Direct Indexing Experiment Update

It has been more than 6 months since I invested $100,000 into a Direct Index that tracks the S&P 500. Now that I have run it through its paces, I thought it would be a good idea to share the actual results of the experiment and why I am adding $74,000 more while also migrating from the S&P 500 Index to a US Total Market Index.

If you are new to the concept of Direct Indexing and Tax Loss Harvesting, check out my original post on the topic:

The Results So Far

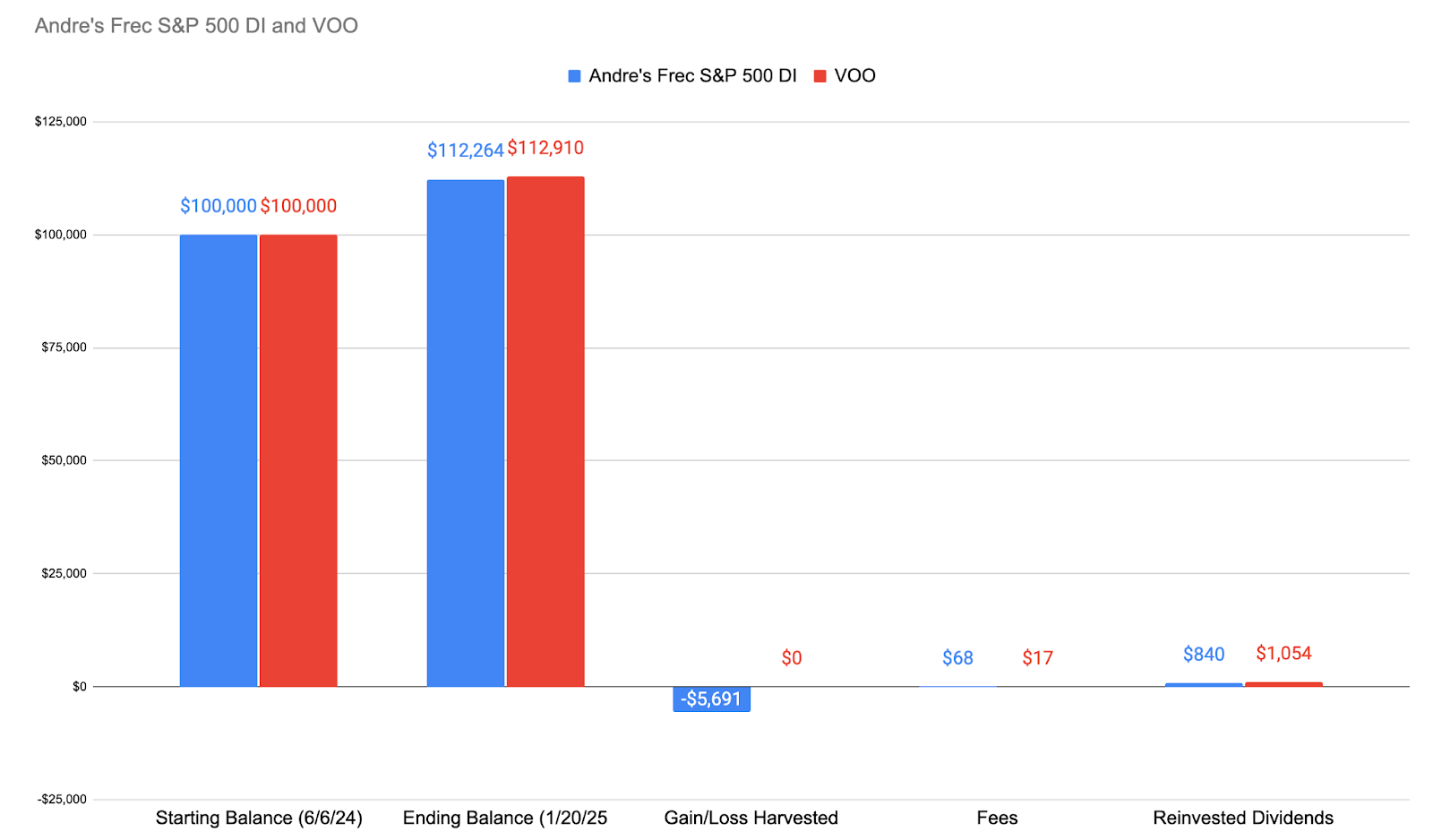

Start Date: June 6th 2024

End Date (for analysis): January 20th, 2025

Beginning Balance: $100,000

End Balance: $112,264

Index Tracking: S&P 500 Excluding Uber (my wife’s employer)

Total Losses Harvested: $5,6911

Total Harvest as Percent Invested: 5.69%

Estimated Tax Savings (per Frec): $2,521.41

Based on 35% federal, 20% LTCG, 9.3% California

Total Fees: $68.22

Cash Dividends & Interest: $840

Portfolio Drift as of 1/2/2025 Factoring in exclusions per Frec: -0.84%

“You are tracking the index with a drift of -0.84%. The drift includes the impact of your index customizations.”

Let’s Dig Into These Results

The key element I have been impressed by was that Frec has managed to harvest $5,691 in losses. This would have been nearly impossible for me to do manually in 2024 due to the market going up and to the right most of the time. If we assume I don’t have any additional gains in 2024, I would be able to use $3,000 of those losses to reduce my taxable income (assume 35% Federal, 9.3% CA). So that’s a real $1,329 I am saved in taxes for 2024 in addition to still having $2,232 in losses to carry forward into future years or offset gains elsewhere in my portfolio along with the $459 already harvested in January for 2025. If I had other realized short term gains to offset, then perhaps the full quoted tax savings of $2,232 would be realized. But, of course the personal tax savings are going to be far more nuanced and up to your individual circumstances.

