My Health Wasn't FIRE-Ready

I started going fishing every few days after I was laid off 2 years ago. It was a great way to get outside and clear my head. It was one of the things I built my day around. Take my daughter to school, drive to the day's fishing spot, pick up my daughter from school.

Then my shoulder started hurting. My body wasn't ready to go from fishing once every few months to nearly every day. My fishing equipment was fine for the occasional trip, but way too heavy for everyday use. An old high school tennis injury likely exacerbated the issue.

After 2 years ignoring it, resting, doing physical therapy, buying random shoulder relievers off the internet, I finally went to the doctor.

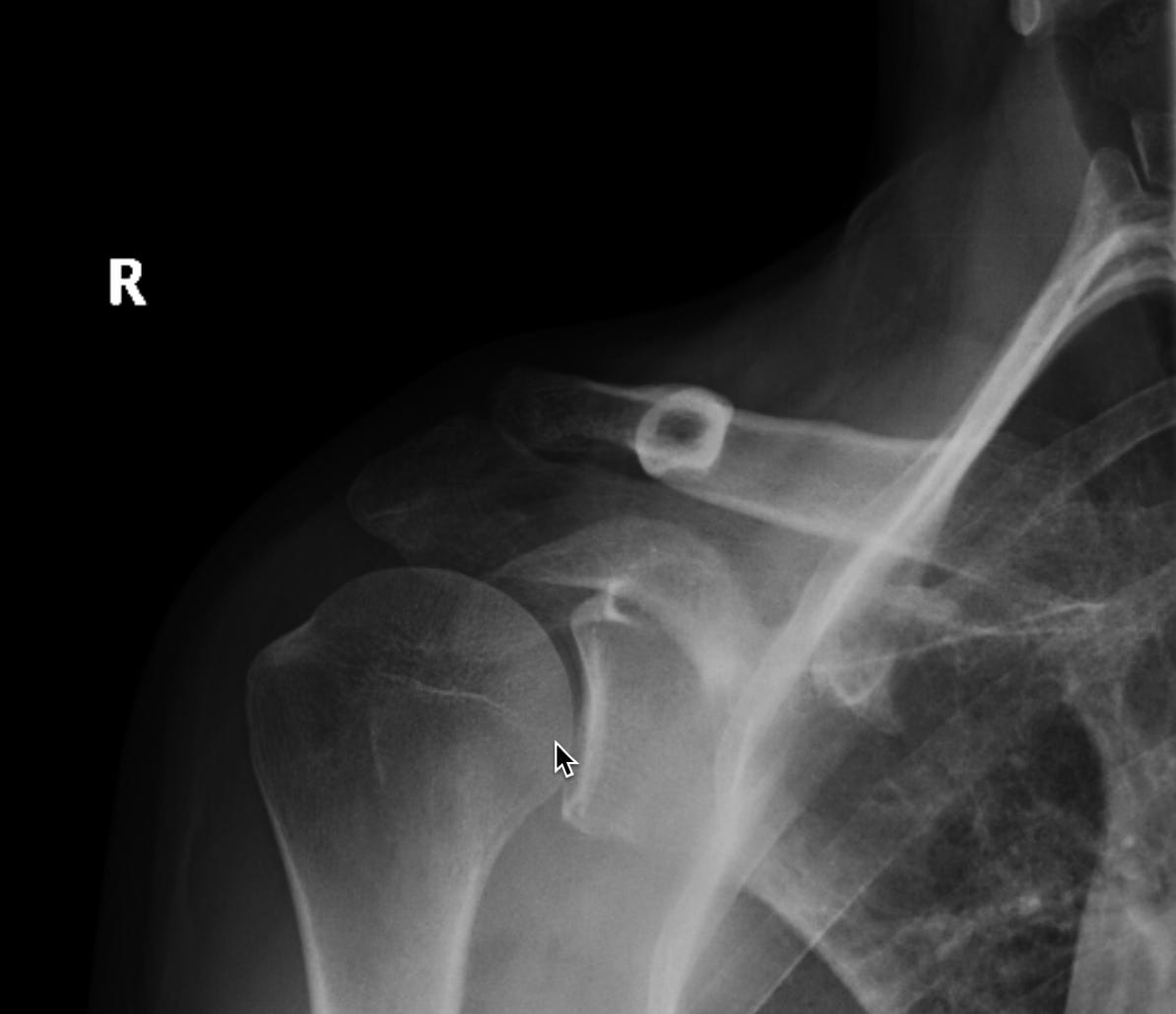

The X-Ray showed "moderate degenerative change of the acromioclavicular and glenohumeral joints". Essentially arthritis or wear and tear on two different joints. Not something someone in their late 30’s should have. The Dr. said the arthritis was likely a symptom of a soft tissue issue that the x-ray can’t see.

