The Crossover Point: Passing the 50% Growth Milestone

This is the final FAANG FIRE post of 2025!

I just finished wrapping up an 80 degree Texas Christmas at my in-laws and thought it would be a good time to reflect back on the year.

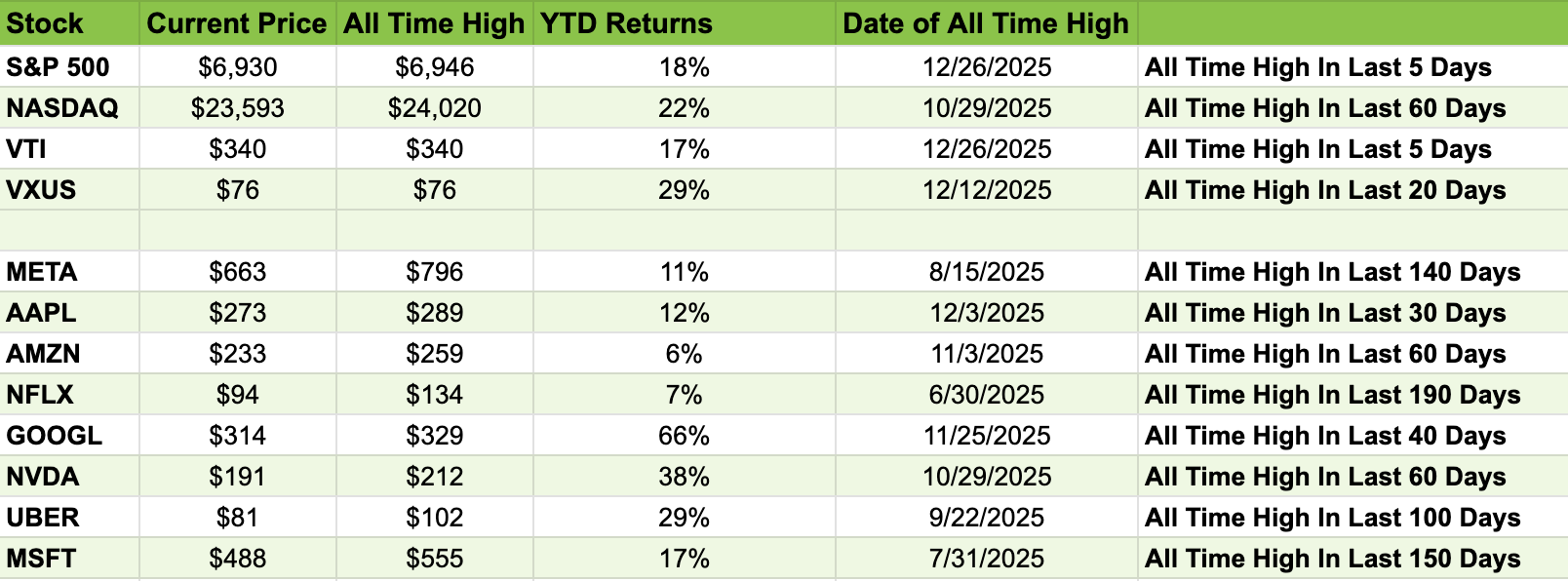

2025 by the numbers

It has been another good year for the financial markets. We are closing the year near all-time highs for the overall US markets (VTI up 17% YTD) as well as international markets (VXUS up 29% YTD). While all FAANG companies reached all-time highs during 2025, many hit the high water mark earlier in the year, while others who were lagging early in the year found their stride later in the year (looking at Google and Apple).

2025 by the vibes

The year didn’t feel as positive as the numbers suggest. It felt more like being a passenger in an Uber XL with a driver who has yet to master the gas pedal, the brake, or the concept of cruise control. There was clearly forward momentum, but the constant lurching was enough to churn even an iron stomach.

Yet here we are. The seemingly imaginary numbers on the net worth trackers are once again at all-time highs.