Let’s Dig In A Little Deeper

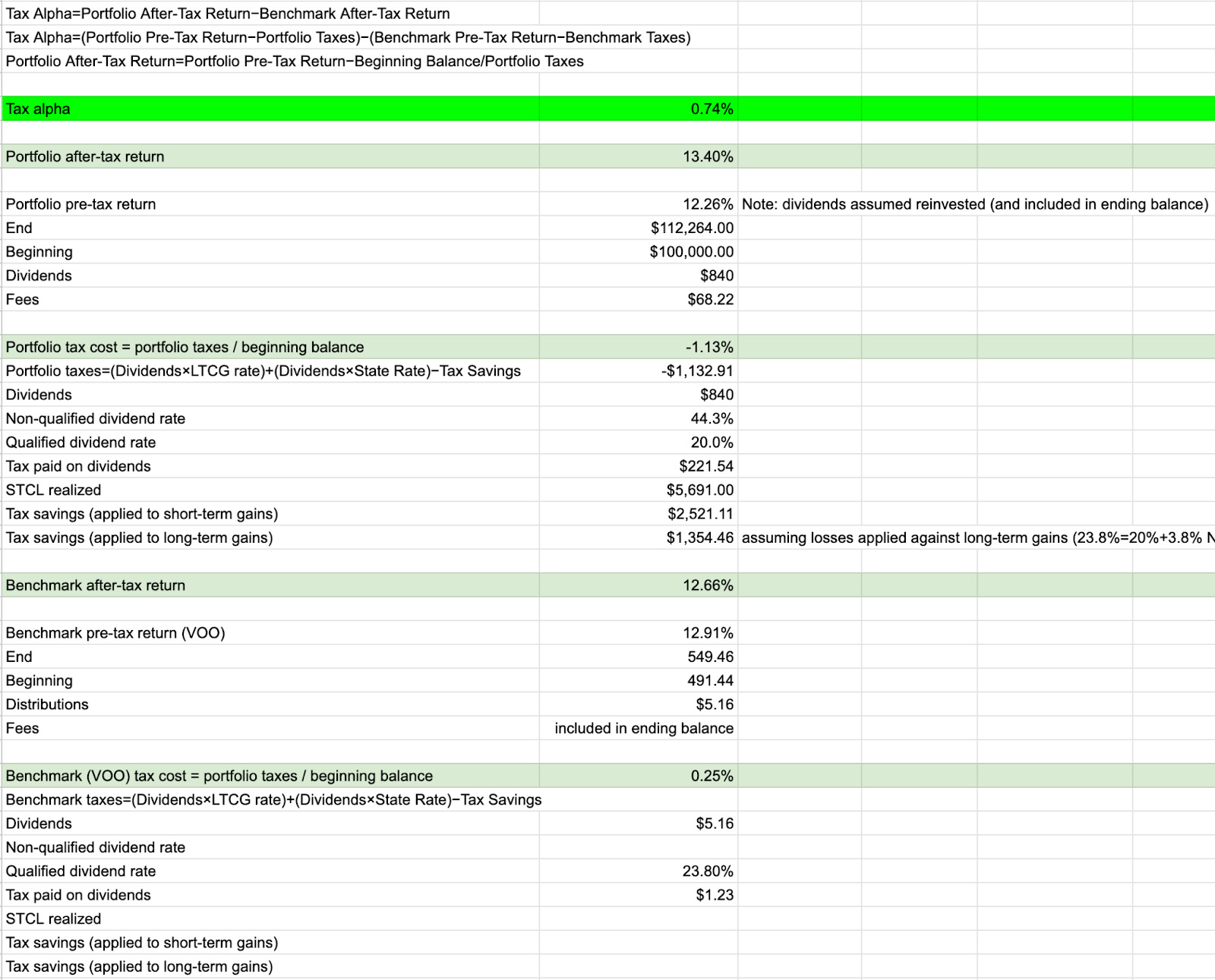

I have been critical of tax loss harvesting in the past. Particularly when high fee brokers/advisors position the benefits as tax loss harvesting as a magic pill that pays for the fee. I broke down the mechanics of how tax loss harvesting benefits can easily be overstated if you ignore the long term impact of now owning stock with a lower cost basis. This means that my new cost basis of my Frec portfolio is ~$95k (after subtracting the harvested losses and adding back reinvested dividends).

This is where the concept of “Tax Alpha” comes in. The “Tax Alpha” is supposed to help us better compare the after tax benefits of utilizing Direct Indexing vs an alternative strategy, in this case, buying an index fund that tracks the S&P 500.

I had my good friend Brent Sullivan, writer of Tax Alpha Insider, help me out with the rough calculations.

Personal Tax Alpha is Personal! In my current situation I am immediately realizing (using) the losses generated from my Frec portfolio to help me reduce some of my partners concentrated Uber holdings. So all of the harvested losses will offset long term capital gains.

With these assumptions we came up with a Personal Tax Alpha of ~0.74%.

There are a tremendous number of caveats to these numbers. It has only been 7 months. It factors in the current portfolio drift of -.84%. It compares against VOO with dividends reinvested. A mix of qualified and non-qualified dividends. It doesn’t factor in the time value. Again, it has only been 7 months and this is an estimate for a single portfolio in my specific tax situation. The Tax Alpha would jump up to 1.75% if you were offsetting short term gains with the generated losses.

This Post is Sponsored by Frec

As we're kicking off the new year, now's a great time to start thinking about your taxes. Frec direct indexing can help you earn more by unlocking tax savings, no matter the market. You can start direct indexing for as little as 0.10%. Check them out at frec.com

FAANG FIRE readers are eligible for a $250 Sign Up Bonus when you join Frec and invest at least $20,000 into one of their Direct Indexing portfolios.

Unexpected Benefits of Direct Indexing

I originally invested $100,000 because the fees that Frec offers finally pushed me into being convinced that a small amount of additional complexity is worth it. So the “tax alpha” that I am seeing above is mostly a confirmation, I am happily seeing what I expected. There are a few other benefits though that I originally didn’t anticipate that come with direct indexing over simply buying index funds.

