Where to Put $100k in Savings Per Year

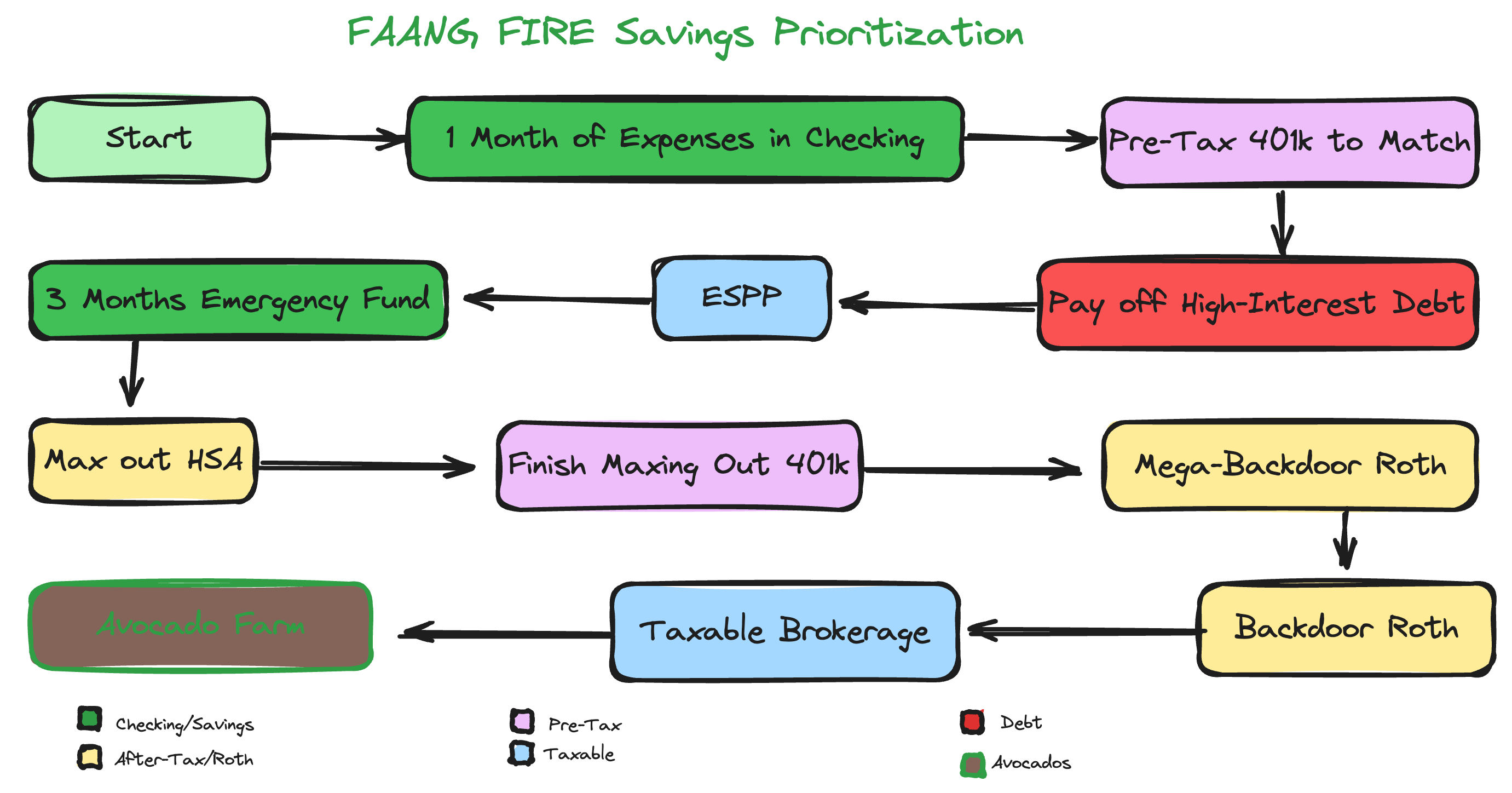

FAANG Savings Prioritization

Let’s run through a few specific scenarios of where I would put an extra $100k in savings per year.

This is $100,000 in annual savings. A sum that is very achievable for mid-level FAANG employees and dual income tech couples. This is a slightly different scenario than if you had a lump sum of $100,000 sitting in your checking account.