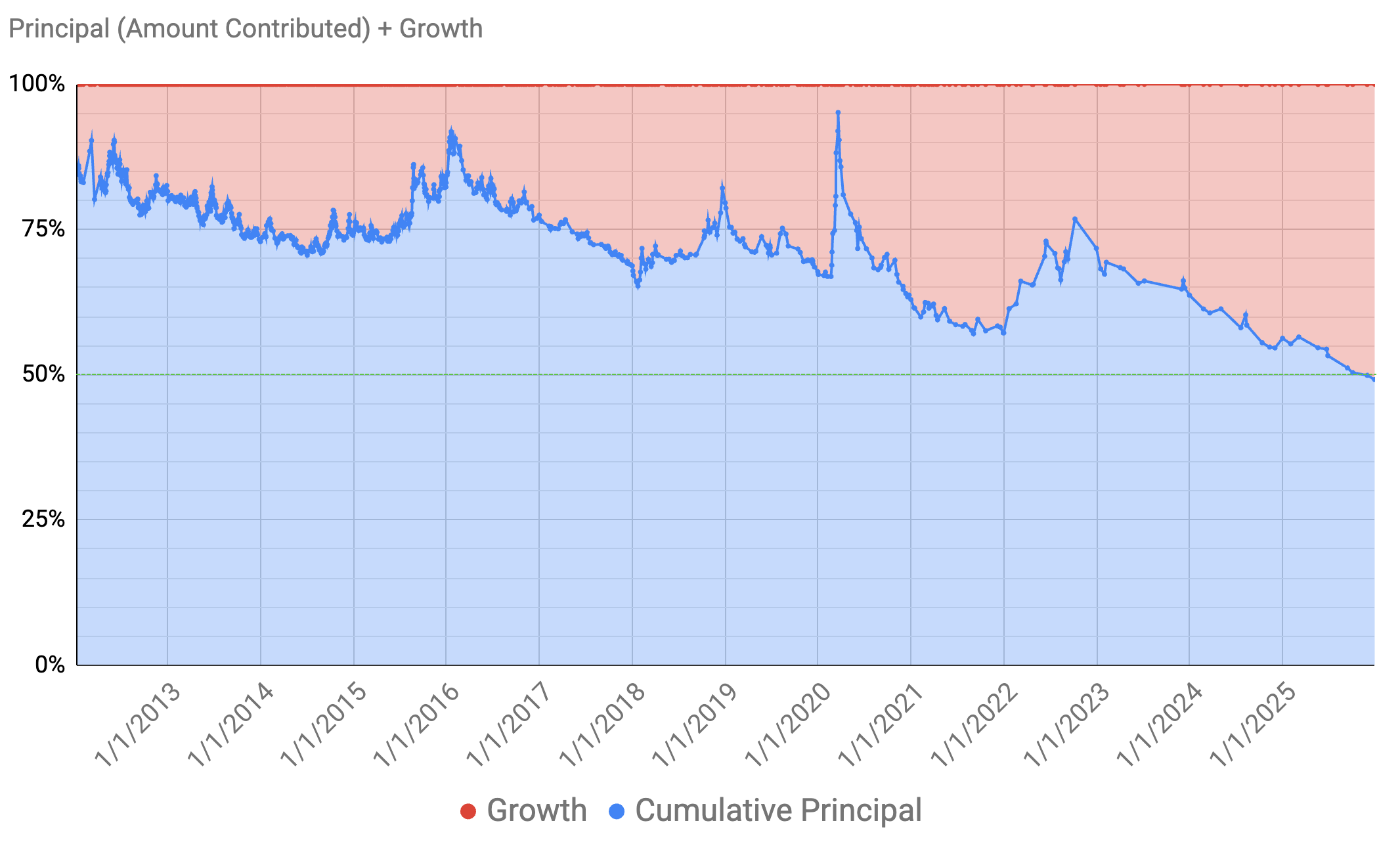

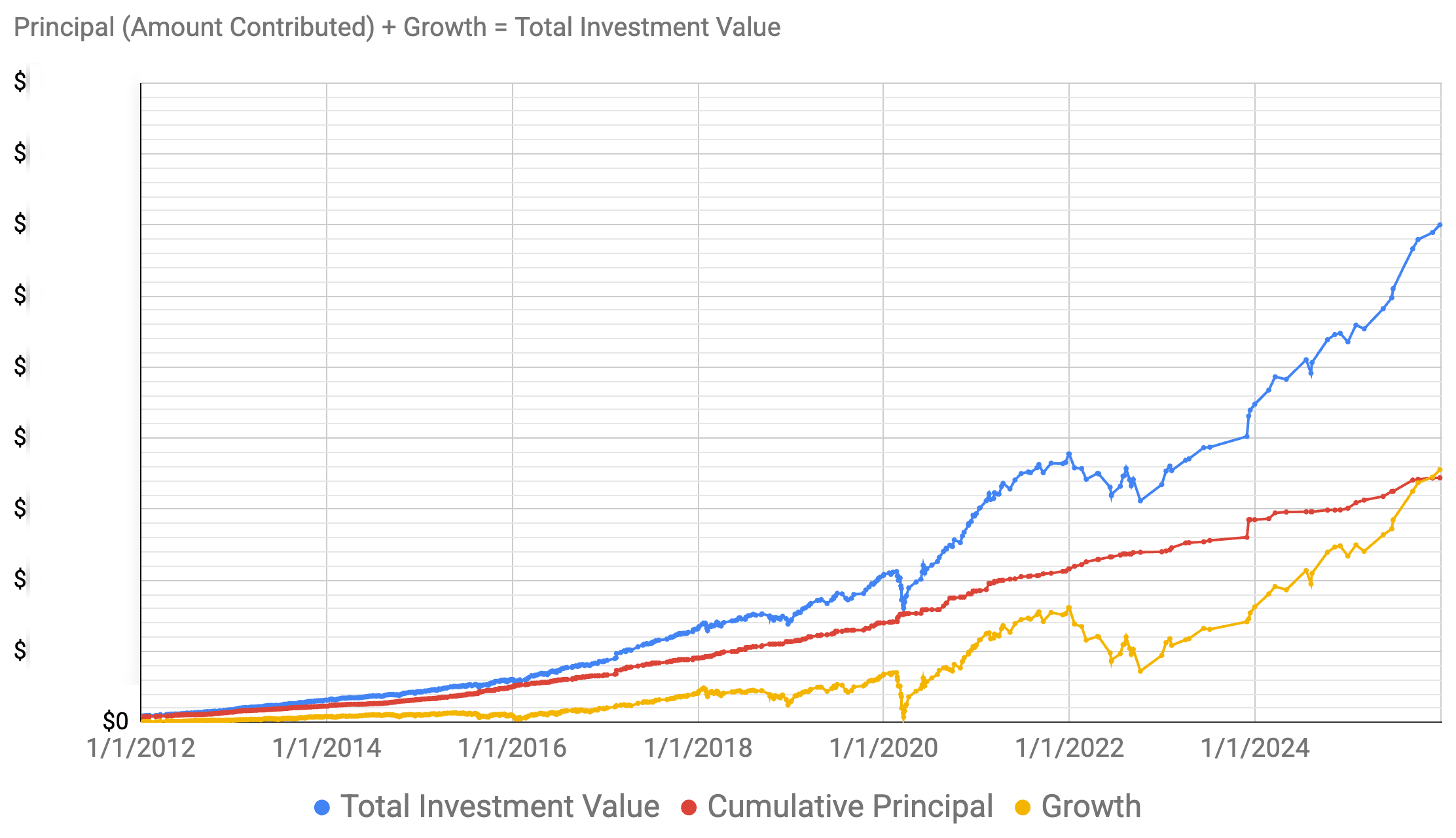

Growth vs Principal Milestone

Standing at these all-time highs makes it easy to forget the long, slow grind where market returns felt nonexistent and I constantly found myself asking: “Why isn’t it compounding?? Isn’t compounding supposed to be the eighth wonder of the world??”

It took me a few years to grasp the idea that compounding early on in your FIRE journey is drastically overrated. This is especially true for FAANG workers who have the ability to save significant amounts each year.

Like most FAANG workers, the primary driver of my net worth was simply how much I was able to invest. My contributions were all that mattered.

This is why I was surprised by a milestone I just hit. A milestone that has taken more than 16 years for my dual income tech household to hit.

2025 Milestone: More than 50% of my FIRE portfolio balance is currently coming from growth.

I never actually set a goal to hit this 50% growth mark.

That is primarily an output of the market, not something I can control. It’s simply an interesting data point I stumbled upon while updating my spreadsheets. The only reason I noticed it is because I was busy tracking the one number I do track religiously: my contributions.

Contribution Goals

Contributions is one of my favorite personal finance goal metrics. Most people gravitate to percent based goals, like “saving 50% of my income” or “net worth reached $500,000. I really hate percent based metrics and total volume metrics leave you at the whims of the market. For me a good financial goal should ladder up to my “Enough Number”, be motivating to track, be mostly in my control, and encourage the right long term behaviors. That is how I landed on total annual contributions for my primary yearly goal.

It is because I focused my goals on contributions that I started tracking my contributions on a regular basis.

So if you are looking for a good 2026 financial goal, my vote is on making it a contribution goal.

