The 3 Year + 75% Confidence Rule For Home Buying

One rule of thumb I keep coming back to is what I’m calling the “3-Year 75% Confidence Rule.”

Yeah… that does not exactly roll off the tongue.

So for now, let’s just call it: The 3-75 Rule

The 3-75 Rule:

If there is at least a 75% chance you will need the money within the next 3 years, that money should not be invested in stocks.

It can apply to any large purchase, but I use it most often with coaching clients who are considering buying a home.

Today’s newsletter is sponsored by Wealthfront.

Doing my taxes and seeing how much interest my cash generated last year was a good reminder that this stuff adds up. It reinforced why Wealthfront is a core part of my 2026 goal to simplify my financial life.

My high-yield Cash Account at Wealthfront has consistently provided access to one of the highest APYs I’ve seen along with up to $8M in FDIC insurance through program banks.

Right now for a limited time, Wealthfront is offering my audience an exclusive 0.75% APY boost for three months on up to $150,000, for a total 4.05% variable APY when you open your first Cash Account using my link. Go to wealthfront.com/andre. Base APY is 3.30% as of 1/30/26, is provided by program banks, and is subject to change. Promotional terms and conditions apply. See our affiliate link for more details.

The Core Framework

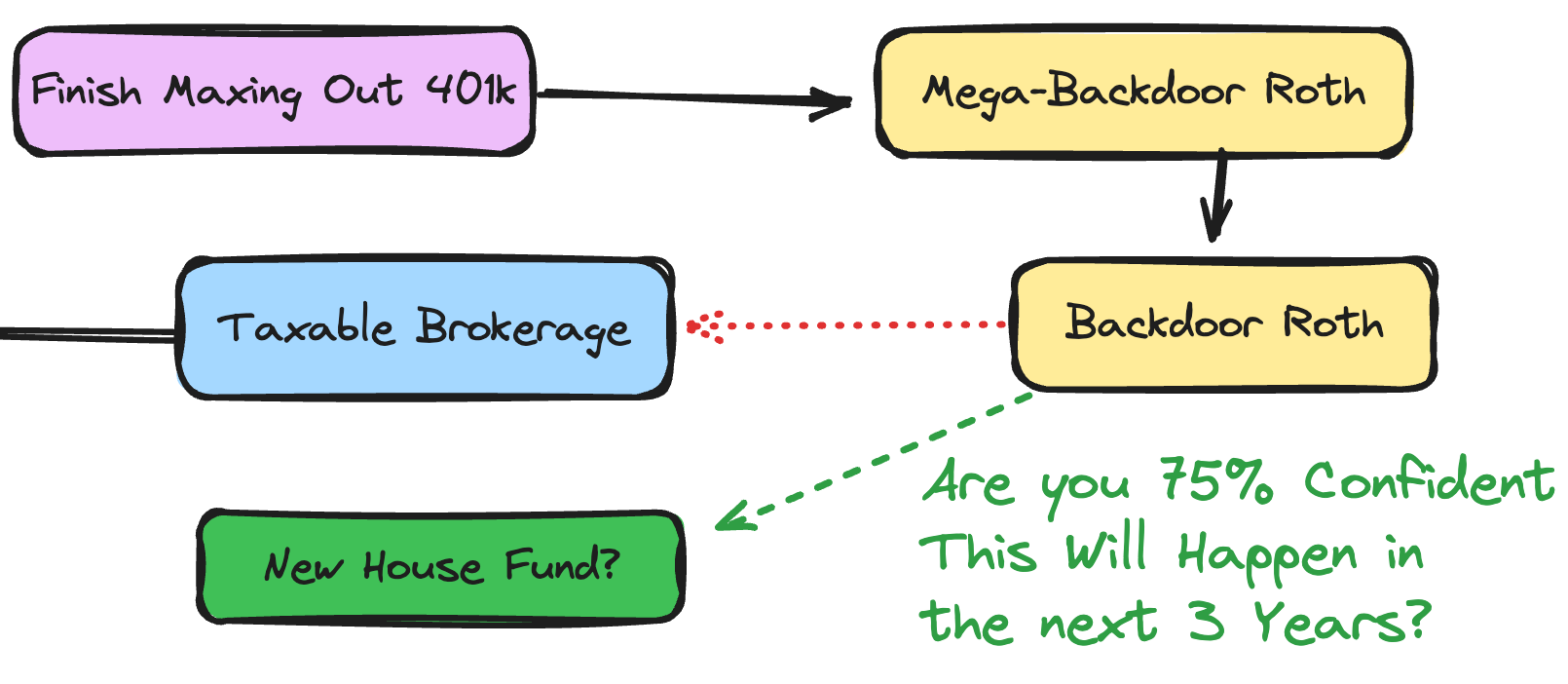

Ask yourself if you are 75% confident that you will make the purchase (like buying a house) in less than 3 years.

If you are less than 75% confident: You should keep investing your excess cash beyond your emergency fund in equities rather than sitting on it.

If you are at least 75% confident: That is the trigger to start being realistic, pull back your equity exposure, and build up a cash position for the down payment. At this stage, you shouldn’t keep those funds exposed to potential 20% market drops.

