I Still Have My Meta 401k

I still have my Meta 401k even though it has been two years since I was laid off.

The main point of this post is to tell you that it is ok to keep your old 401k. You don’t need to do anything with it.

The primary reason I still have mine is so I can still contribute to a backdoor roth ira. Even if I didn’t want to do a backdoor roth, there is minimal downside to keeping my 401k in my Meta plan.

So if you were recently laid off, or voluntarily left your job, I don’t want you to feel like your 401k is something you need to deal with right away. Odds are, doing nothing with your 401k can be perfectly fine.

It used to be common wisdom that after you leave a company, you should roll your workplace 401k into a rollover IRA.

I think this is bad advice.

When you leave a company, you typically have three options for what to do with your 401k. For those in big tech, choosing to use a rollover IRA is the worst of those three options.

Three Options on Handling Old 401ks

Option 1: Do Nothing

Do nothing. Keep your 401k at your old company. This is a perfectly good option, especially for those who recently left their jobs. Don’t feel like you need to do anything with your 401k right away. You can ignore it, knowing that it is often a perfectly good solution. You can look at me; I still have my Meta 401k and I was let go more than two years ago.

Option 2: Roll Your Old 401k Into Your New Company 401k

Roll your old 401k into your new workplace 401k. I am a fan of simplifying your financial life. The fewer accounts, the better. So if you join a new company, consolidating all your 401ks into your new one can be a good option. If I didn’t semi-fire, I would likely choose this option.

Option 3: Roll Your 401k into a Rollover IRA

Roll your old 401k into a Rollover IRA. This used to be the common advice for anyone leaving a company. I think this should no longer be the default! I think anyone who tells you to do this should be able to clearly explain why. (I have encountered advisors who recommend this, which I interpret as a way to increase the assets they manage and collect fees on).

FAANG folks, ex-FAANG, or those soon to be ex-FAANG, and really all high earners in tech, the generic advice around your finances is often wrong. It wasn’t written for you! That is why I write this newsletter! If you are into that, consider subscribing. If you have a friend that might be into that, I’d definitely appreciate a share.

Four Reasons Why I Still Have My Meta 401k

TLDR:

If I rolled my 401k into a rollover IRA, then I wouldn’t be able to contribute $7,000 per year into my Backdoor Roth IRA due to the pro-rata rule.

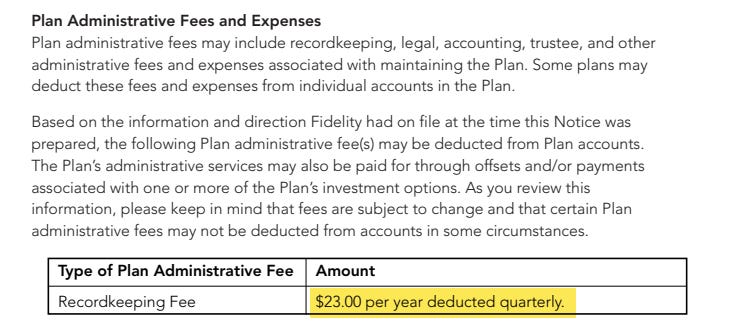

Meta’s 401k plan is actually great. For ex-employees, annual fees are only $23. The expense ratios on the funds are lower than you could get elsewhere.