Next step is an MRI to try and get a better idea of what the underlying issue is.

Why am I telling you all of this? Does this have anything to do with FIRE?

I want you to learn from my mistakes.

Don’t wait until you are retired (early or otherwise) to start doing the activities you enjoy doing. Invest in taking care of your body in ways that will allow you to do the things you enjoy.

Pay Off Your Debt Now

One of the first things I think everyone should do before even considering FIRE is to tackle their high interest debt. It is one of the first steps in the FAANG FIRE prioritization waterfall.

While I was diligent in keeping my high interest financial debt low throughout my career, there was another type of debt I neglected.

My Health Debt.

Just like financial debt, health debt can also bury you in interest penalties, high fees, and an ever-growing mountain that feels impossible to get out from under.

I know it’s easy to say “I’ll worry about my health after I retire”, because that is what I told myself.

Now that I finally have the time to invest in my health, I need to take a step back first. I need to start paying off that debt.

I am far far far from a health expert. So let me swing back and make the financial case here.

You want to get your health in order while you are working. That big tech health insurance is often some Rolls Royce level of premium insurance. I am lucky right now because I am still on my wife’s big-tech company insurance plan.

That X-Ray I just received? I paid $25 co-pay on my EPO plan to see the Dr. and didn’t get hit with any extra costs for the X-ray since everything was in-network (something I have found very easy to do within San Francisco).

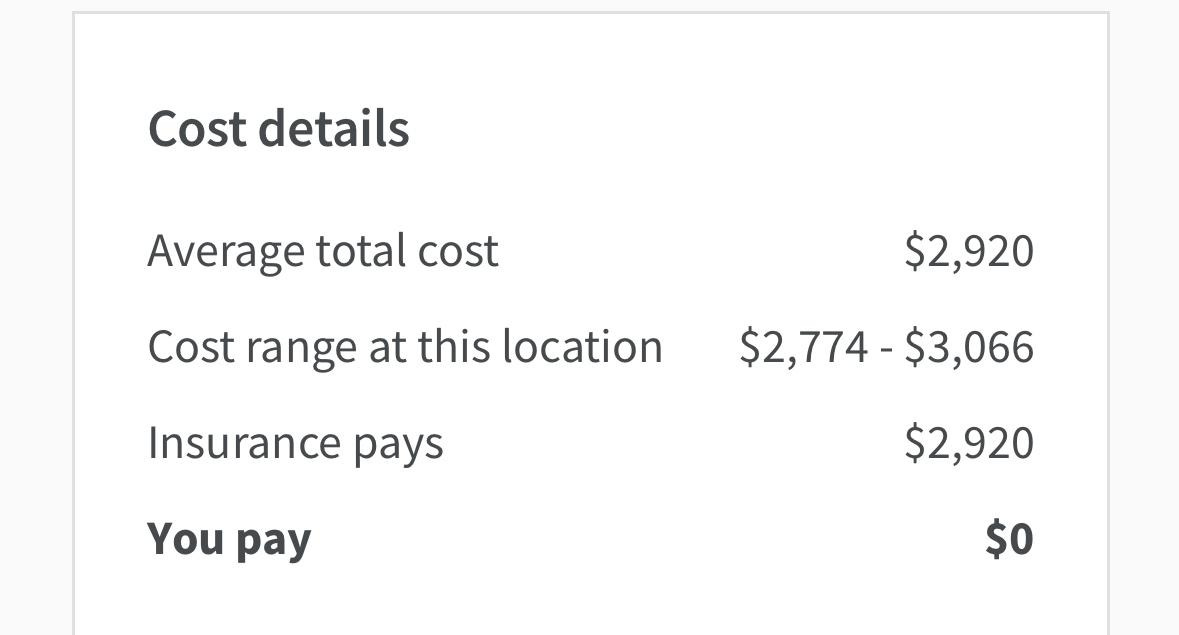

That upcoming MRI? A procedure that averages nearly $3,000? I’ll probably another co-pay at most. Likely $0.

While you are working is the optimal time to begin taking steps to address those ailments.