Imaginary internal Dialog: … $100k is a crazy amount of money, yes FAANG workers are privileged, yes not all FAANG workers, yes it is hard with 2 Tesla leases, yes…. ok back to the post…

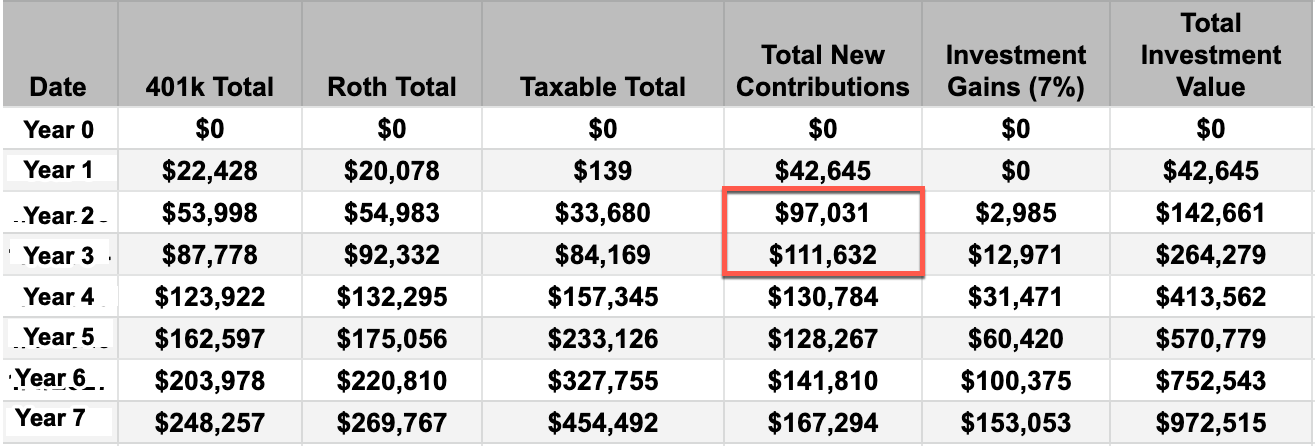

In my New Grad Engineer to FIRE series, I projected that a new grad engineer at Meta could hit the $100k annual savings milestone in around their 3rd year as an E4. This is without assuming any stock appreciation. (deep link to where the chart below appears)

Executive Summary:

I will walk through a number of specific examples across different scenarios of how I would invest $100k over the course of a year.

Different $100k Scenarios Covered:

Married, Single Income, Works at Meta, Has HDHP w/HSA, No Debt, No Kids, 6 month Emergency Fund

Single, Works at Meta, No Debt, No Kids, 1 Month Emergency Fund

Single, Works at Uber, $25k CC Debt, 3-6 Months Emergency Fund

One key theme I want to highlight is that personal finances are deeply personal; prioritization can be impacted by a large number of factors, from your goals, existing debt, timelines, and company benefits. Understanding how to prioritize your finances is more important than any underlying framework.

