Front Loading Your 401k: A 15-Year Backtest

“Front loading” 401k contributions means pushing as much of your annual contribution as possible into the earliest months of the year.

Based on a backtest of the past 15 years of S&P 500 returns, maxing out your 401k within the first four months of the year would have resulted in a final balance 3.2% higher than an equal monthly contribution strategy.

In this analysis, I modeled 401k contribution strategies that front load an entire year’s contributions over 1 to 11 months and compared them with an equal monthly contribution strategy.

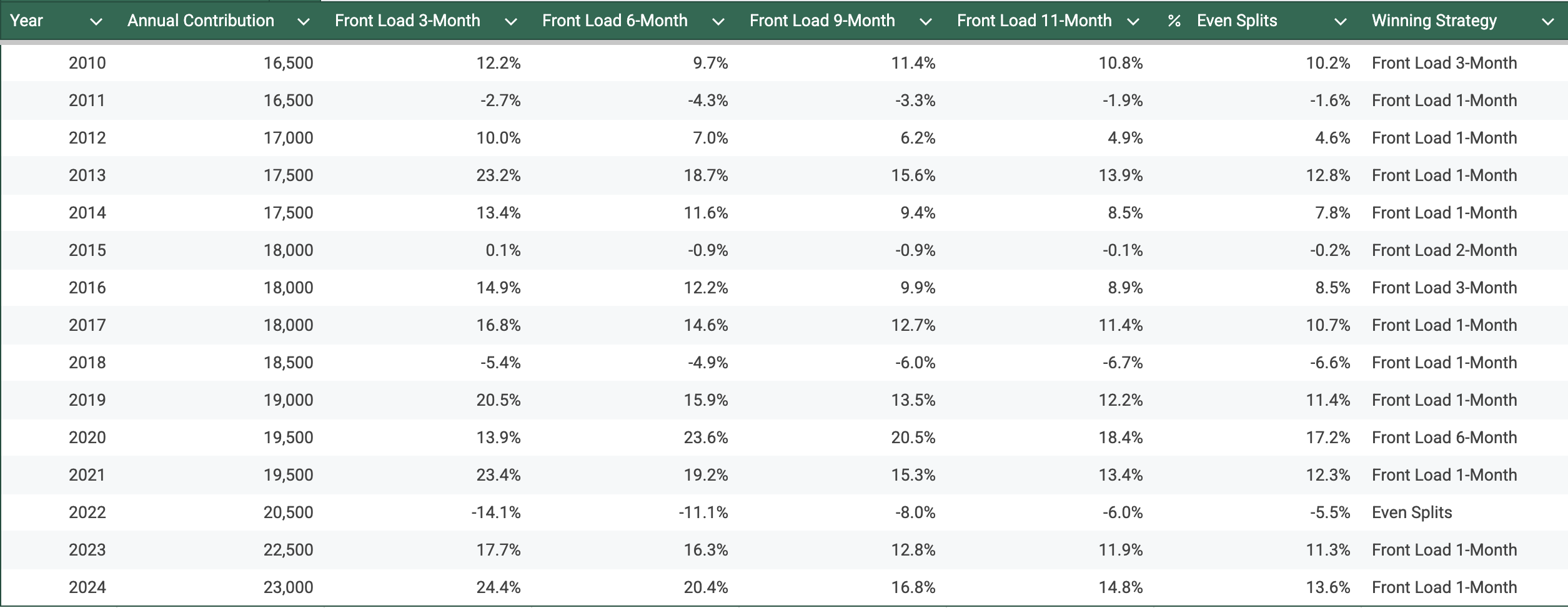

Here are the per-year results:

Front loading within the first four months of the year outperformed equal monthly contributions in 13 of the last 15 years.

Over the full 15-year period, this translated into an additional $23,852 compared to splitting contributions evenly throughout the year.

When previously discussing 401(k) contribution strategies, I leaned on academic literature that consistently found lump sum investing outperforming dollar cost averaging, which helped justify why I front-loaded my own 401(k) while working at Meta.