It is much easier to throw money at the problem while you are working too. I often tell those who are close to FIRE, or feeling particularly burnt out, whether there are opportunities to use that big-tech salary to make their lives easier. Because the reality is that if you can spend more on things that improve your life just enough to stay in your job for one more month, maybe one more vest, then that would have a very high ROI.

Throwing money on things that will reduce the friction to getting healthy is likely even higher ROI! Both financially but also in terms of the harder to measure metrics around lifetime enjoyment (or utility for you econ nerds).

Don’t Wait to Do Things You Enjoy

This is a cliche phrase within the FIRE community at this point but “build the life you want, then save for it”. It is very easy to flip that around, something that I am often guilty of. It is just easier to save than live life. That is sad to type, but I know that about me. Knowing that is critical to addressing it.

I waited until I was semi-FIRE before I started going fishing regularly. If I would have made time for this sooner, I would have likely caught the shoulder issue earlier. Whether I could have done anything to prevent it is unclear, but with most of these health things your body is just able to recover more quickly the younger you are.

It could have also helped prime me to identify other activities that were better suited sooner.

You honestly have to be really intentional about it. I personally found this to be particularly true after I had my daughter. With both my wife and I working, it just felt impossible to spend time doing things I enjoyed. I envy those other parents who seem to continue living their best lives after having kids, but I personally struggled. It really felt impossible.

My limited, n=1 experience is that it doesn’t get easier; it just gets harder in new and unanticipated ways.

Sorry, I got sidetracked a bit there. Let’s bring it home for a minute.

1. Run a personal understand analysis on the state of your health

That nagging pain in your knee? Now is the time to put that premium big-tech health insurance to work. Schedule that physical, get your blood work done, see that specialist, get the MRI. Let your company’s benefits plan pay off most of the “interest” on that health debt. You’ll likely still have to put in the hard work to pay down the “principal”!

2. Reduce Friction with High-ROI Purchases

While you’re still working, it is much easier to throw money at a problem. So, what is one purchase that could reduce the friction to getting healthier? Think about it. Maybe it’s a better mattress to improve sleep, a meal delivery service to free up time for evening walks, or in my case, lighter fishing equipment that doesn't aggravate an old injury. We need to calculate the return on investment here not just in dollars, but in the harder-to-measure metrics around lifetime enjoyment. The reality is, if you can spend money on something that improves your life just enough to help you stay in your job for one more month, or even one more vest, that purchase offers an incredibly high ROI. Throwing money at things that will reduce the friction to getting healthy likely provides an even higher return.

3. Force Yourself to Make Time For Enjoyable Activities

I get it. Life is busy. It is easy to keep putting off “leisure”. At the same time you feel like you are stuck in this “boring middle”. Just remember. That “boring middle” is you living your life. You have the power to do things. You have the money to do things. So, please don’t wait to go enjoy life. The mental trick that helped me here is to think about activities in your life as earning “experience points”. Each time you think back on those experiences, you then earn “experience dividends”. Certain experiences are worth more experience points at different times in your life (i.e., skiing in your 20s is more enjoyable than skiing in your 50’s). Your new goal in life is now to maximize your lifetime experience points. (hat tip “Die With Zero”)

Refocusing 2025 on Health

I am done waiting. I am in the middle of “Step 1: Run a personal understand analysis”.