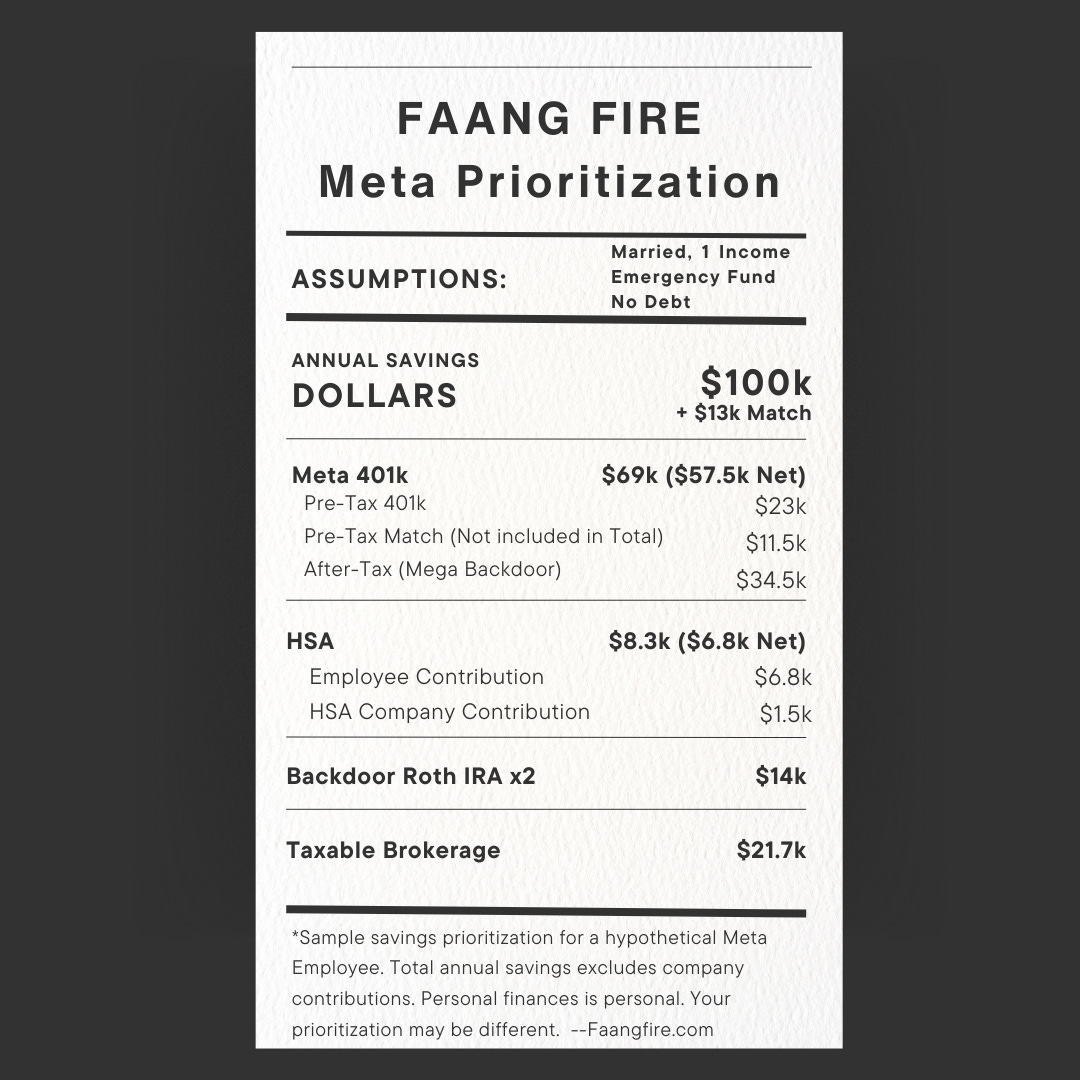

Scenario #1: Married Meta Employee w/ Single Income

Married, 1 Income

Age: early 30s

Has a 6 months emergency fund in a HYSA

No debt

Has HDHP w/ HSA

Excess Savings Available per Year: ~$100k

No kids and no plans for kids

FIRE Timeline: >5 Years

The first thing I note here is that there are 2 people, but only 1 is working. This will limit our 401k contribution options. They have a high deductible health plan with an HSA; this opens up a few other options. A FIRE timeline of more than 5 years makes it easier to focus on retirement accounts without needing to factor in existing savings as much.

The $100k Savings Breakdown:

$57,500 towards the Meta 401k. With Meta’s 401k match of $11,500 it will increase the overall balance of their 401k by the annual IRS limit of $69k. $23k of that will go towards their pre-tax 401k (the limit), and the remaining going towards their After-Tax 401k w/ in plan Roth Conversions. ($42,500 remaining)

$6,800 towards HSA. The HSA annual family maximum contribution is $8,300. Meta contributes $1,500 into your HSA, which counts against your contribution limit. I would fully max out the savings into the HSA. I wouldn’t spend this money on medical expenses, instead paying out of pocket, while saving the receipts in a Google Drive folder. I would then move my HSA funds to Fidelity’s free HSA that allows for the full balance to be invested. An HSA account is funded pre-tax, grows tax free, and if used for medical expenses in the future, isn’t taxed at withdrawal. I have a longer post in the works dedicated to HSAs. ($35,700 remaining)

$14,000 into two Backdoor Roth IRAs. Normally, you need earned income to contribute to an IRA; however, if your spouse is working, you can use their earnings. This is called a Spousal IRA contribution. The process of executing a Backdoor Roth IRA is important to understand prior to doing this. I covered this process in this post dedicated to a step by step Backdoor Roth Walkthrough. ($21,700 remaining)