The Standard 5-Year Trap

Traditional financial advice often uses a five-year timeframe. If you’re going to need money in the short term, it should not be exposed to stock market volatility.

But in cities like San Francisco, New York, Seattle… I have seen so many people fall into the trap of “we’re going to buy a house in 5 years“.

It becomes a nebulous rolling timeline of you saying “5 more years, 5 more years, 5 more years”. Next thing you know it has been 15 years and y’all are still saying “we’re going to buy a house in 5 years”.

The trap here is that you have been leaving your excess cash uninvested this entire time!

The 3-75 Rule is supposed to challenge you. Are you really planning on buying a house? I want to force you to be honest with yourself.

Why 3 Years?

In 2026, five years feels like an eternity. It is just too far away to be useful.

Three years feels different. It feels close enough that I can be directionally right.

I’ve been using a personal three-year rule for bigger life decisions for a while now, from my career to where I want to live to school decisions for my daughter.

I am writing this right now in March 2026. That means I want to really think about whether you are going to buy that house any time between now and March 2029.

Try imagining your life in March 2029.

I can personally picture my daughter finishing her final months of 5th grade. As I extend my vision out into 2030… everything gets fuzzy!

How old will you be? How old will your kids be? What grades will they be in? Will you still be working the same job? Will you be itching to live somewhere else?

The 3-75 Rule is really just the financial version of that broader idea.

The 75% Confidence Threshold

There is nothing magical about 75%.The point is forcing yourself to put a number on the decision.

Sitting on cash for a year or two is fine. If you do not end up using it, sure, it probably would have been better off invested. But over a short stretch, that usually is not going to make or break your plans.

The real problem is when that cash drag quietly stretches into 10 years.

That is why the 75% threshold matters. It forces you to be honest with yourself. Are you actually likely to buy within 3 years, or are you just using a future purchase to justify holding more cash than your investment philosophy would otherwise support?

That is the real question: Are you at least 75% sure you are going to do this within 3 years?

Is there a deeper reason you are sitting on that cash?

I really want to push people on this whenever they’re saving for bigger purchases.

Are you actually 75% sure you’re going to go through with it in the next 3 years? Or has that future purchase become a stand-in for something else?

Because sometimes the cash is not really about the house. Sometimes it is about wanting flexibility. Wanting optionality. Wanting to feel safe in a world that feels uncertain.

And to be clear, there is nothing wrong with that.

There is nothing wrong with being more conservative. There is nothing wrong with holding more cash. There is nothing wrong with wanting a bigger safety net.

But be honest about what that cash is doing for you.

If it is truly for a near-term purchase, great. Call it that.

If it is really there because it helps you feel more secure, that is fine too. Call it an expanded emergency fund. Write down the number that actually makes you feel safe, whether that is six months, twelve months, or something else entirely. Then invest the rest with confidence.

Because over the next 5, 10, 15, or 30+ years, what matters most is not whether you perfectly timed one future home purchase. It is whether you built the habit of consistently investing your excess cash instead of leaving it on the sidelines because maybe, possibly, someday, you might need it.

That’s the FAANG FIRE 3-75 Rule. Tell me what you think in the comments!

Disclosures:

Andre Nader is a Wealthfront client and was compensated ~$3,330 for the testimonial and promotion of the Wealthfront Cash Account. This compensation creates a conflict of interest. Experiences may vary among Cash Account clients, and results are not guaranteed.

The Cash Account, which is not a deposit account, is offered by Wealthfront Brokerage LLC (”Wealthfront Brokerage”), Member FINRA/SIPC. Wealthfront Brokerage is not a bank. The Annual Percentage Yield (”APY”) on cash deposits as of January 30, 2026, is representative, requires no minimum, and may change at any time. The APY reflects the weighted average of deposit balances at participating Program Banks, which are not allocated equally. Funds in the Cash Account are swept to Program Banks where they earn a variable APY and are eligible for FDIC insurance. Conditions apply. For a list of Program Banks, see: www.wealthfront.com/programbanks. FDIC pass-through insurance, which protects against the failure of Program Banks, not Wealthfront, is not provided until the funds arrive at the Program Banks. While funds are at Wealthfront Brokerage, and while they are transitioning to and/or from Wealthfront Brokerage to the Program Banks, the funds are eligible for SIPC protection up to the $250,000 limit for cash. FDIC insurance is limited to $250,000 per customer, per bank, regardless of whether those deposits are placed through Wealthfront Brokerage. You are responsible for monitoring your total deposits at each Program Bank to stay within FDIC limits. Wealthfront works with multiple Program Banks to make available up to $8 million ($16 million for joint accounts) of pass-through FDIC coverage for your cash deposits. For more info on FDIC insurance coverage, visit www.FDIC.gov.

If you are eligible for the overall boosted rate of 4.05% offered in connection with this promo, your boosted rate is also subject to change if the base rate decreases during the three-month promotional period.

Can you explain the dotted line from RothIRA to taxable brokerage? Is it moving money from rothIRA after 5 years. If so, whats the thought process in doing that? rather than letting it grow in Roth