I still wanted to understand the real world difference between aggressive front loading, which can require extreme budgeting early in the year, and simply spreading out contributions evenly over the year.

In this analysis, I modeled a range of 401k contribution strategies that front load an entire year’s contributions over 1 through 11 months and compared each of them against an equal monthly contribution strategy.

The chart below shows a single comparison: front loading contributions over the first four months of the year versus spreading contributions evenly across all twelve months. This allows us to compare how the two strategies performed in each individual year.

Each row represents a calendar year, with the dots showing the annual return achieved under each contribution strategy.

Note: This analysis is based on a 100% S&P 500 portfolio using total returns calculated from Shiller’s published historical data. Data was from 2010 to 2024. Based on prior Vanguard research, default target date funds would be expected to show a similar pattern, simply reduced in magnitude.

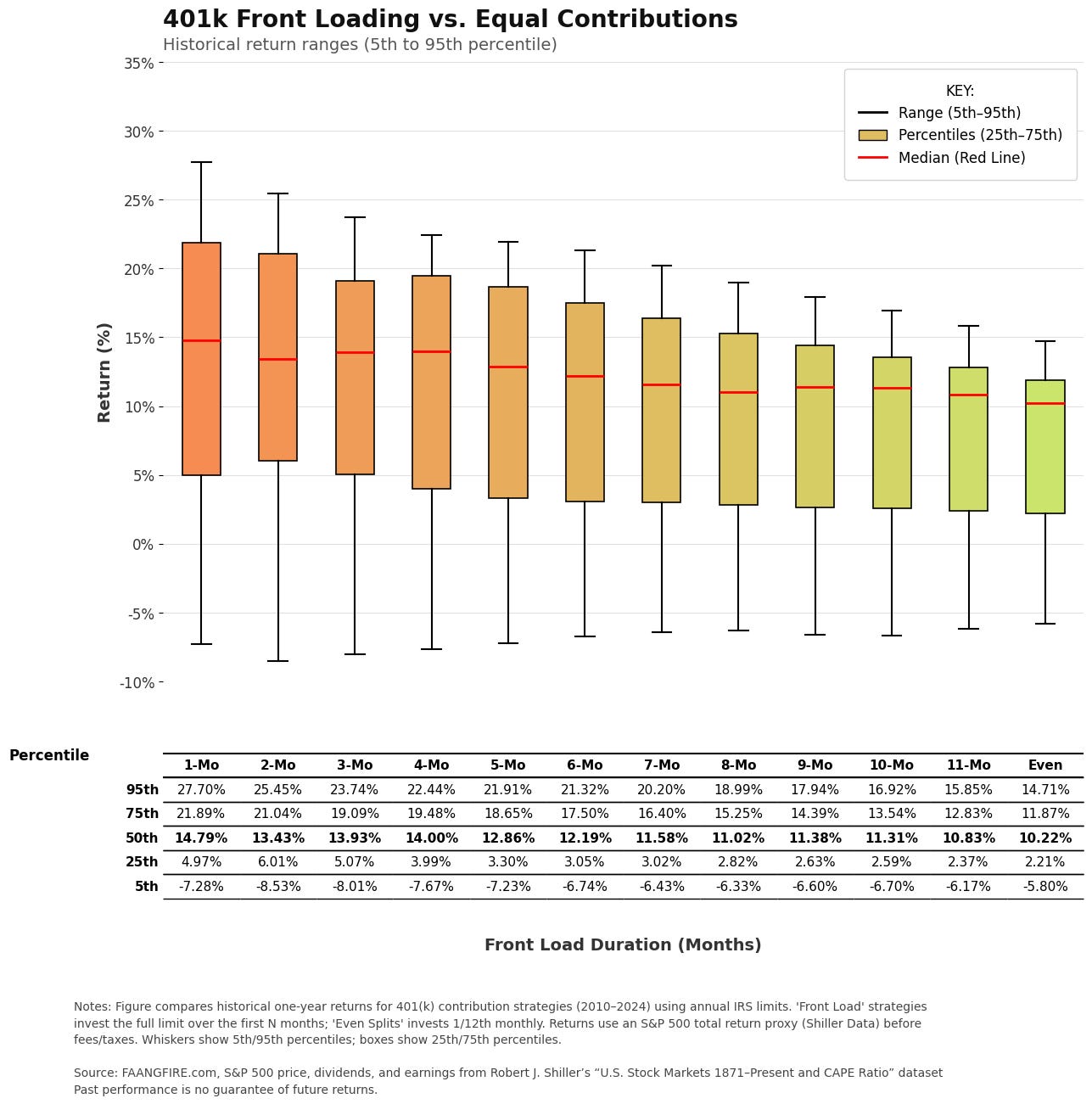

The results of this analysis are consistent with prior academic literature on lump sum investing, which finds higher median returns from earlier investment timing, alongside lower volatility for evenly split contributions.

Distribution of Returns Across Strategies

The chart below shows the distribution of annual returns across the twelve contribution strategies. The more aggressively you front load, the higher the median return tends to be, but with a much wider range of outcomes. Evenly split contributions cluster more tightly, which reduces volatility, at the cost of lower returns.

Overall the results seemed consistently to say that the sooner you’re able to contribute, the better. Every month you pulled contributions forward added a little more return.

Perhaps it is not as surprising when the past 15 years looked like this:

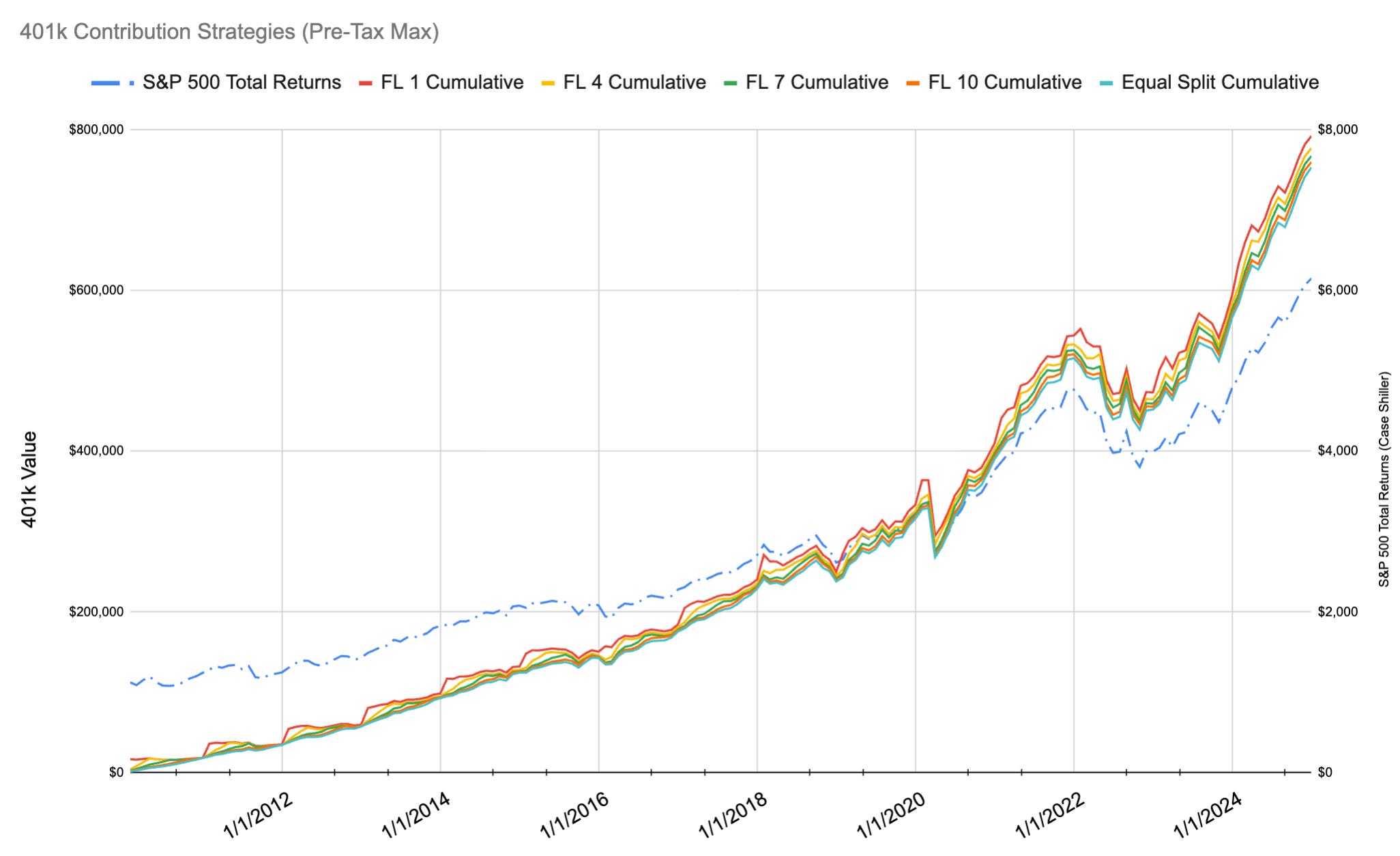

Now let’s take a look at what the dollar impact would be for someone who consistently stuck to one of these strategies starting in January 2010 through the end of 2024.

The red line represents front-loading the entire year’s pre-tax 401k contributions up to the annual limit, and it finished as the leading strategy over the full period. The dashed blue line, representing the underlying S&P 500 total returns, is graphed on the right axis to help contextualize the market conditions over the period.

Over the full 15-year period, front-loading contributions within the first four months resulted in a 3.2% higher final portfolio value compared to an equal monthly contribution strategy.

In dollar terms, that meant $23,852 more in the account for someone who front-loaded their 401k contributions compared to someone who split contributions evenly throughout the year.

For those curious how this scales at higher contribution levels, using full limits including match and mega backdoor contributions, the four-month front-loading strategy ended $76,484 ahead of equal monthly contributions after 15 years, based on $903k in total contributions.

Should You Actually Do This?

Now let’s dig into when this strategy makes sense in practice, and when it doesn’t, in the next section.

Should You Front Load Your 401k in 2026?