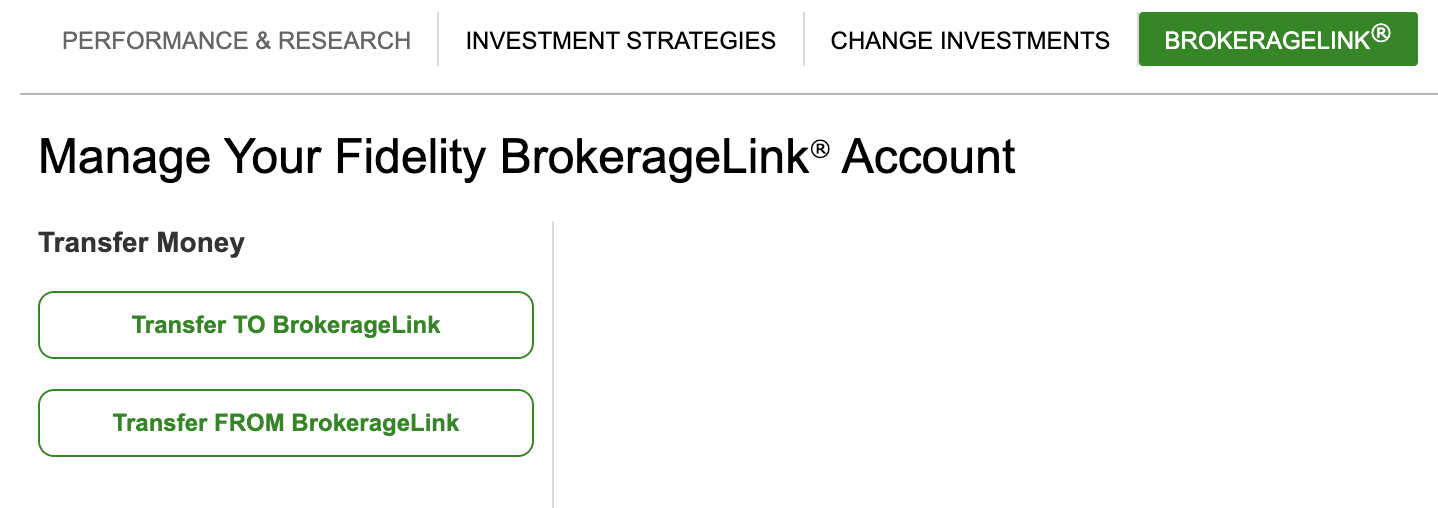

Even if I didn’t like the 401k options, Meta’s 401k has BrokerageLink, which allows you to purchase nearly almost any stock or funds on the open market.

There are additional asset protections that a 401k has that an IRA doesn’t.

Reason #1: Backdoor Roth Compatibility

The main reason I still have my Meta 401(k) is that it lets me keep doing the backdoor Roth.

If you have an existing traditional or rollover IRA, the IRS treats all your IRAs as one when calculating taxes on a Roth conversion. That “pro-rata rule” often makes the Backdoor Roth not worth doing.

Rolling my 401(k) into a rollover IRA would trigger that rule and kill the Backdoor Roth.

Check out my longer article on the specifics of the pro-rata rule for more details, especially if you still want to do a backdoor Roth (or already did one this year).

Reason #2: Meta’s 401(k) Plan Is Actually Really Good

This used to be common wisdom or generic advice: “After you leave your employer, you should roll over your 401(k) to a rollover IRA”

But it’s 2025 (or later, depending on when you are reading this), and many of you are working at FAANG companies with really good 401(k) plans. The reason this advice was prevalent in the past was because 401(k)s were notorious for having terrible options and super high fees. You’d be stuck with things like American Funds with 1%+ fees on everything, and you were restricted by what you had access to within your 401k.

If you’re working at a FAANG company, or really any large employer, your options are probably great.

Let’s look at Meta’s 401(k) for example. I have access to a full array of funds that I couldn’t get as a normal consumer. These are institutional-only options. I have State Street investments with extremely low fees (some 0.01% or lower), and there are no annual fees.

One thing to look out for: if your old company’s 401(k) starts charging annual fees now that you’ve left, those fees can be in the hundreds of dollars and make it not worth keeping. But in Meta’s case, it’s only $23 per year, which is minimal.

Reason #3: Investment Flexibility (BrokerageLink)

Another reason people recommend rollovers is to get more investment options.

Meta’s 401(k) has access to something called BrokerageLink, which allows you to purchase any fund in the open market. So I’m not only restricted to the core plan funds. I can essentially buy anything.

Investment options alone are no longer a good reason to roll over.

