Tax Impact Per Share:Before You Sell RSUs, Know This Number

Understanding and calculating the tax impact per share.

I am not sure if I’ve mentioned this yet, but RSUs are taxed as income the moment they vest whether you sell or hold.

(This post is specific to US Public company RSUs).

RSUs are taxed as income the moment they vest, whether you sell or hold. This means that at the moment of vest, if you sell your newly vested RSUs, you will only pay additional taxes if the stock price is now higher than the vest price, and in most cases it will be minimal in the days after vest.

But how are shares from past RSUs taxed?

This Post is Sponsored by Frec

Want a way to express your market view while offsetting more capital gains?

Frec is launching a new long short direct indexing strategy, starting with a 140/40 structure built on the Russell 1000. This next level of direct indexing allows investors to express a point of view on the market (e.g. increased exposure to growth stocks) while also increasing potential tax loss harvesting results.

This strategy can be particularly helpful for FAANG employees with concentrated positions holding big cap gains when it is time to diversify.

FAANG FIRE readers are eligible for a $250 sign up bonus when you join Frec and invest at least $20,000 into one of their Direct Indexing portfolios. If you are an extra guac member you also get AUM fees waived on your first $75,000 invested - this applies to the long short product too.

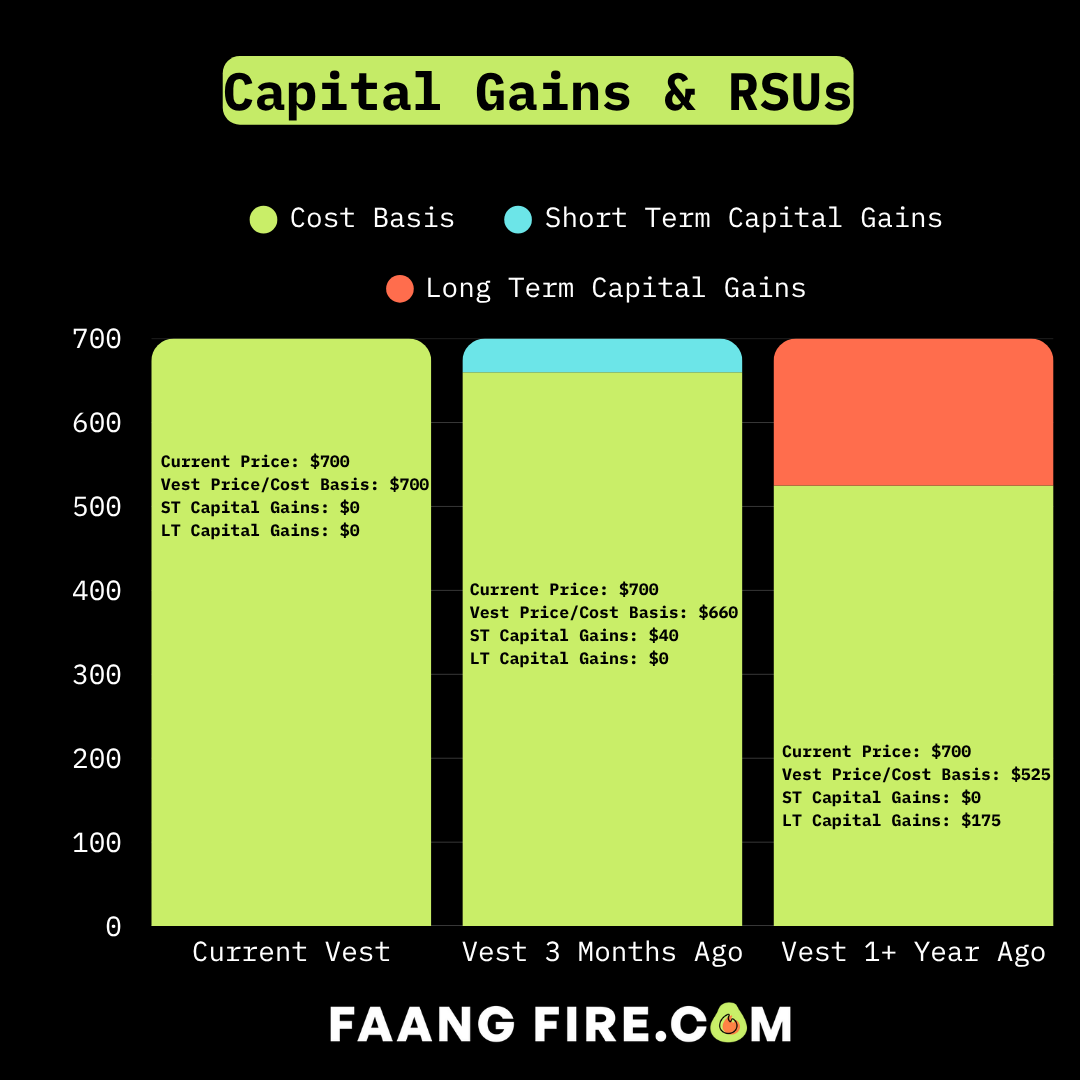

What about Capital Gains?

If the stock price goes up after vesting, you’ll also owe capital gains taxes when you sell. Only on the gain! So if the stock vested for $700 and you sold for $700, you would owe $0 in capital gains taxes. If the stock increased to $705, you would only owe capital gains taxes on the $5 of gain! How much though?

Short Term Gains vs Long Term Gains?

Short-term capital gains (held <1 year) are taxed at your ordinary income rate. Long-term gains (held >1 year) get lower rates, 15% if you’re under $533k single / $600k married, 20% above that, plus the 3.8% net investment income tax if you’re over $200k single / $250k married. States add their own layer: California taxes all gains as ordinary income, while Washington only taxes long-term gains above ~$270k.

Individual Tax Lots

Every vest creates a new tax lot with its own cost basis. Some lots will have short-term gains or losses, others long-term. The right decision isn’t always “sell long-term first”, it really depends on the specific tax impact of each lot.

