the privilege. We began looking for alternatives and stumbled upon news articles describing how California’s 2020 SB30 legislation opened a path for opposite-sex couples to utilize registered domestic partnerships (aka civil unions) previously reserved to same-sex couples. This would allow us virtually every legal and financial benefit of traditional marriage without the drawback of a bigger bill from the IRS. We decided to give it a try and it has worked out great. Every year, we file a joint return for the state of CA and two single federal returns. This October, we will celebrate our third anniversary with no regrets!

-Sagar Manda in California

Closing Thoughts

A few other considerations you should be thinking about if you are wanting to go deeper into this topic:

State Taxes: Each state has different taxes. Some do not have a marriage penalty/bonus while others do.

Kids: The introduction of kids also adds the potential to have one partner file as Head of Household which can be more favorable than filing Single.

Tax laws are constantly changing. If the TCJA expires in 2026 then the marriage penalty could once again increase even more across all income levels.

If you have significant itemizations it could be even more advantageous to have one person filing single and the other taking on all the itemizations over the standard deduction.

Marriage in the US comes with a significant number of legal benefits/implications that should be factored in.

It is ridiculous that a marriage penalty exists at all. There shouldn’t be a financial incentive to dissuade couples from getting married. Yet, here we are. I always encourage my audience to understand the financial implications behind their decisions… while also factoring in the non-financial. In this case, I would highly encourage you to add a significant weight to the non-financial side. I view my marriage as one of the greatest force multipliers on my path to FIRE. Being dual income with no kids, sharing a 1 bedroom apartment, while both of us were working in big tech greatly accelerated my FIRE plans.

As a non-working spouse to a tech worker, I confidently let my wife know that by being married to me I was saving the house a significant amount of money. To which she quickly reminded me that if I was also working, we would be making even more net of taxes.

Touché.

Are those sheets shared above available? Thanks

Interesting, hadn't considered this. Though for a couple that makes $1.5M I think they'll survive if they had to pay another $11k :)