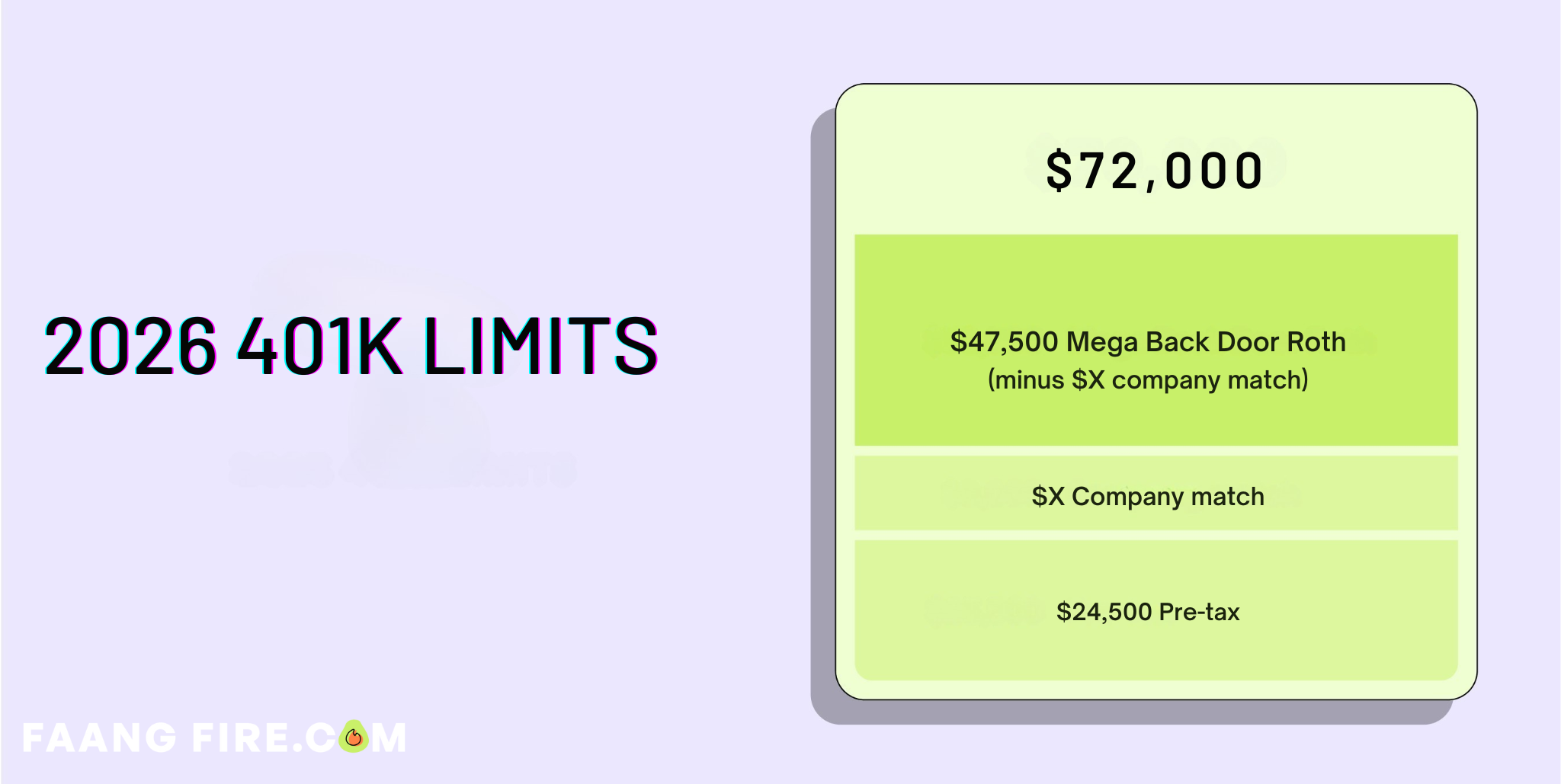

In 2026 the full 401k limit for those under 50 with access to a plan with a Mega Backdoor Roth IRA is $72,000.

Should You Front Load Your 401k?

The real answer has more nuance. There’s a subtle fallacy in this analysis that’s easy to miss, especially when looking at the more aggressive front loading options.

No, it isn’t an income issue. Many in FAANG make more than enough income to pull off front loading within the first four months. I personally did it nearly every year while at Meta. Six or more pay periods plus a healthy annual bonus landing in Q1 made it completely doable.

My primary issue with this analysis is that you still need to fund your life while nearly 100% of your paycheck is going into your 401k. That usually means either building a cash buffer in Q4 of the prior year or planning to live off upcoming RSU vests.

In the first case, this data actually reinforces that you would have been better off investing those funds in your taxable brokerage as they became available. In the second case, assuming your spending isn’t changing, if you simply invested your RSU proceeds as they became available, the gains from front loading would be greatly diminished.

Plan and Personal Nuance Can Change the Answer

It is also important to understand the specifics of your individual 401(k) and to factor in your plans for the new year.

If your employer matches on a per-paycheck basis, front loading could result in missing out on your 401k match (aka free money). The lost match will typically dominate any expected benefit from investing earlier in the market.

If you anticipate switching employers, the strategy changes. You may be able to double-dip on Mega Backdoor Roth contributions, while also leaving enough room in your employee contributions to maximize the match from both employers.

Optimizing 401ks When You Change Jobs Mid-Year

Are you switching FAANG jobs this year? Already switched jobs? Or do you have side hustle income alongside your W2?

Example Scenario: You’re a current Meta employee planning to move to Google after your 2026 bonus lands. Here’s what I would focus on:

While at Meta:

Contributing to your pre-tax 401k up to $12,250 which will unlock the full Meta match of $12,250. Then stop your pre-tax contributions!

Beyond reaching the full match you want to contribute to the Mega backdoor as much as the plan allows which I believe is $35,250.