Reason #4: Asset Protection

Finally, 401(k)s have some specific asset protections that IRAs don’t.

There is a lot of nuance here, that varies by state. It is worth understanding how your state treats IRA accounts and what’s at risk if you get sued, go through bankruptcy, or a divorce.

California, for example:

In California, some retirement accounts are protected (such as 401ks and profit-sharing plans). Others are more vulnerable to judgment creditors (such as IRAs). -NOLO

Based on the article linked above, it seems like there are still protections in place for rollover funds. I am very much not a lawyer, so I won’t begin to think through strategies that involve cycling funds through a 401k.

This still highlights differences in protections for 401k accounts and IRA accounts, which are very state-specific.

What Should You Do With Your 401k If You’ve Left Your Company?

So, should you do what I did and keep your old 401(k)?

You have to look at all the details:

What are your investment options?

What are the fees?

Do you plan to keep doing the backdoor Roth?

Is your new employer’s 401k better?

Option one is to do nothing. I don’t think you should feel bad for not dealing with your old 401(k) and just keeping it there.

Option two, if you’ve gotten a new job, is to move your old 401(k) into your new employer’s 401(k). Most plans will allow this. This is another good option if you still want to do the backdoor Roth and avoid the pro-rata rule.

Option three is rolling it over into a rollover IRA. That can be a good option if the funds in your 401(k) are poor or the fees are high, and you don’t plan to do a backdoor roth.

What About My Roth Funds?

Did you know I don’t have any Roth funds within my Meta 401k?

One of my main justifications for keeping my Meta 401k was so I could still do the backdoor Roth IRA without running into the pro-rata rule, by having funds in a rollover IRA. This only applies to pre-tax IRA accounts. Having a Roth IRA with funds separate from your 401k doesn’t impact your ability to do a Backdoor Roth IRA at all.

I have never kept my Roth funds in my Meta 401k. These were funds that resulted from contributing to my Mega Backdoor Roth. Even though Meta had an automatic in-plan conversion of after-tax funds to a Roth 401k, I would still roll those Roth funds out into a separate Roth IRA.

Why would convert my mega backdoor roth ira funds from my 401k into a separate Roth IRA?

Honestly… it was to make it easier for me to track my investment funds across different tax types (Roth, Pre-Tax, Taxable). This isn’t a practical reason, it just made it easier for me to personally track in my spreadsheets. Fidelity required too many steps for me to easily see the breakdown of Pre-tax vs Roth. It is there; it was just a pain to parse out. So I would regularly roll my Roth funds into a separate Roth IRA.

Meta’s 401k allowed me to move Roth 401k funds into my Fidelity Roth IRA directly through the “Rollover” flow in NetBenefits. Not all 401ks allow this, even my partner’s Uber 401k doesn’t make it possible without calling Fidelity. So your mileage may vary!

The Takeaway

The main takeaway: beware of generic financial advice, especially advice from past generations that no longer applies.

If you’re in tech with a strong 401(k) plan, the old “always roll it over” advice isn’t necessarily true anymore.

Understand:

The pros and cons of rolling over

The option of moving it into your current employer’s plan

And that it’s okay to just keep it where it is

I’m also a big fan of simplification. Over time, if you have multiple old 401(k)s sitting around, that’s not ideal. If you get a new job with a decent plan, consider consolidating them, but be mindful of the backdoor Roth implications.

If you’re not doing a backdoor Roth, don’t overthink it. Keep it simple.

If you have any questions, drop a comment or reply to the email if you got this via the newsletter.

Thanks again for being a subscriber!

-Andre

Note that depending on the employer plan, one might not be able to move Roth funds (Roth 401(k) contributions) while still employed. Converting Roth portion to Roth IRA after employment should be allowed which separates Roth and non-Roth portions.

I followed that advise and rolled my Meta 401K into IRA in Robinhood. And eventually realized what I did -- I lost the chance to contribute to the Backdoor Roth IRA. Is this completely irreversible?