I Gained a Deeper Understanding of the Index

Since I now own >500 individual companies, I have a much greater feel for the overall index. I can easily look at the composition of a fund, somehow actually having the shares makes it much more real. It also makes it even more apparent how head heavy the markets are right now… and why has Broadcom managed to avoid the limelight as they pull into the largest 10 companies in the US!

Dividends Are Fun?

I am in the total return vs dividend camp. That is to say that I invest with a focus on overall growth, not dividends. Alas, some dividends are inevitable though. The S&P 500 Direct Index AND an index fund tracking the S&P 500 will return the equivalent dividends over time. VOO distributes the dividends 4 times over the year, while a direct index pays these dividends in small chunks in real time! Randomly entertaining seeing the deposits nearly every day…

Unexpected Downsides To Direct Indexing

I also went into Direct Indexing understanding some of the downsides. I was giving up the pure simplicity of an index fund like VOO in exchange for holding 500 individual positions! There were a few downsides I didn’t fully anticipate though.

All My Tools & Dashboards Are Flexed

Frec has done a good job investing in making the integrations work with 3rd party budgeting tools. The budgeting tools however are just not prepared for dealing with 100’s of trading transactions per day. I gave up on my personal spreadsheets that track all the individual positions I hold (there is now a “catch all” Frec ticker that I manually update).

This is what my Monarch Money transactions look like every day now:

New Nerves on Market Drops?

I really like how the direct index automatically executes dozens or even hundreds of trades per day in companies that make up small portions of the overall index. However, most losses tend to be captured on days when the market experiences a broad decline. I do feel a bit nervous when some of the largest companies are sold because at those times you are really relying on Frec’s ability to swap those shares for other highly correlated assets.