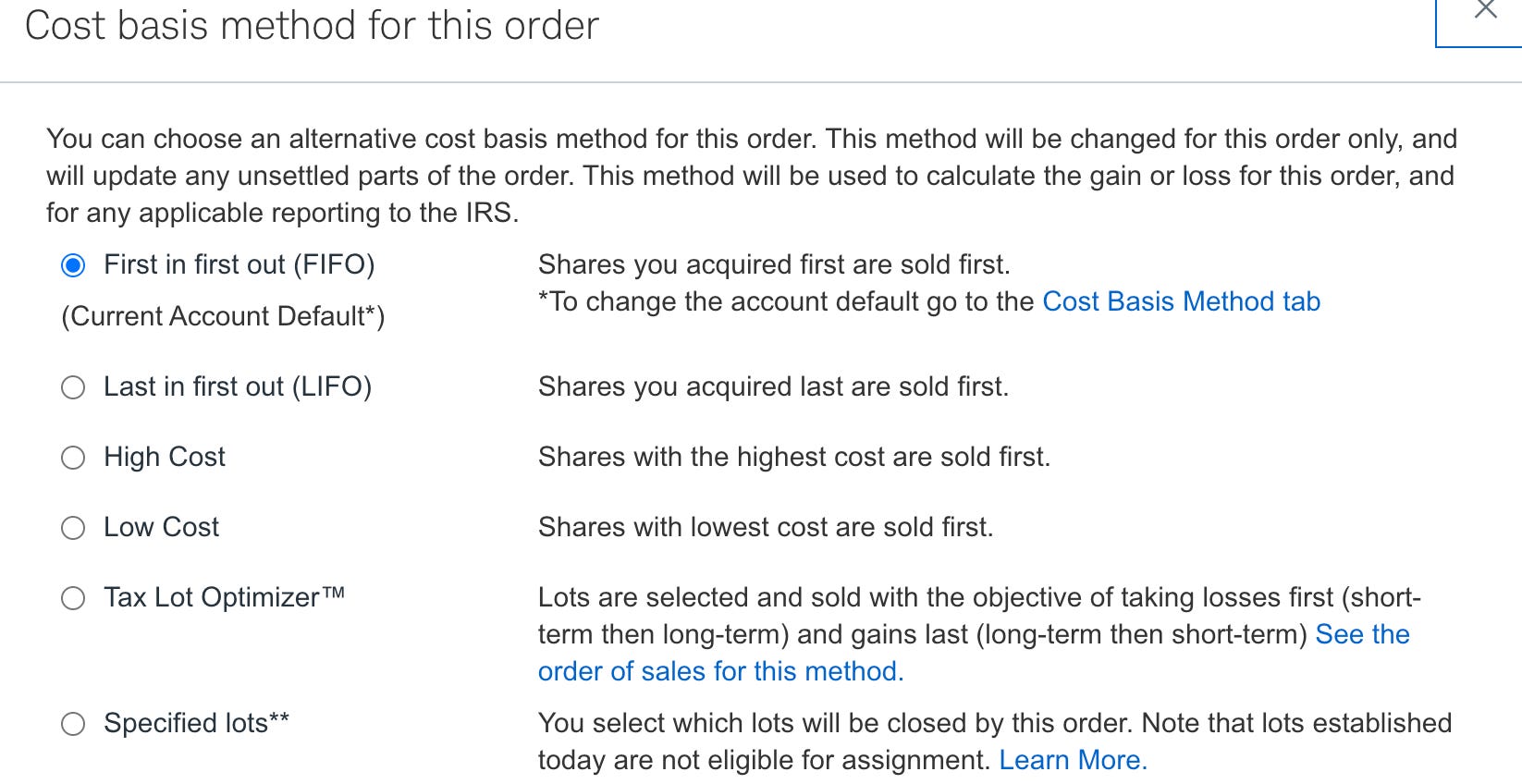

When you go to sell your company's stock, you can actually choose which lots you sell. This is often referred to as selecting the cost basis method for the specific order. By default, it is often first-in-first-out (FIFO), which means by default it will sell your oldest shares first. This can often be the worst option from a tax perspective!

Most brokers have tools like Schwab’s Tax Lot Optimizer:

Tax Lot Optimizer (or your broker’s equivalent), is often a great place to start.

However, what I like to do is export my lots into Google Sheets and calculate the tax impact myself, factoring in state taxes. That way I know exactly what each sale will cost and can prepare for the bill come April.

One metric I track is the tax impact per share, and in the next section I’ll walk you through exactly how to calculate it.

Tax Impact Per Share

Tax Impact Per Share is calculated by dividing the estimated taxes for a lot of shares by the number of shares in the lot. When I go through to select which lots to sell, I simply sort by Tax Impact Per Share lowest to highest.

I have a very rough Google Sheet you can use as a starting point at the end of this doc and I’ll even write the instructions below in a way that ChatGPT 5 can probably 1 shot an app to do this for you.

Disclaimer: This is for educational purposes only. Please consult a tax or financial professional for accurate calculations. Don’t sue Andre.

Calculation Examples

For the following calculations I am going to use the following assumptions:

Current Date: 8/8/2025

Current META Stock Price: $761.83

Marginal Federal Tax Rate: 35%

Long Term Capital Gains Tax Rate: 20%

Other Short Term Taxes: 3.8% NIIT which applies to both short term and long term gains, can be modified to add Short Term State Tax Rates

Other Long Term Taxes: 3.8% NIIT which applies to both short term and long term gains, can be modified to add Long Term State Tax Rates