While at Google:

Thankfully you will have $12,250 of employee contributions available. This will allow you to get $6,125 of Google’s employee match (50%).

You can also contribute as much as possible to Google’s Mega Backdoor. If their limits match Meta’s, that would allow at least $35,250.

This is a clear case where front loading would result in being able to contribute less into your 401k overall.

What Will Be My Personal Approach in 2026?

I’ll be approaching 2026 with two very different 401k setups.

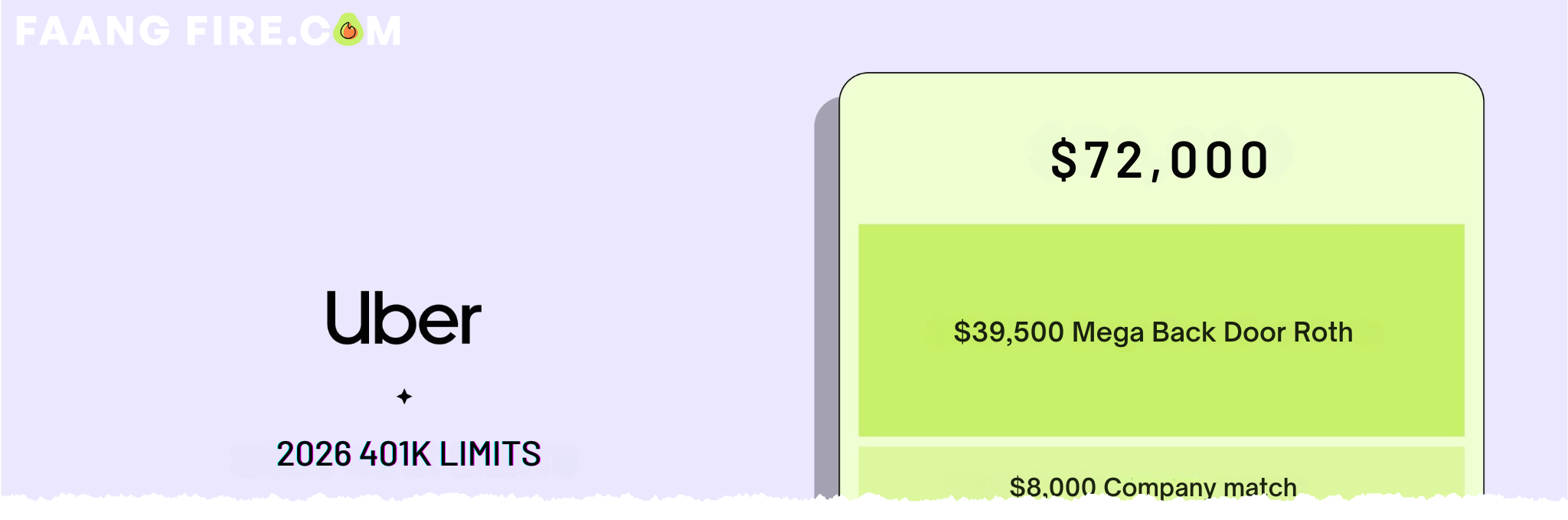

On my end, I’ll be able to contribute $72,000 into a Solo 401k using Carry, which I have access to via the Extra Guac subscription tier. My partner, on the other hand, will be contributing through Uber’s 401k, which comes with an $8,000 company match and very specific matching mechanics.

Let’s start with my partner’s Uber 401k. The overall 401k contribution limit in 2026 is $72,000 and Uber provides an $8,000 company match. Match contributions are applied per paycheck, if there is a contribution, otherwise the match will be trued up in the following year for the missed match, if you left room for it.

To be continued, I’ll share all my plans in a future newsletter!

Can you believe it is nearly 2026 already! How are you setting up your 401k contributions going into 2026?

If you front-load and planning to change job early in the year, you will not be able to take advantage of new employer match.

Andre, when front loading you get your match earlier which potentially gives you a bit more "leverage" for the market gains (or losses). Does that make front loading even more attractive?