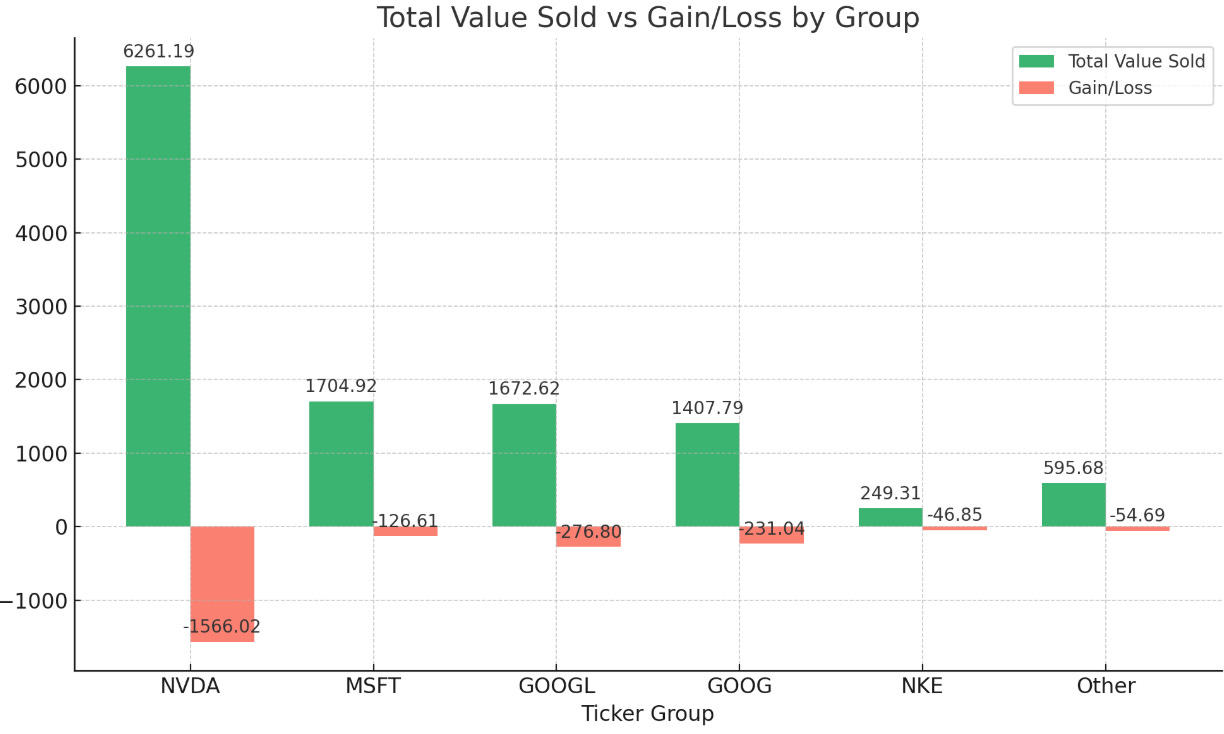

For example, on September 6th Frec harvested more than $2,300 in losses in just one day.

That single day accounted for 40% of all my harvested losses so far. Among the companies sold were Nvidia, Google, and Microsoft, which meant my portfolio went 30 days without three of the biggest names in the index. That is exactly how the process is supposed to work, though it can still feel unsettling, especially if you worry that Nvidia will bounce back quickly and create a performance gap. I imagine these large swings are where most of the “drift” comes from.

My Future Plans

As mentioned in the first paragraph, I have added $74,000 more into my Frec Direct Indexing portfolio. My normal investments outside of my Direct Index have focused on the total US Market. When I first started with Frec the primary option available at the time was the S&P 500 index. They have since drastically increased the number of indexes available, including now adding one for the Overall US Market that tracks the same index that VTI tracks.

I didn’t want to transfer my S&P 500 Direct Index straight into the Total US Market index though. If I did that, then it would end up using up all the losses it had previously harvested in addition to capturing unnecessary gains as it went through and rebalanced the portfolio from the 500 companies to the more than 3,600+ companies that make up the new index.

Instead, I emailed Frec and asked them “I want to transition my current portfolio from the S&P 500 Direct Index into the Total US Market Direct Index. How much in new funds would I need to add to allow you to properly rebalance without needing to incur unnecessary gains or harvest unnecessary losses?” The friendly ops teams at Frec ran the calculations and let me know that I would need ~$65k. I wanted to provide a buffer so I bumped it up to the $74k in new funds.