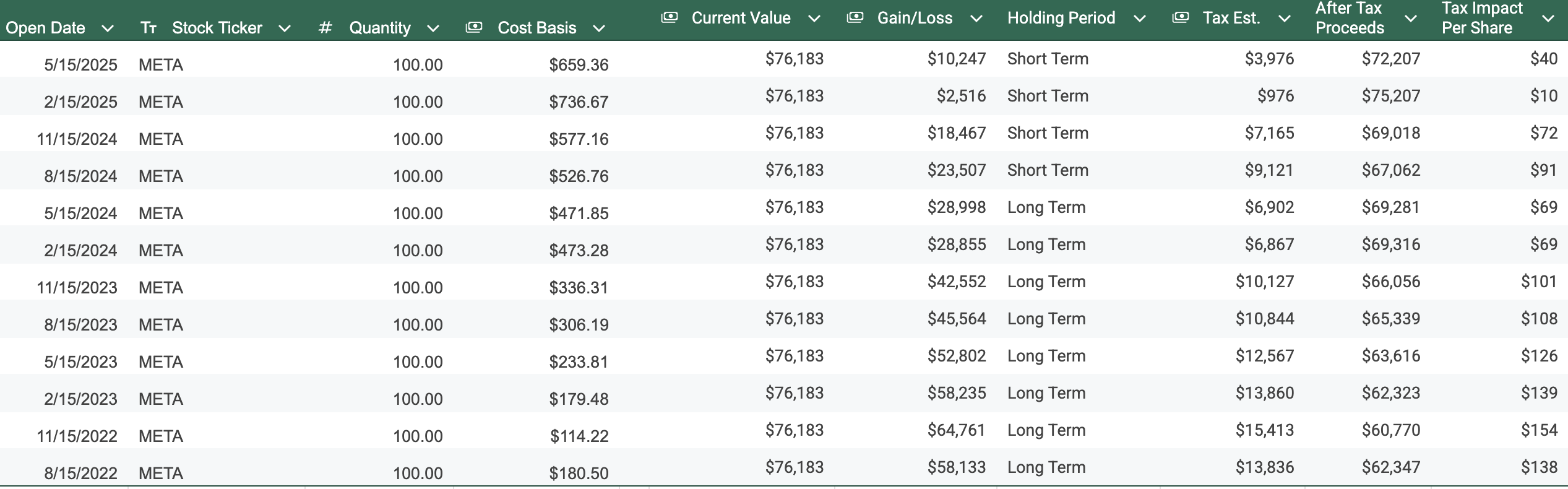

Short Term Lot Example

Stock Ticker: META

Vest Date: 5/15/2025

Quantity: 100

Cost Basis Per Share: $659.36