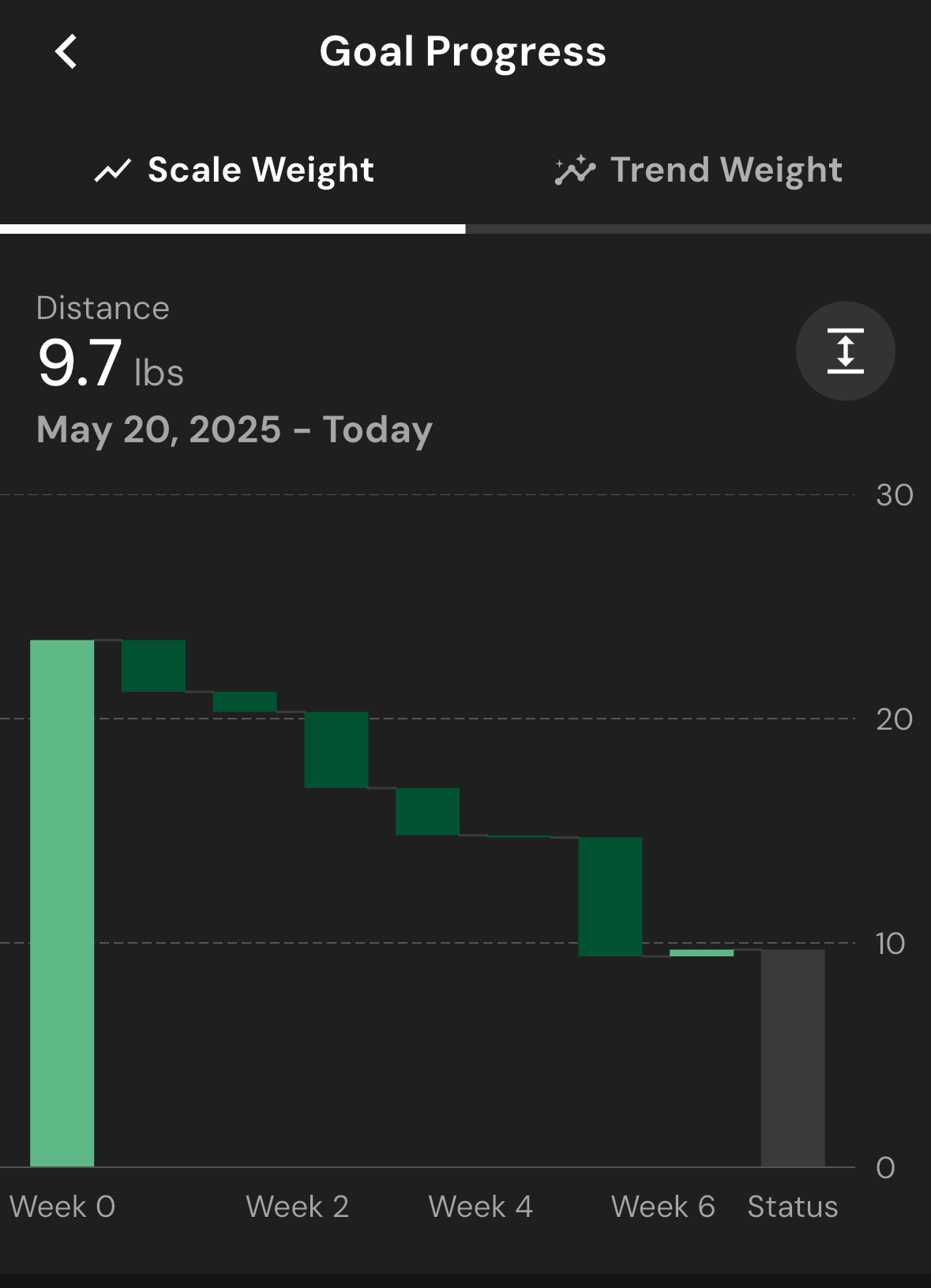

In May I added more logging into my life in the form of calorie tracking. My goal is to lose 25 lbs by the end of September via a simple reduction in calories. Currently targeting 1,600 calories per day, targeting ~1.4lbs weight loss per week. I have around 10 lbs to go.

Next week I’ll be getting my shoulder MRI which will inform more specific plans to address that injury.

Regardless of those plans, I will be layering in some very light cardio. The only goal here is to get my body acclimated to any level of activity without risk of injury. Light zone 2, 3 times per week, should also assist with my weight loss goals.

That is where I am at right now. I know I will want to introduce strength and mobility into the mix. I don’t yet know what form that will take.

While I am impatient, I need to remember that this is a lifelong marathon. The goal is the be able to have a body that allows me to spend time doing things I enjoy. The life outside the spreadsheets.

I am not going full Bryan Johnson; but I am wanting to start exploring all those options between doing nothing and adopting a blood boy.

There we go. I wrote all that down and pressed publish. That means I now have you all to hold me accountable. I also want your help. For those who have been there, what worked? If you have other ideas for how to help, reach out!

You are doing the right thing addressing this now. I can tell you waiting will only make things worse. I got serious about improving my health during COVID and now walk about 8 miles a day and lift weights twice a week. My personal trainer is pricy but it is an investment in my health span and is money well spent. I am much stronger, healthier, and mentally stronger. I still have the aches and pains of being 56 but I can’t imagine where I would be if I had not invested in my health. Good luck!

What health care are you getting? Silver or gold? How much do you pay monthly? Thanks for sharing