Now, contribution goals are not without flaws. The biggest one is that if you get compensated with a more variable income source like RSUs or bonuses then it can make hitting your goal not achievable due to no fault of your own. That is when you simply re-goal… who doesn’t love a good re-goaling exercise. This is your personal goal, nobody is going to give you a hard time about it other than yourself.

Financial Goals

Since we are heading into the new year and many of you are thinking about new year’s resolutions, I would encourage you to shift away from resolutions and focus on actual numeric goals.

My annual goals would typically look like:

“Contribute $200,000 into my FIRE accounts”.

This could be further broken down for 2026 (based on cash-flow waterfall):

$72k into my 401k

$72k into my partner’s 401k

$15,000 into our backdoor roths ($7.5k each)

$41,000 into our taxable brokerage

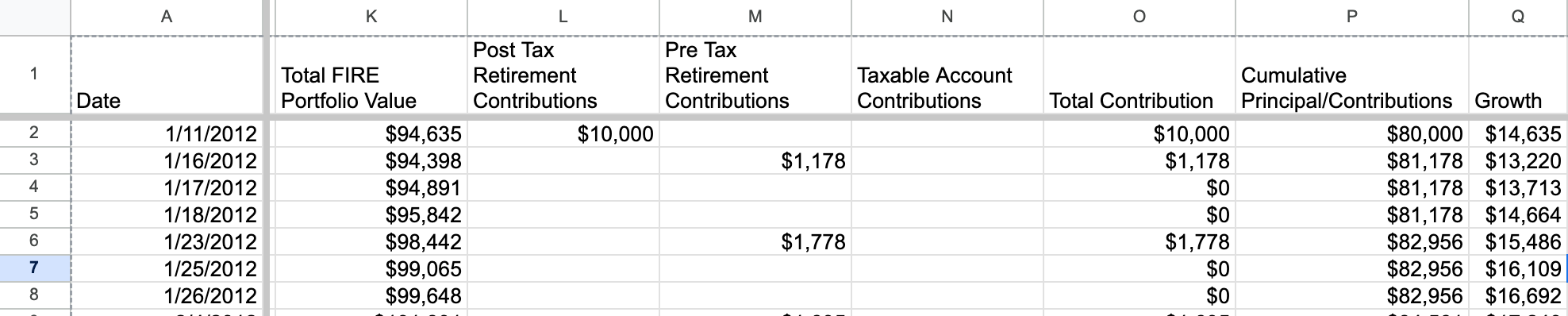

How I tracked contributions.

Another downside is that I have not yet found a good way to track this automatically. Instead, I relied on a Google Sheet I have been updating manually.

I only include contributions into “FIRE” accounts.

Only includes accounts that I based my Enough Number on.

Taxable Brokerage, Pre-Tax Accounts, and Roth Accounts (including HSAs)

Doesn’t Include Vested Company RSUs

This added an extra mental incentive to sell on vest and diversify, because otherwise it wouldn’t count towards my goal.

Doesn’t include 529s, uninvested cash, emergency funds, UTMAs.

I track taxable, pre-tax, and Roth contributions separately

Dividends automatically roll into Growth.

Company 401k matches should be included in contributions.

FAANG FIRE w/ Extra Guac

If you want to kickstart 2026 with access to some of the financial tools I actually use, that’s what the Extra Guac subscription tier is for.

For $200 annually, Extra Guac members get access to the following tools free (new users):

1 year free of ProjectionLab Premium to model your FIRE plans

1 year free of Lunch Money to add logging into your financial life

1 year free of Mezzi to get an AI driven insights into your portfolio

1 year of Carry Solo 401k for $1 to power your Solo401k

$75,000 managed fee free with Frec to power your direct index

30 minutes of 1:1 FIRE coaching with me to help bring it all together

Offers available for first time customers of the tools, you can upgrade to the Extra Guac tier and to claim your codes which will be delivered within 2 days.

Other Financial Tools I Use from my Partners

Top Free Tool: Empower. If you are looking for a free alternative to track your overall net worth Empower (formerly Personal Capital) is my recommendation.

Top All-In-One Paid Tool: Monarch. If you care about strong categorization of your spending, goal setting, smart automation, good design, and are willing to pay Monarch is an easy option to recommend ($99 normally but available 50% off with promo code MONARCHVIP).

Premium Net Worth Tracking Tool For Complex Scenarios: Kubera. Kubera has quickly become one of my favorite net worth trackers. It helps me break down my entire net worth in all the ways I want. Designed to help high-net-worth individuals track their overall finances.

-Andre

ps, I read every reply to these emails

Good read. Might actually swap my NW goal for contribution goals after reading this