Calculations (rounded below for simplification):

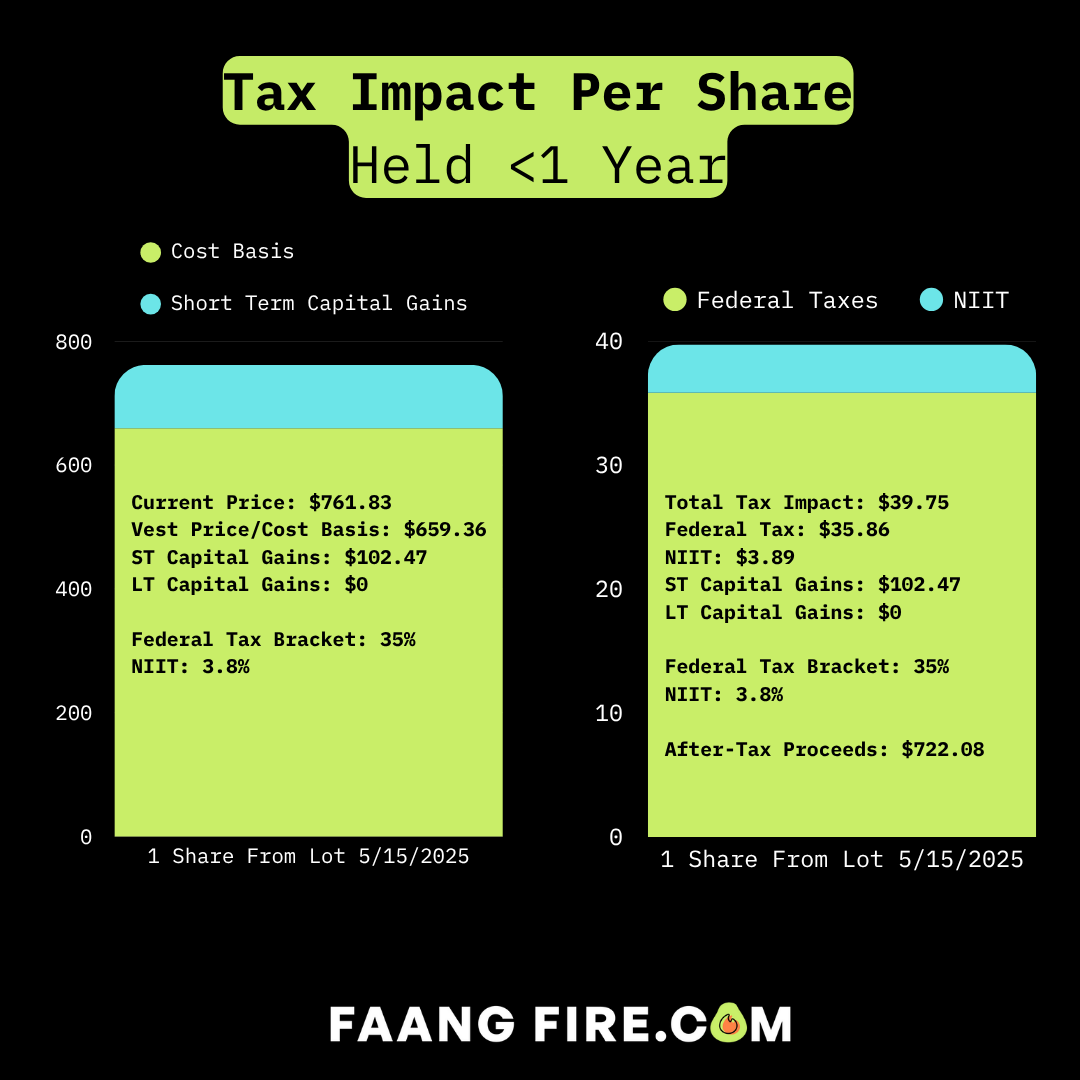

Current Value: $76,183 (Current Stock Price x Quantity; 100 x $761.83)