$21,700 invested into a normal taxable brokerage account. Since there are no mentioned short term spending goals (I consider spending goals of less than 3 years to be short term), I would focus this on the longer term FIRE goals. ($0 remaining)

Savings Nutrition Label:

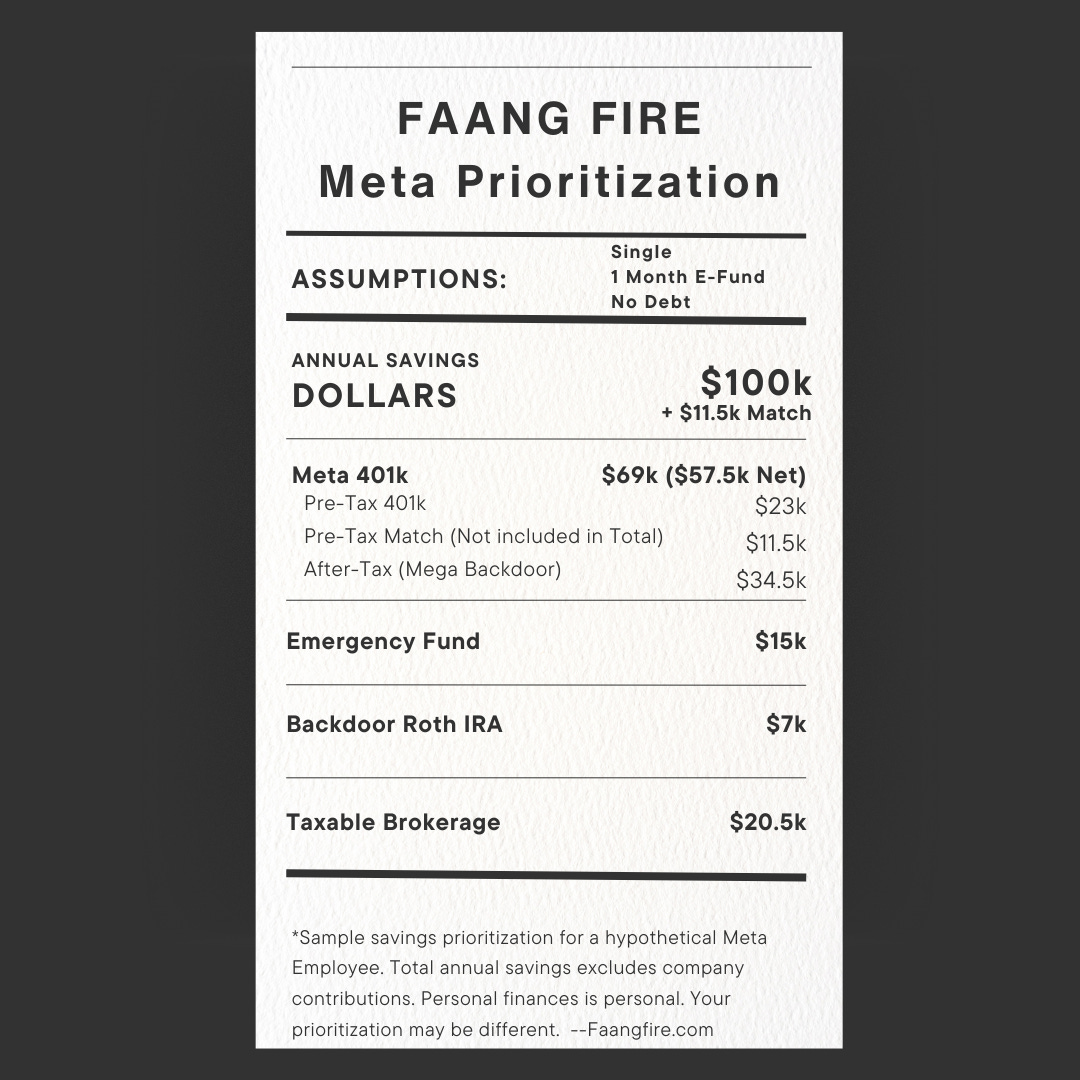

Scenario #2: Single Meta Employee

Single

Age: 27

No Debt

No Kids

1 Month Emergency Fund

FIRE Timeline: >10 Years

$100k Savings Breakdown:

$15,000 towards bringing their emergency fund up to around 3 months. This is a reasonable buffer for a single person. They also have the “benefit” of seeing 3+ rounds of Meta layoffs and knowing the severance historically has been generous in the event of an unexpected layoff. ($85,000 remaining)

$57,500 towards the Meta 401k. With Meta’s 401k match of $11,500, it will increase the overall balance of their 401k by the annual IRS limit of $69k. $23k of that will go towards their pre-tax 401k (the limit), with the remaining going towards their After-Tax 401k w/ in plan Roth Conversions. ($27,500 remaining)

$7,000 towards a Backdoor Roth IRA. The process of executing a Backdoor Roth IRA is important to understand prior to doing this. I covered this process in this post dedicated to a step by step Backdoor Roth Walkthrough. ($20,500 remaining)

$20,500 towards invested into a normal taxable brokerage account. Since there are not any mentioned short term spending goals (I consider spending goals of <3 years to be short term), I would focus this on the longer term FIRE goals. ($0 remaining)

Savings Nutrition Label:

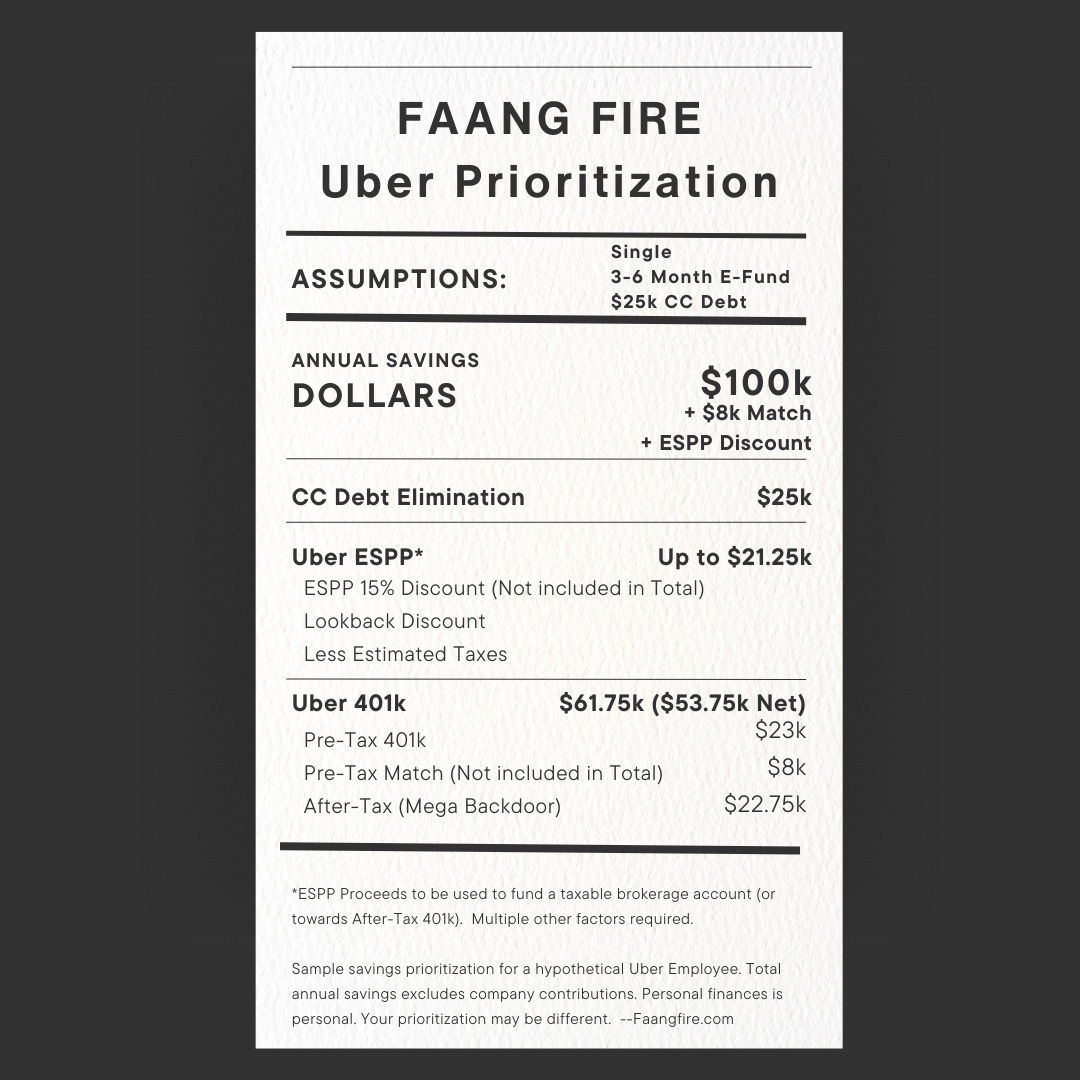

Scenario #3: Single Uber Employee w/Debt

Single

Age: 25

$25k Credit Card Debt at ~24% APR

3-6 Month Emergency Fund

FIRE Timeline: >15 Years

$100k Savings Breakdown:

$25,000 towards eliminating the credit card debt. With the interest so high, there will be few better uses for their savings. I would go so far as to recommend that they reduce their Emergency Fund down to 1-2 months while they focus on eliminating this debt. ($75,000 remaining)

$21,250 towards the Uber ESPP, sold and used to fund a taxable brokerage account. The Uber ESPP allows employees to purchase Uber stock at a 15% discount in addition to a look back window. The $21,250 is the maximum they would be able to contribute (85% of $25,000), which would be reduced further depending on the purchase price. ($53,750 remaining)

$53,750 towards the Uber 401k. With Uber’s match of $8,000 it will increase the overall balance of their 401k by the annual IRS limit of $69k. $23k of that will go towards their pre-tax 401k (the limit), and the remaining going towards their After-Tax 401k w/ in plan Roth Conversions. There are not enough funds to fully max out the after-tax portion of their 401k. ($0 remaining)

The introduction of the debt and ESPP changes the prioritization. There may be further optimization opportunities here with the ESPP proceeds that may allow for the full maxing out of the After-Tax 401k. There are too many ESPP tax factors to fully encompass here. I would still likely prioritize at least $5,000 towards a normal taxable brokerage account just to get that account started. I found it mentally easier to add money into an existing account vs needing to open a new one.