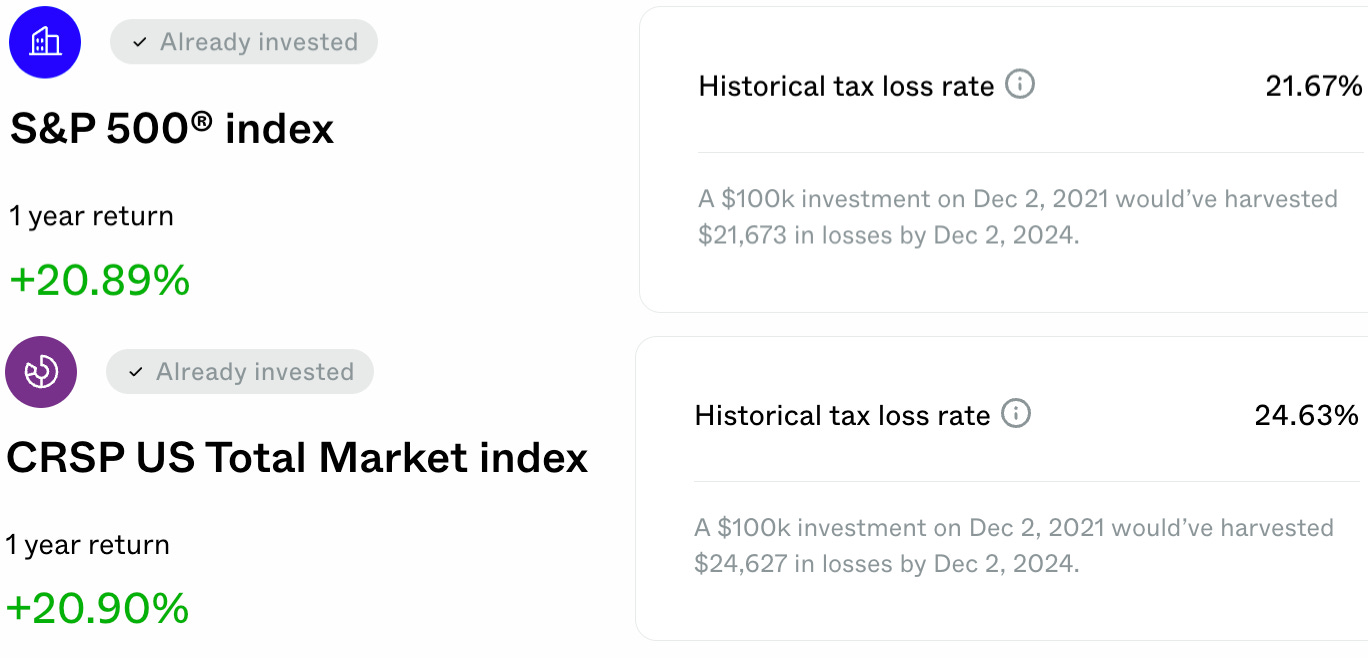

This will not only help me match my personal asset allocation goals better, but the total US market’s 3,600+ should provide more opportunities for Direct Indexing to work its magic with that many more tax loss harvesting opportunities. Frec’s historical estimates put the tax loss rate over 3 years as 24.63% for the total market index vs 21.67% for the S&P 500. The tax loss rate per Frec: “It is based on a historical simulation of a one-time $100,000 deposit into the CRSP US Large Cap from Dec 2, 2021 to Dec 2, 2024, harvesting tax losses on a weekly basis in a three-year time frame. The results are hypothetical, do not reflect actual investment results, and are not a guarantee of future results. The Frec AUM fee was included in the simulation.”

This is Not a Strategy Shift!

When I shared that I was making this change on LinkedIn multiple people were curious about why I was shifting from the higher performing S&P 500 to the broader US Index. It is definitely true that over the past few decades the S&P 500 has out performed the broader index, in addition to greatly eclipsing the entire international stock market. Unfortunately, I can’t invest in the past nor do I have the ability to see the future. My overall goals are to match the overall broader market based on my target asset allocation of 56% US, 27% International, 15% bonds which is likely more conservative than the average almost 40 year old and potentially more internationally heavy. Just to reiterate though, the transition from S&P 500 to CRSP US Total Market Index in my direct index is simply a reflection of my existing strategy and Frec adding in more indices which better matches my current broader strategy.

Closing Thoughts

One of my favorite genres of personal finance is when companies like Frec are able to democratize access to features that were previously exclusive to high net worth households or gated behind high fees. I’ve personally allocated a portion of my taxable portfolio into direct indexing, and I feel like it is proving it’s worth. The strategy would be even more valuable to me if I was in my peak accumulation years or if I was expecting an upcoming capital gain that I was needing to offset. I am also anticipating it will get even more opportunities to harvest losses as we head into what seems sure to be a bit more volatile of a year.

Disclosure: I am a Frec client and Frec paid a one-time fee for this newsletter. I also receive $250 for each referral that uses my link and earns $250.

Investing involves risk, including the risk of loss.

$5,691.67 is the total losses harvested from 6/6/2024-1/20/2025. However, $5,232.34 was harvested for the 2024 tax year and $459.33 was harvested for the 2025 tax year.

I have the same question as Javier. How did Frec perform during the turbulent times of the last few days? Did it panic or remain composed and seized the opportunity?

Great article. Andre, Regarding some of your concerns, I wonder how Frec is doing now (April 2025) when the stock market is down in general. Are they selling most of the biggest company positions to harvest losses and finding new ones to replace? Super curious