Gain/Loss: $10,247 (Current Value - (Cost Basis Per Share x Quantity)); $76,183 - (100 x $659.36))

Holding Period: Short Term (simplified: if Current Date - Vest Date <=365 then Short Term)

Tax Estimate: $3,976 ( If the Gain/Loss is >0 then multiply the Gain either all Short Term or all Long Term taxes; $10,247 x (35% + 3.8%)

After Tax Proceeds: $72,207 (Current Value - Tax Estimate, $76,183 - $3,976)

Tax Impact Per Share: $40 (Tax Estimate / Quantity, $3,976 / 100)

Let’s calculate this for every Meta RSU vest since August 2022:

As you can see, the “Tax Impact Per Share” in this case is positive for all lots! With the current lowest being the 2/15/2025 vests that have a cost basis of $736.67. Which gets taxed at Short Term Capital Gains rates, and still results in a lower tax impact per share than any of the Long Term shares.

Ok, here is the link to make a copy of the spreadsheet. Warning, this is very janky.

When Do You Pay Capital Gains Taxes?

Taxes on capital gains are not typically withheld/paid to the IRS automatically. Each broker will issue you a 1099 at the end of January that includes all the capital gains and losses you had over the prior year. You’ll use this form when you file your taxes in April of the following year. This is why I think it’s important to estimate your capital gains taxes throughout the year so you can prepare for any potential bill.

Offsetting Capital Gains with Capital Losses

This is also where having accumulated losses from strategies such as direct indexing or long short direct indexing can come into play. Any capital losses you have are used to offset capital gains. If you have more losses than gains, then you can use those losses to reduce your taxable income by $3,000 before the rest of the losses are carried forward into future years.

For example if you have accumulated $10,000 in losses and have $10,000 in gains, the net capital gains for the year would be $0 and there wouldn’t be any additional federal tax obligation.

Washington State Note: At the federal level short term losses can be used to offset long term gains. In Washington that isn’t the case. Only long term losses can offset long term gains, and short term gains aren’t taxed at the state level.

Interested in learning more about how tax loss harvesting with direct indexing and long short direct indexing with factor tilts work?

Join us for a FIREside chat this week with the CEO, Mo Al Adham, on August 13th at 12pm PST. Registered here: https://lu.ma/dx6nomhv

Don’t Let The Tax Tail Wag The Dog

You shouldn’t only focus on taxes when it comes to selling RSUs. I would first determine how many of your RSUs you want to sell, and THEN go about determining the most tax efficient way to sell those shares.

Calculating the Tax Impact Per Share is just one small piece of an effective strategy around dealing with RSUs. I do think it is an important piece of information to understand. Too many people state a nebulous “I am not selling because of taxes” excuse to ignoring their RSU vests. By calculating the Tax Impact Per Share at least you can quantify it.

Disclosure: I am a Frec client and Frec paid a one time fee for the upcoming webinar. Investing involves risks, including the risk of loss. Long short strategy will add to your risk.

Read about how I personally use Frec in my original direct indexing article and 6-month follow up.

Thank you for this post Andre! It is super helpful.

Thank you for the post. One question that remains for me is that here you only consider the one sale and do a greedy optimization that does not consider future sales. It seems to me that selling short-term lots and paying more taxes is always going to be worse than selling long-term ones since the taxes there will be less. Even if the short-term lot may pay less tax now, you are still paying a higher rate, and the long-term lot will have to be sold *eventually* anyway, so it is not like you're avoiding *those* taxes. This of course assume selling all lots eventually and therefore ignores estate planning, for simplification purposes.

I would like to write a complete simulation of different strategies taking into account multiple sales across time. While I haven't had the chance to do that yet, I did have this interesting conversation with ChatGPT, for what it's worth: https://chatgpt.com/share/68adf4db-b964-8001-a8c7-436475bcf51b