Savings Nutrition Label:

Rough Prioritization

As I walk through these different scenarios, I am mentally going through a prioritization exercise. At the end of the day, this is like any other resource allocation exercise, and prioritization is one of the most important things you can control.

It is also important to realize that many factors that can change this basic sequencing.

For example:

If you are a dual income household 3 months of emergency fund might be fine, but a single income household with kids might be better suited with a 6-12 month emergency fund.

There are some scenarios where you might prioritize an ESPP w/ a good discount and look-back window ahead of your debt, depending on the interest rates and ESPP terms.

If you have short term spending goals, I would place a larger prioritization on building up a more liquid savings balance.

An HSA might be a poor option for your household due to the out of pocket costs of the HDHP making the return on hassle of saving money into an HSA not worth it.

Supplemental Reading:

Personal finance is personal, and financial prioritization is just as personal.

I hope seeing a few examples can help give you confidence in how you are thinking about your own personal prioritization.

Should I turn this into a series? If so, what scenarios would you like to see me walk through?

Podcast: One Year After Facebook

There is a funny tendency in the FIRE community for some men to jump up and say "I am retired" while their wives are still working, even with children at home. I can't recall a single time when I have heard a woman leave work, take on more child related activities, and declare themselves "retired". This is why I consider myself “Semi-Retired”.

I had the chance to talk about this with Sam Dogen on the Financial Samurai podcast. It was a fun conversation, almost exactly one year after our last conversation when I was just laid off from my job at Meta.

Listen on Apple Podcasts, Spotify, or on the web.

-Andre

I’m confused about the 401k bit. I thought max contribution is 23k regardless of Roth/traditional. So if you put 23k in pre-tax, you won’t be able to put anymore in roth?

Can you share the math for why ESPP (15%+ instant discount, mostly taxable with some weirdness if held for multiple years) is prioritized above maxing out mega backdoor roth 401k space, which at high income tax levels is worth more (https://www.bogleheads.org/forum/viewtopic.php?t=171858)?